• Conflict concerns. Risk sentiment negative. Oil prices higher. Equities lower. USD edging up. AUD & NZD on the backfoot. AUD ~4.7% from its March peak.

• Global economy. More volatility likely. Impact on world economy from energy supply shock still in the pipeline. Cyclical/growth-linked assets under pressure.

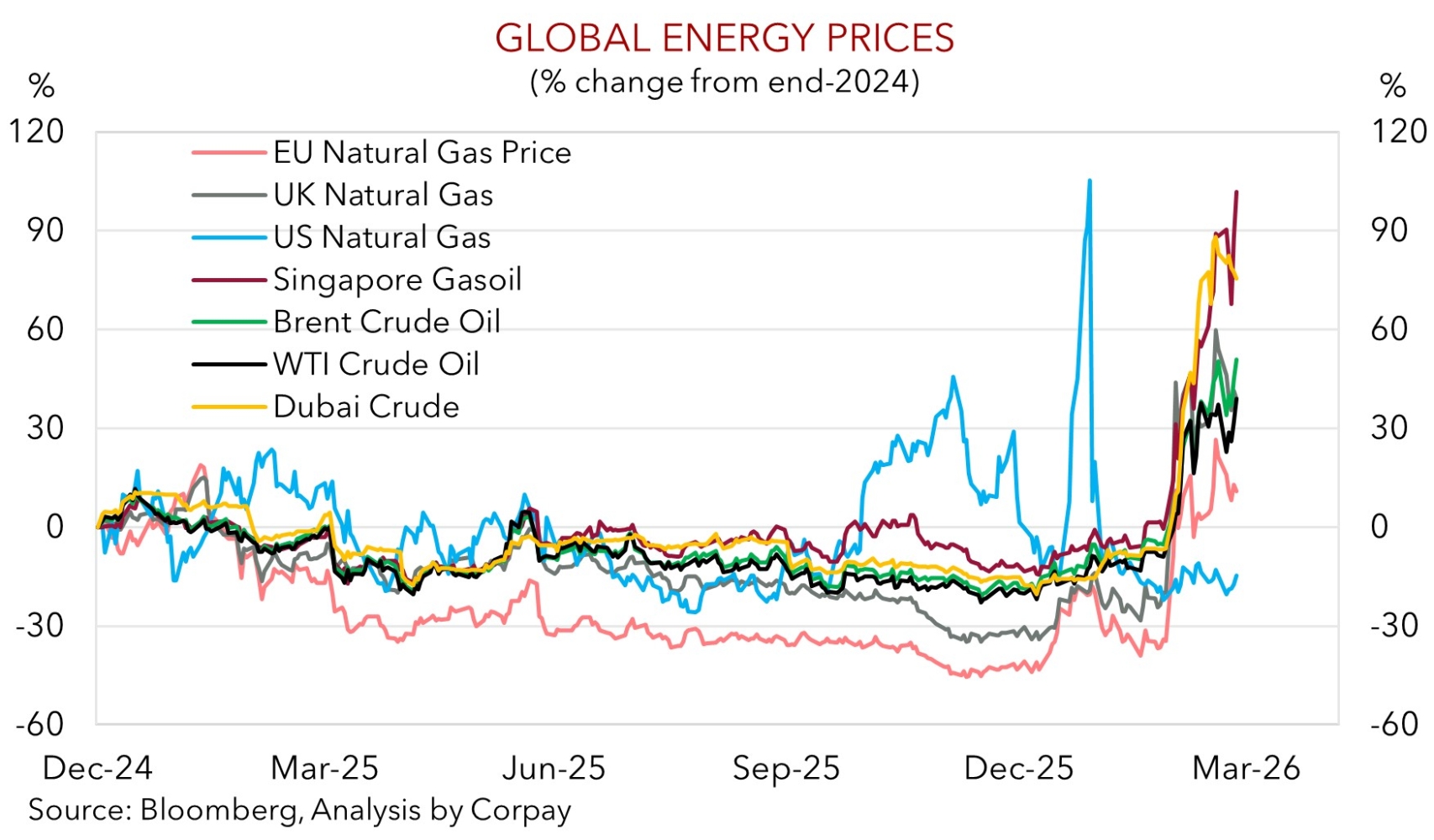

Global Trends

Middle East related nervousness kept sentiment negative at the end of last week. Worries the conflict (which is now in its 5th week, and showing no signs of improving) will generate a “stagflationary” environment for the world economy (i.e. higher inflation and slower growth) are front of mind. The Strait of Hormuz, the shipping route where ~20-25% of global energy flows through, remains effectively shut. The US’ decision to push back the ‘deadline’ for potential strikes on Iranian energy infrastructure to 6 April has done little to reduce uncertainty, particularly as both sides remain on the offensive, and there are increased odds of disruptions to Red Sea shipping following Houthi attacks over the weekend.

In terms of markets, global equities extended their selloff on Friday with the US S&P500 shedding another ~1.7%. The S&P500 is now ~8.9% from its mid-February peak with the index declining in 7 of the past 8 weeks (its worst run since mid-2022). Energy prices rose as a greater supply premium was baked in with Brent crude oil tracking near US$112.60/brl (~93% above its December low). And while interest rate expectations/bond yields remain elevated there was a bit of a paring back as investors begin to shift focus from upside inflation to downside growth concerns. This was also observed via the widening in credit spreads. In FX, the backdrop continues to underpin the USD with EUR slipping towards ~$1.15 and USD/JPY touching its highest point since July-2024 (now ~160.23). Cyclical currencies like the NZD (now ~$0.5751) and AUD (now ~$0.6866) remain on the backfoot.

Looking ahead, Good Friday is a public holiday in Australia/NZ and across much of Europe. In the US, although equity and bond markets will be closed, economic data is still published. The monthly US jobs report is due on Friday, but markets will have to wait until next week to react to the news with analysts predicting a modest rebound in employment and stable unemployment rate in March after weak figures in February. Ahead of that, US Fed Chair Powell speaks (tonight 1:30am AEDT), the China PMIs are due (Tues), and in the US JOLTs job openings (Tues night AEDT), retail sales and ISM manufacturing survey (both Weds night AEDT) are out. That said, developments in the Middle East look set to remain in the driver’s seat. More twists and turns that impact short-term sentiment should be anticipated. However, we would also stress that the fallout across the real economy is only in its infancy. Disruptions to energy supply might take months/quarters to clear up, and this will only begin to improve once the conflict ends. We believe fragile risk sentiment coupled with the higher level of oil prices (because of the US’ ‘net energy exporter’ status) should continue to be USD supportive over the short-run.

Trans-Tasman Zone

The negative risk sentiment stemming from the ongoing conflict in the Middle East, worries about global growth due to higher energy prices, and a firmer USD are keeping the NZD and AUD under pressure (see above). At ~$0.6866 the AUD is at a ~2-month low and ~4.7% from the multi-year peak touched in early March. The NZD (now ~$0.5751) is at its lowest level since January, and more than 1 cent below its 1-year average. The backdrop is also weighing down the AUD on the cross-rates with falls of ~0.1-0.3% recorded against the EUR, NZD, CAD, and CNH. At ~0.5970 AUD/EUR is at a 1-month low, while AUD/CNH (now ~4.7525) is drifting towards its 200-day moving average.

Locally, the minutes of the March RBA meeting are released this week (Tues). The cash rate was increased by 25bp to 4.10% earlier this month, however it was a close 5-4 vote. The minutes might give more colour on the debate among Board members, and why some wanted to wait until the next meeting to move rates. Beyond that there are no economic releases which are typically market moving due until after the Easter holiday period.

As outlined previously the surge in oil/fuel will mechanically propel Australian headline inflation much higher in March/April. After that there may be spillovers across other parts of the CPI basket like airfares, and if firms in fuel-intensive industries such as agriculture, logistics, construction, and manufacturing pass on higher costs. Given inflation was already problematic, the RBA should deliver at least 1-2 more rate rises, in our view. Markets continue to factor in more RBA action with the odds of a May hike now assigned a ~74% chance, and ~75bps of tightening factored in by November. As discussed, more twists and turns are likely in the Middle East, and a lot of the negative economic impacts are still yet to show up. As we repeatedly warned the past month, there are more downside than upside risks for the AUD in the near-term. We remain of the opinion that based on the fragile situation in the Middle East, how much more RBA tightening is already discounted, the looming global growth slowdown, and with the negative domestic consequences of higher mortgage rates and fuel costs still in the pipeline the AUD could remain on the backfoot.