• Upbeat tone. Softer US inflation, solid PMIs & positive US/China trade talks support risk sentiment. Equities rose. AUD & NZD strengthen.

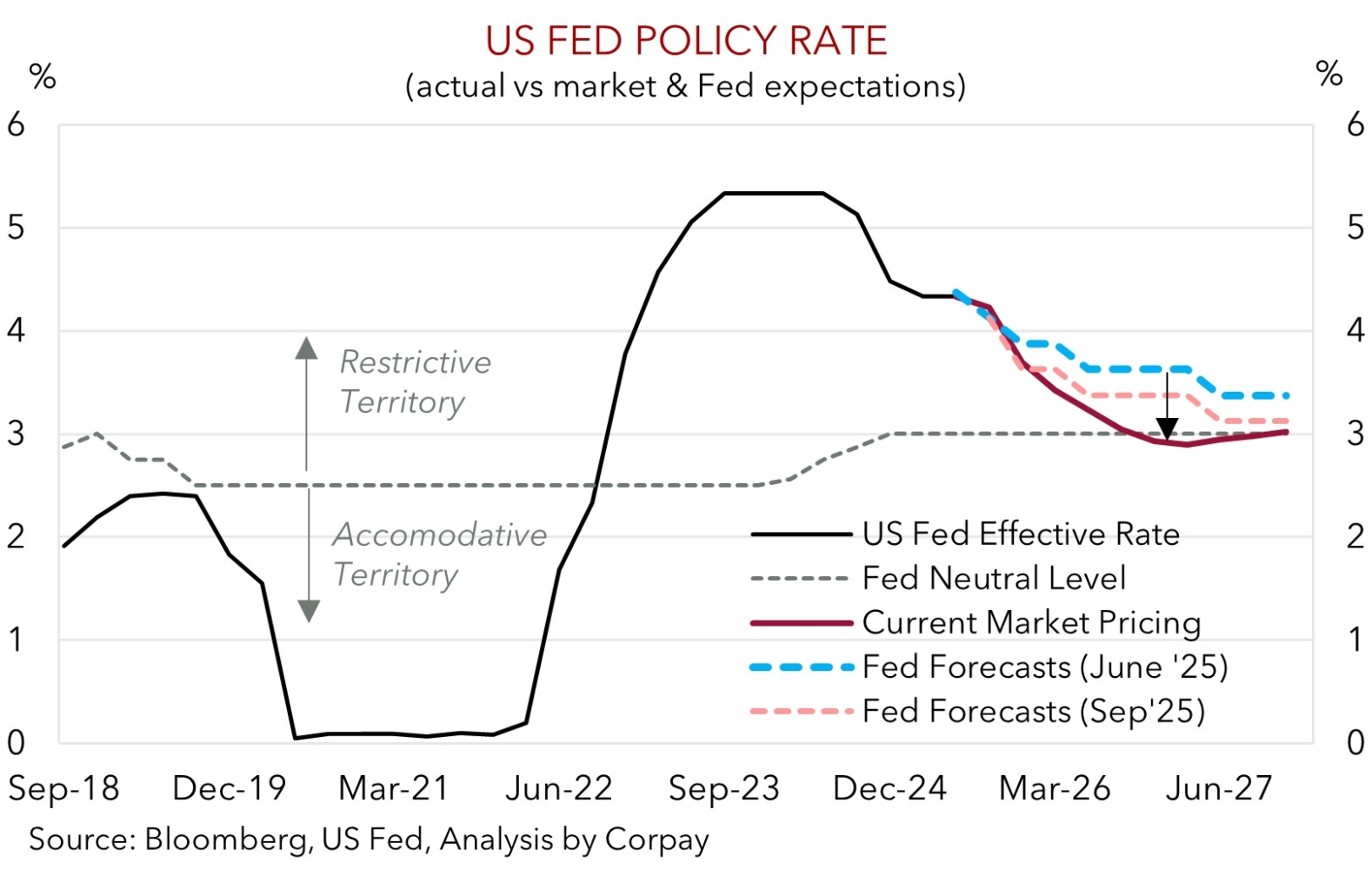

• US Fed. Upside US inflation risks fading while downside jobs risks rising. US Fed looks set to cut rates this week & should keep door open to more.

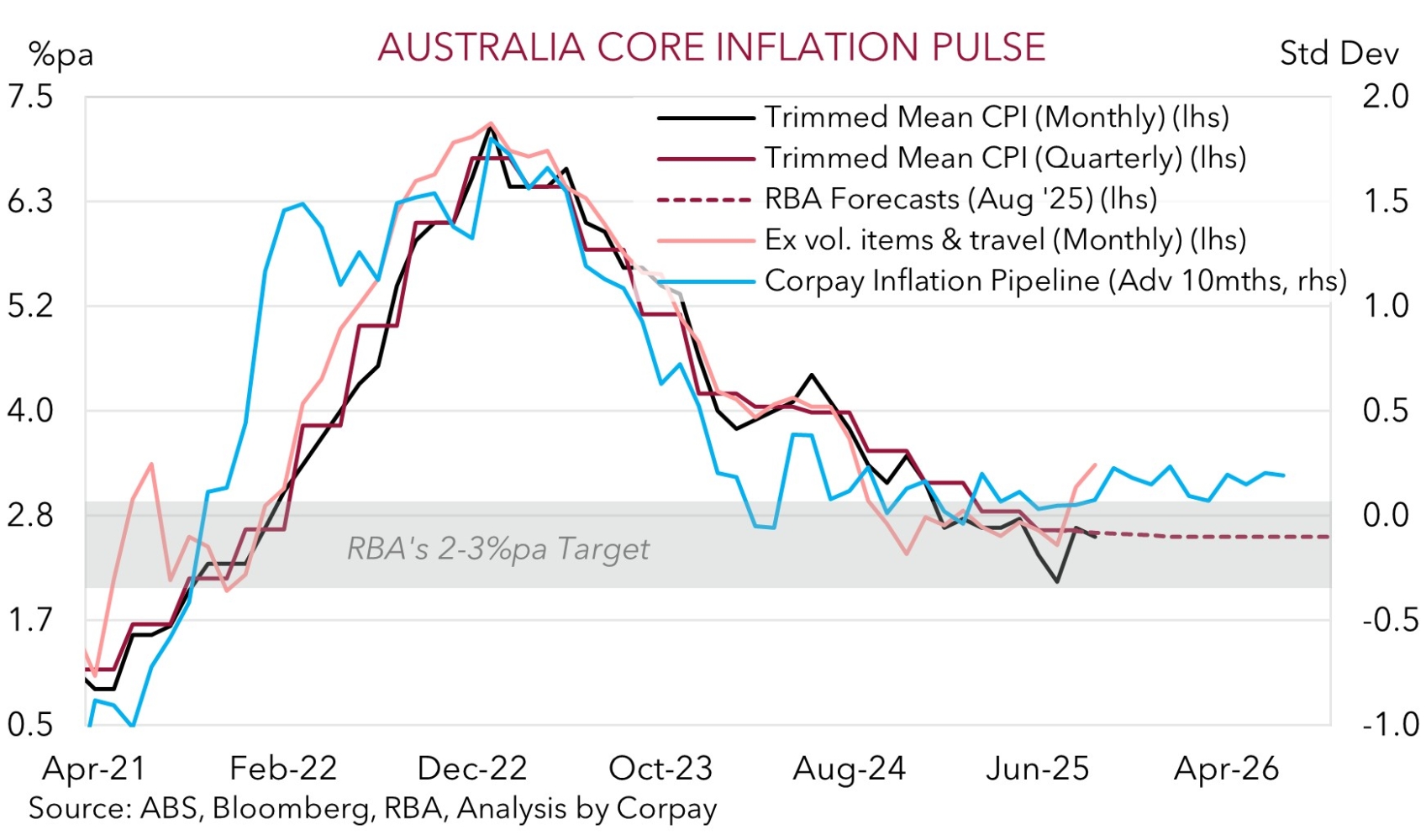

• AU inflation. Gov. Bullock speaks tonight, Q3 CPI due Weds. Monthly data points to uptick in Q3 inflation. RBA rate cut pricing may be pared back.

Global Trends

A combination of factors underpinned risk sentiment at the end of last week and in this morning’s early Asian trade. US and European equities rose on Friday with the S&P500 (+0.8%) and NASDAQ (+1.2%) touching record highs, while bond yields were steady and cyclical currencies such as the AUD (now ~$0.6540) and NZD (now ~$0.5779) strengthened. Elsewhere in FX the EUR ticked up (now ~$1.1636), USD/CNH slipped back (now ~7.1185), and USD/JPY edged up a little more (now ~152.83) to be near the top of the range occupied since mid-February.

In terms of the drivers behind the upbeat market tone the government shutdown delayed September US CPI was relatively more benign than forecast. US core inflation slowed to 3%pa with the tariff pass-through to ‘goods’ prices still somewhat constrained and ‘services’ prices slowing with rents a major drag. The moderation in US inflation coupled with the challenges in the jobs market reinforced expectations looking for a stream of US Fed interest rate cuts over coming months with a move this week now almost fully discounted (Thurs morning AEDT). In addition to the US CPI the generally better than anticipated US and Eurozone business PMIs painted a resilient picture about growth. And over the weekend US/China trade relations looked to have taken a step in a more positive direction with negotiators announcing a “very successful” framework for the meeting between President’s Trump and Xi at this week’s APEC summit. According to reports the US and China reached a consensus on several contentious issues with the potential agreement set to cover export controls, shipping levies, fentanyl, and China’s rare earth trade.

This week in addition to headlines from the discussion between President’s Trump and Xi, market action may also be driven by central bank meetings. Another 25bp rate cut in Canada is looked for (Weds night AEDT), while the European Central Bank (Thurs night AEDT) and Bank of Japan (Thurs) are forecast to hold steady. In the US with the government shutdown still in place economic data releases will remain on ice, however the US Fed is still meeting, and another rate cut should be delivered (Thurs morning AEDT). We think Fed Chair Powell could keep the door open to more action down the track given upside risks to inflation seem to be fading and downside labour market risks are building. We remain of the view that the outlook for lower US interest rates combined with slower economic activity due to higher import costs/uncertainty should see the USD gradually weaken over the medium-term.

Trans-Tasman Zone

The positive vibes across risk markets stemming from the mix of softer US CPI inflation, improved US/Eurozone PMIs, outlook for US Fed interest rate cuts, and positive US/China trade developments has given the AUD and NZD a boost (see above). At ~$0.6540 the AUD is near its 3-month average while the NZD (now ~$0.5779) is north of its 1-month average. The backdrop has also given the AUD a helping hand on the major crosses with gains of ~0.4-0.6% recorded against the EUR, JPY, GBP, CAD, and CNH since this time on Friday. At ~0.5625 AUD/EUR is above its 100-day moving average while AUD/CNH (now ~4.6585) is approaching its 50-day moving average. Elsewhere, AUD/JPY (now ~99.95) is close to the top of its year-to-date range, though we believe it is looking stretched compared to fundamental drivers such as relative yield spreads.

In Australia RBA Governor Bullock holds a fireside chat tonight (7:15pm AEDT) and on the data front Q3 CPI inflation is a focal point (Wednesday). Tonight’s discussion will provide an opportunity to gauge Governor Bullock’s thoughts on the tension between inflation and labour market trends. It is an interesting time with core inflation still lingering above the RBA’s target while labour market conditions are cooling.

In terms of the quarterly CPI, based on the monthly indicator Q3 inflation may come in above the RBA’s forecasts. The question is by how much with core inflation (a gauge of inflation persistence) monitored closely by RBA policymakers. Trimmed mean (the RBA’s preferred core inflation measure) is forecast to accelerate in Q3 with consensus looking for it to step up to ~0.8%qoq. We think the RBA might need to see a ~0.7%qoq or lower result to justify a rate cut this year. With interest rate markets factoring in a ~63% chance the RBA delivers a rate cut in November (or a ~90% probability it happens by December) there could be a meaningful burst of AUD volatility around the Q3 CPI report. In our opinion, confirmation in the quarterly CPI that the inflation pulse remains firm might temper the markets enthusiasm about near-term RBA rate cuts, which if realised should be AUD supportive. This could be compounded by more positive US/China trade developments and/or another interest rate reduction by the US Fed (Thursday morning AEDT). As discussed above, we think downside US jobs market risks should see the Fed lower rates again and keep the door to open to more easing over future meetings.