• Market swings. Middle East conflict generated a burst of volatility overnight. Equities declined, oil prices rose. AUD traded in a ~2.5% range yesterday.

• Macro news. AU Q4 GDP today. RBA Gov. Bullock noted the March meeting is “live”. China PMIs also due. US ISM services & ADP employment out tonight.

Global Trends

The broadening conflict in the Middle East and concerns that it could drag on longer than the “4 to 5 weeks” touted by President Trump rattled market nerves overnight. Risk sentiment soured as ‘stagflation’ worries took hold given the prospect of a simultaneous slowdown in growth and jump in inflation stemming from higher energy prices. The US/Israel continue to strike targets in Iran, Iran continues to fire missiles and drones across the region, and there are lingering risks energy shipments via the Strait of Hormuz might be disrupted (~20% of global oil and LNG is transported via this route). That said, these concerns eased a bit after President Trump stated the US will escort and insure tankers and other vessels through the Strait “as soon as possible”.

In terms of markets, brent crude oil is tracking near ~US$81.50/brl, ~11.5% above where it closed last week but a few dollars below its intra-day highs after President Trump’s transport comments somewhat soothed fears. Gold declined (-4.5%) as did industrial metals like copper (-2.1%). Elsewhere, European equities underperformed (EuroStoxx600 -3.1%), in part due to the headwinds to the Eurozone economy from higher energy costs, and despite a late session reversal the major US equity markets shed ~1%. Bond yields rose with 10yr rates in the UK climbing ~10bps (now ~4.47%), while US rates are ~2-3bps higher across the curve. Markets are now only fully factoring in another US Fed rate cut by September, while traders see a ~33% chance the ECB will deliver a rate hike by year-end. Eurozone inflation was stronger than predicted in February with the energy price impulse a source of future upside risks. In FX, the USD strengthened with EUR tracking near the bottom of its 2-month range (now ~$1.1617). USD/JPY edged higher (now ~157.69) and GBP slipped back (now ~$1.3362). Closer to home, the NZD is at a multi-week low (now ~$0.5891) and the AUD (which traded in a wider than average ~2.5% range yesterday) lost ground (now ~$0.7042, though it had fallen to as low as ~$0.6945 intra-session).

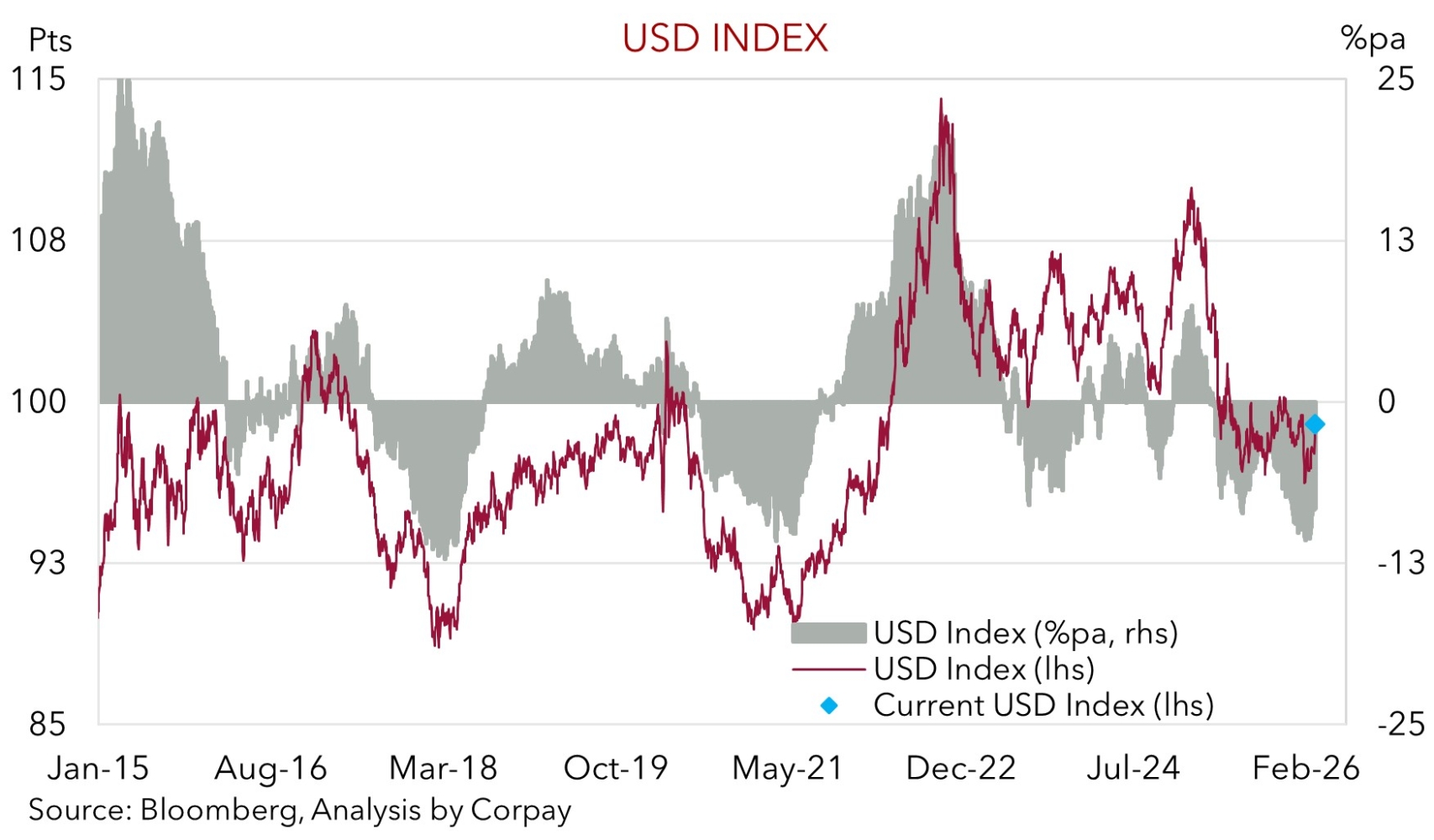

In addition to the unfolding Middle East developments there are still a number of important macro events on the horizon such as Australian GDP (11:30am AEDT), the China PMIs (12:30pm AEDT), US ADP employment (12:15am AEDT), the US ISM services index (2am AEDT), US retail sales, and the monthly US jobs report (both Friday night AEDT). In our opinion, signs of stabilization in US activity and/or labour market conditions may compound the geopolitical backdrop and help the USD extend its recovery, particularly as it is still below our ‘fair value’ estimate.

Trans-Tasman Zone

Domestic and global forces have generated an acute burst of AUD volatility over the past 24hrs. On the one hand, ‘hawkish’ comments from RBA Governor Bullock who noted that the 17 March meeting was “live” for a policy change boosted interest rate expectations and supported the AUD during yesterday’s Asian trade. More than a full 25bp RBA rate rise is now baked in by the May meeting with a move in March assigned a ~33% chance. However, the bout of risk aversion overnight saw the AUD reverse course quite sharply before soothing comments by President Trump about energy transport through the Strait of Hormuz saw risk assets rebound. That said, at ~$0.7042 the AUD is on net lower compared to where it was this time yesterday (and where it closed last week), with yesterday’s ~2.5% trading range more than double its long run average. The NZD was also whipped around, although not to the same extent as the AUD. On balance, the negative risk backdrop also weighed on the NZD which is around levels last traded in late-January (now ~$0.5891).

Today in Australia the Q4 GDP figures are out (11:30am AEDT), while in China the business PMIs are released (12:30pm AEDT). Based on the partial indicators that have been released over recent days, Q4 GDP looks like it could come in above the RBA’s and consensus predictions of ~0.8% quarterly growth. Confirmation that momentum quickened rather meaningfully in Q4, at a time the economy is already grappling with capacity constraints, could further reinforce views that the RBA will need to act again sooner rather than later. This might generate a bit of intraday AUD support. That said, while the 17 March meeting is ‘live’, at this stage we continue to think that the Board might want to wait until the 5 May meeting to gather a bit more information on the labour market/inflation and see how the Middle East conflict is playing out before acting again.

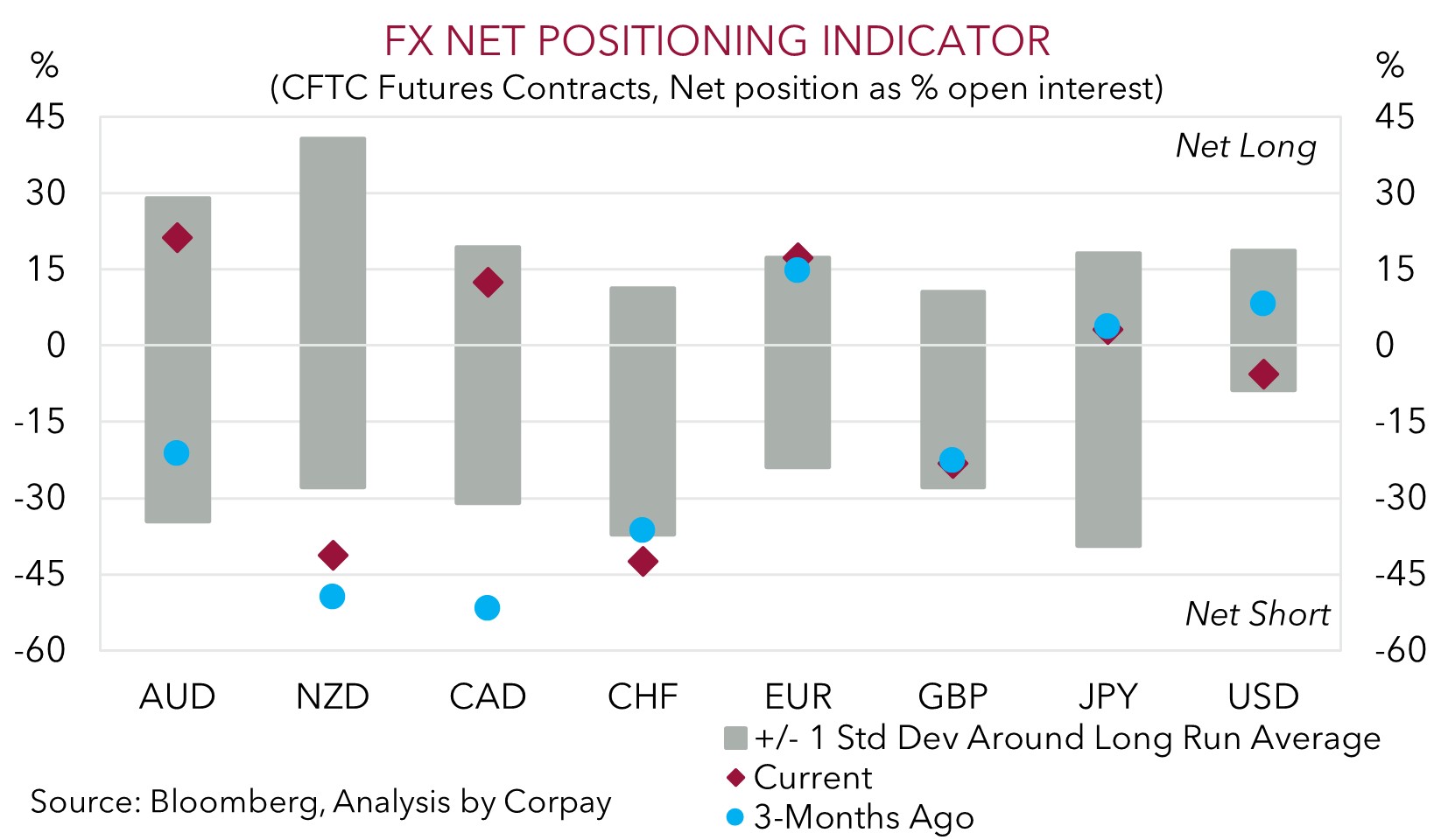

As outlined above, and early in the week, the situation in Middle East remains fluid and more bouts of AUD volatility are probable over the period ahead. While the outlook for further RBA rate hikes and more favourable interest rate differentials should act as an AUD cushion, the negative external risk environment is an offsetting force. Indeed, based on its strong start to the year, with it tracking above our model estimate (we see ‘fair value’ now closer to ~$0.6950), the shift in positioning to being ‘net long’ AUD (as measured by CFTC futures contracts), the negative growth/inflation implications for parts of Asia stemming from higher energy prices, and potential for the undervalued USD to claw back more lost ground, we believe there are more short-term downside than upside risks for the AUD.