• Risk wobbles. Positive sentiment after the Nvidia earnings report faded. US equities declined, as did bond yields. AUD & NZD lost ground.

• US jobs. Delayed US jobs data showed stronger payrolls but also higher unemployment. Odds of a December US Fed rate cut have declined.

• Data flow. Global PMIs & Fed members speaking today. Because of shutdown backlog Fed won’t have another jobs report before mid-December meeting.

Global Trends

Risk appetite continues to swing around with another burst of volatility coming through overnight. The positive vibes stemming from yesterday’s corporate earnings report from tech-powerhouse Nvidia faded. Broader sentiment changed direction as government shutdown delayed US jobs data raised more questions about near-term policy decisions by the US Fed. The US S&P500, which was up almost 2% early on, ended the session in the red (-1.6%) with the tech-focused NASDAQ underperforming (-2.2%). Timing is everything. While the NASDAQ is now a little more than 8% below its late-October record highs, it remains almost 13% above where it started the year and ~49% from its ‘Liberation Day’ April lows.

The intra-session reversal in risk sentiment flowed through to other asset classes with US bond yields falling ~5-6bps across the curve as investors sought ‘safe-haven’ shelter. Oil prices slipped back (WTI crude -0.4% to ~$59.30/brl), as did copper (-1.3%). In FX, as per our expectations at the start of the week, the USD index ticked up a bit further with EUR consolidating (now ~$1.1526) and USD/JPY extending its upswing (now ~157.52, a fraction below its 1-year peak) with reports Japan’s new PM Takaichi is set to announce the largest spending plan since the pandemic keeping the JPY on the backfoot despite ‘hawkish’ rhetoric from BoJ Board member Koeda about the need to proceed with interest rate normalisation. Elsewhere, the backdrop exerted downward pressure on the NZD (now ~$0.5589, a low since mid-April) and AUD (now ~$0.6444, near the bottom end of the range occupied the past few months).

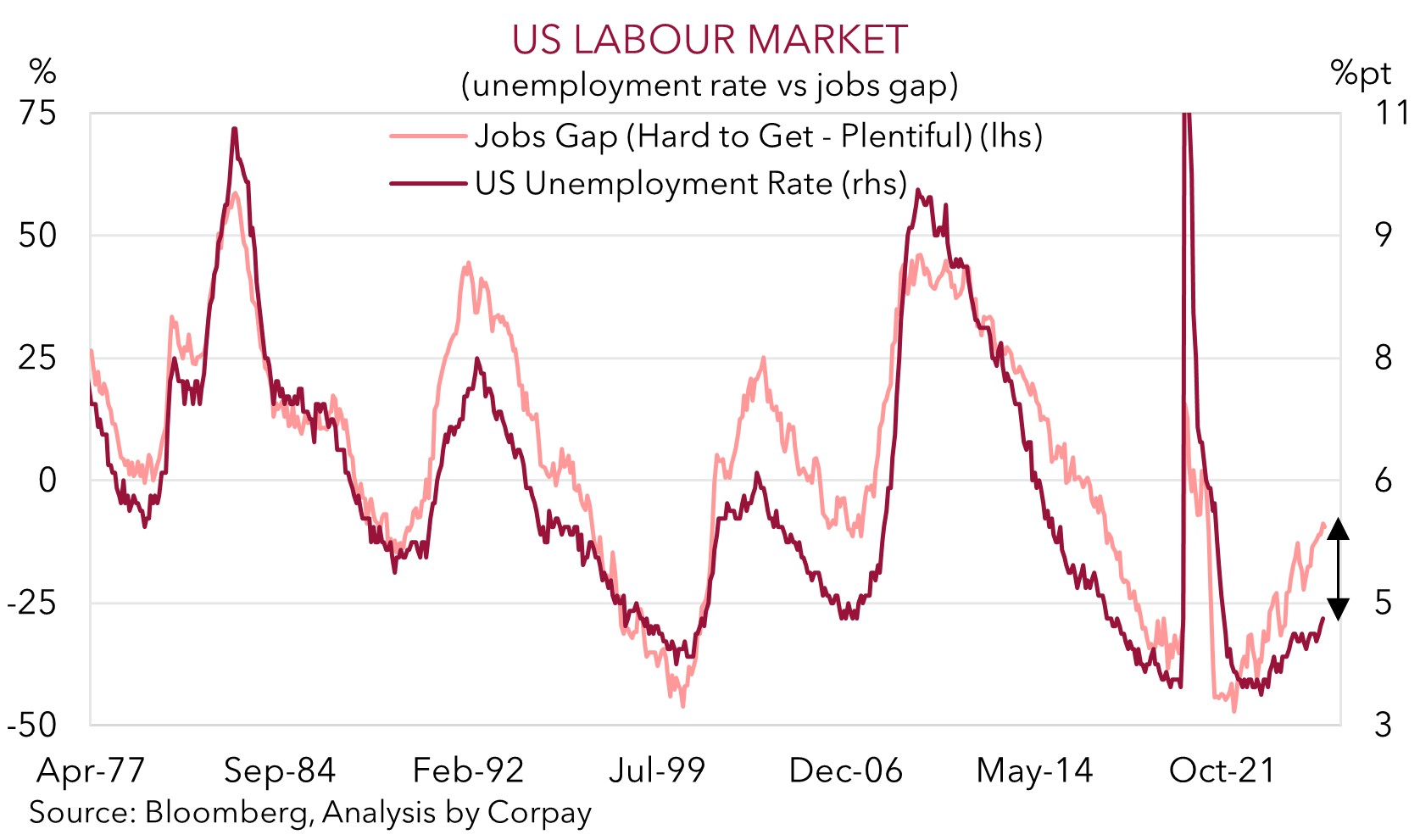

In terms of the US data, the delayed September jobs report was a mixed bag. Non-farm payrolls were stronger than predicted, with 119,000 workers added, though negative revisions to prior months take some of the shine off the headline figure. The US unemployment rate nudged up further to 4.4%, another sign the cracks in the overall labour market are widening, particularly as forward indicators suggest it may have more to go (see chart below). The havoc caused to the US data flow by the prolonged government shutdown means this is the last set of official job stats the US Fed will see before its next meeting (the October & November US jobs reports are set to be released on 17 December AEDT, while the US Fed meets on 11 December AEDT). Policymakers are flying somewhat blind, and as a result pricing for a December rate cut has been trimmed (odds of another rate reduction in December are now ~35%). The global PMIs are due today (Eurozone 8pm AEDT, US 1:45am AEDT). A few US Fed members are also speaking. We think signs of resilience in the US and/or shaky risk appetite may keep the USD supported in the short-term.

Trans-Tasman Zone

The wobbles across risk markets such as US equities and base metals, coupled with a firmer USD (largely due to the weaker JPY) has weighed on the NZD and AUD the past few sessions (see above). At ~$0.5589 the NZD is hovering around its lowest level since mid-April, while the AUD (now ~$0.6444) is near the bottom of the rather tight ~4.5% range it has oscillated within since late-June. The backdrop has also seen the AUD lose ground on most of the major crosses with falls of ~0.2-0.5% recorded against the EUR, GBP, NZD, and CNH over the past 24hrs. AUD/JPY has consolidated just below its 1-year peak (now ~101.50). As mentioned before, we think the bout of JPY weakness generated by expectations of increased fiscal spending in Japan might not last and that there is a growing risk of an abrupt reversal in the JPY over the period ahead. Crosses like AUD/JPY and NZD/JPY look stretched compared to underlying drivers such as relative yield spreads, in our opinion.

Locally, it is a limited economic data calendar until next Wednesday’s October CPI figures. We think the inflation report could once again show that underlying inflation remains sticky, reinforcing the view that the RBA may not cut interest rates again this cycle. In NZ, the RBNZ also meets next Wednesday. A 25bp rate cut appears likely, which if realised would lower the RBNZ OCR to 2.25% as policymakers try to revive NZ’s economic fortunes.

In the short-term, we believe the burst of market volatility and firmer USD stemming from the shaky risk sentiment and reduction in December US Fed rate cut expectations might keep the AUD and NZD on the backfoot. However, barring a sharp sustained deterioration in risk appetite we doubt that the AUD will lose that much more ground. The AUD is already tracking a few cents under our ‘fair value’ models, indicating a degree of negative news is already baked in. As sentiment stabilizes, we think the underlying improvement in US/China trade relations, more favourable yield spreads between Australia and other nations, and a pickup in growth momentum in China as stimulus measures gain traction should help the AUD claw back lost ground over coming months.