Good morning. Oil prices are in the ascendant once again after another military escalation between the United States and Iran reignited fears of a prolonged disruption in energy shipments through the Strait of Hormuz. Both Brent and West Texas Intermediate are up roughly 2.5% after Revolutionary Guard units declared the strait closed to commercial shipping and fired on several vessels over the weekend, prompting a fifth round of American strikes and triggering Iranian retaliatory operations against US military facilities. Ten-year Treasury yields are roughly 2 basis points higher, equity futures are falling as the technology sell-off continues, and the dollar is weakening against a basket of its most-traded rivals for a fifth consecutive session.

Tomorrow’s US inflation report could shape expectations for the Federal Reserve’s next move. Headline consumer prices are expected to fall in month-on-month terms in June, driven largely by a sharp drop in gasoline prices after the signing of the US-Iran memorandum of understanding, with the year-over-year rate easing to 3.9% from 4.2%. Core inflation—far more important from a monetary policy standpoint—is seen rising at a pace similar to the prior month, bringing the annual rate down to 2.8% from 2.9%. Traders will be scrutinising the breadth of price increases—how many categories are running above target—for evidence that inflation pressures are broadening beyond energy. A widening in diffusion measures would strengthen the case for a hawkish stance from the Fed even as the headline rate moderates, while a narrowing would reinforce the view that the current overshoot is a supply-driven phenomenon the committee can afford to look through.

On Wednesday morning, Chair Kevin Warsh will testify before the House Financial Services Committee on the central bank’s semi-annual monetary policy report. Markets have thus far interpreted the newly-minted chair as a hawk, but at the European Central Bank’s recent gathering in Sintra, he noted that inflation expectations and risks had both fallen, and again suggested that if artificial intelligence expands the supply side of the economy, the implications for monetary policy would be significant—remarks that hinted at a more patient stance*.

The Bank of Canada is universally expected to hold rates on Wednesday for a sixth consecutive meeting, and its communications are unlikely to force a meaningful repricing of the expected policy path. Officials will reiterate their readiness to respond to risks on both sides, and repeat that the Bank is looking through the war’s near-term impact on headline inflation while remaining vigilant against a broadening in price pressures. The accompanying monetary policy report should point to improving economic momentum, a tightening in labour markets and a pickup in capital investment—a modestly encouraging backdrop that nonetheless leaves the Bank with no reason to move. Barring an unexpected misstep, market reaction should be muted.

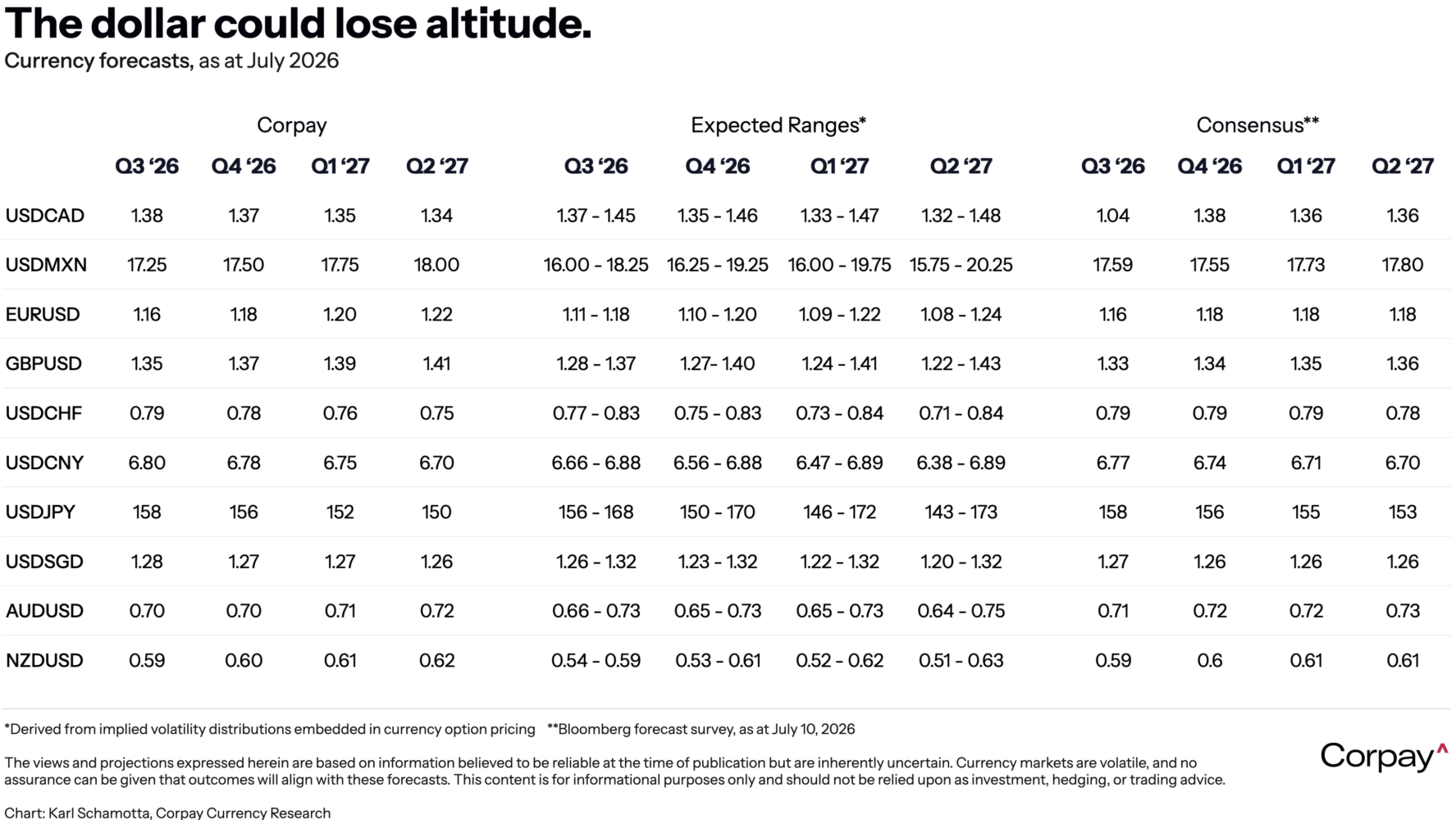

More broadly, currency markets are in mean-reversion mode, with many participants rebalancing exposures away from the dollar. We think this reflects a wider reappraisal of overvaluation risks in American equity markets, growing scepticism about the strength of the US economy, and doubts about the durability of the Fed’s hawkish turn. We have updated our forecasts** to reflect a modest easing in the dollar’s strength over the coming quarters.

The case for a softer dollar rests on several converging forces. In our view, American inflation should ease more quickly than markets expect as tariff increases slow and the oil shock fades, keeping the Fed sidelined. The labour market’s headline resilience flatters: most new jobs are coming from healthcare and education, not private employers, and that hiring looks set to cool. A rotation out of frothy artificial-intelligence stocks threatens the foreign capital inflows that have been propping up the greenback, and looming midterm elections promise policy turbulence without the credible tariff threats that had previously hurt other currencies. Meanwhile, other advanced economies are showing nascent signs of steadying. Confidence is reviving, and data may increasingly beat the gloomy expectations now embedded in the euro, pound and loonie,

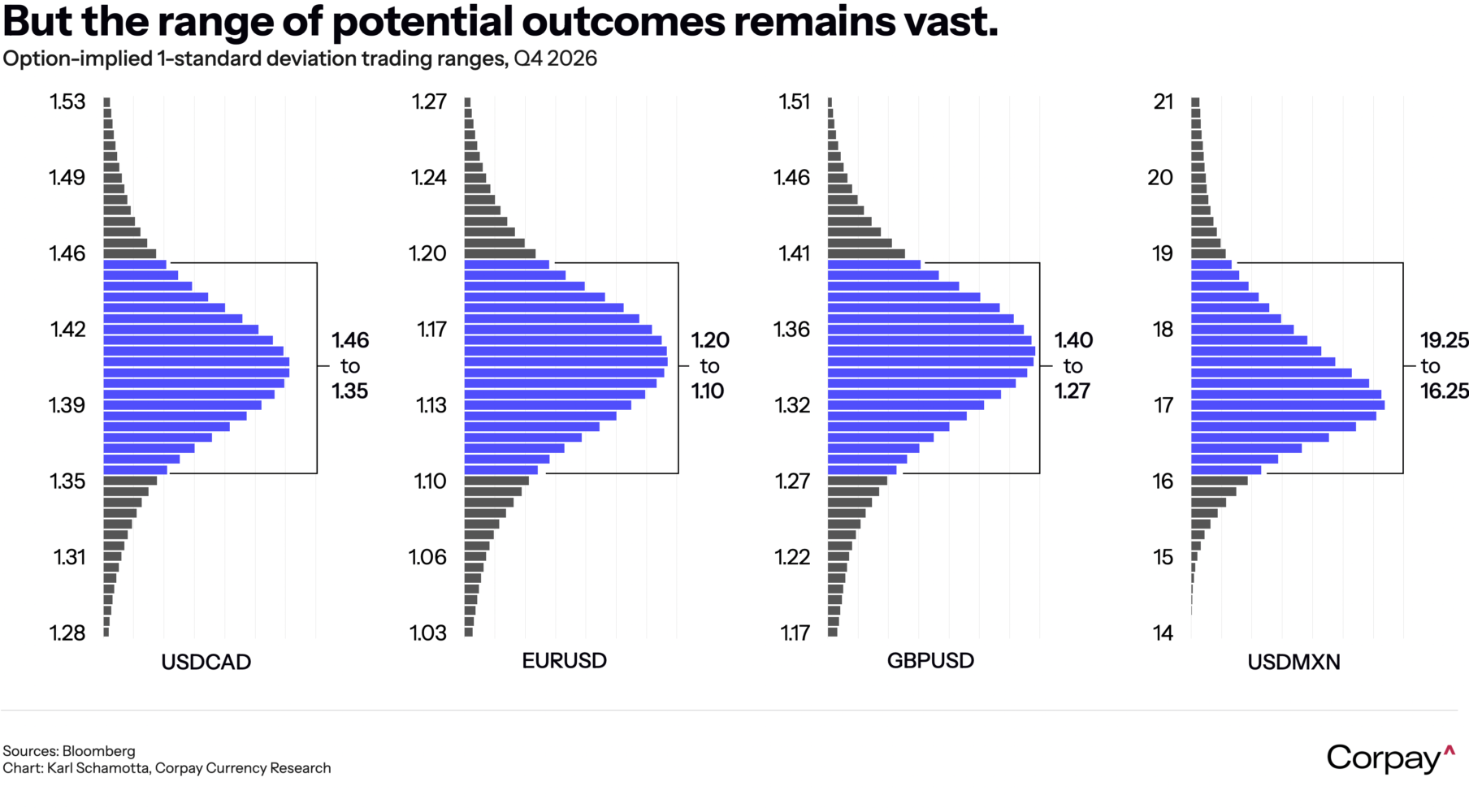

However, in line with the caveats set out in last week’s market note, it is important to recognise that this environment is not conducive to linear forecasting***. The direction of oil prices, shifts in the expected path of interest rates, relative growth prospects, changes in positioning, and political developments could each overwhelm the slow-moving forces described above. Option-implied distributions suggest a wide range of potential outcomes in the quarters ahead. Hedgers should plan accordingly.

*Warsh will undoubtedly seek to keep his cards close to his chest, but Congress has a tendency to bring out the worst in people. Surprises are quite possible.

**You can always find our updates, including cross rates here.

***It frankly never is.