• Mixed signals. Sanctions on Russian producers boosted oil prices. Limited spillover into other markets. Equities rose. AUD outperformed overnight.

• US inflation. US CPI due tonight. US government shutdown delayed it. Diverging ‘goods’ & ‘services’ price trends at play. Data may generate USD vol.

Global Trends

Geopolitical developments generated a little volatility across a few markets overnight, though risk assets are generally firmer. US sanctions on some of Russia’s largest oil producers due to the lack of commitment to end the Ukraine war saw oil prices rise ~5%. That said, at ~$66/brl brent crude is still tracking below its 1-year average. Russia accounts for ~12% of global oil supply with a large chunk of its exported product sent to India and China. While the latest news may generate a bit of a geopolitical risk premium, a substantial/sustained jump higher in prices doesn’t look likely, in our view. At last count the global oil market was in a state of ‘excess supply’ with softer growth constraining demand at a time supply has been picking up.

Higher oil prices dragged up bond yields with the benchmark US 10yr rate climbing ~5bps. But at ~4% the US 10yr is still hovering around the lower end of its multi-month range. There was no real spillover into equities with European and US stock markets posting gains overnight. Lead by the tech-sector (NASDAQ +0.9%) the S&P500 ticked up ~0.6% with sentiment somewhat boosted by news President Trump will meet China’s President Xi on 30 October on the sidelines of the APEC summit. The meeting comes as a trade truce between the US and China is set to expire on 10 November. In FX, the USD index consolidated with gains against the JPY offset by a steady EUR (now ~$1.1618) and weaker GBP (now ~$1.3327). USD/JPY (now ~152.58) is approaching the top end of the range occupied since mid-February. We believe USD/JPY is looking stretched compared to underlying drivers such as yield spreads. Elsewhere, the backdrop helped cyclical currencies such as the NZD (now ~$0.5749) and AUD (now ~$0.6510) edge up.

The US Government Shutdown remains in place with the current iteration the second longest in history. The shutdown has played havoc with official US statistics with several releases put on hold. But with CPI inflation an important input into Social Security cost-of-living adjustments staff have been recalled to release the delayed September data tonight (11:30pm AEDT). We believe more tariff related impacts might show up in US ‘goods’ prices, and higher gas prices may boost headline CPI. However, softness in a few ‘services’ areas could be a more powerful force that sees core inflation undershoot forecasts. ‘Goods’ prices account for ~19% of the US CPI basket, while ‘services’ equate to ~60%. If realised, we believe this can reinforce the case for the US Fed to deliver another rate cut next week and more easing over future meetings given the US labour market wobbles. In our opinion, this could exert downward pressure on the USD, as would signs of slower US growth momentum in the latest business PMIs (Eurozone 7pm AEDT, US 12:45am AEDT).

Trans-Tasman Zone

The more upbeat tone in risk assets, as illustrated by firmer equites, and higher commodity prices supported cyclical currencies such as the NZD and AUD overnight (see above). At ~$0.5749 the NZD is close to its 1-month average while the AUD (now ~$0.6510) is near the middle of the range occupied since late-May. The backdrop also helped the AUD outperform on the cross-rates with gains of ~0.3-0.6% recorded against EUR, GBP, CAD, and CNH over the past 24hrs. There has been a larger rise versus the JPY (+0.8%) with AUD/JPY (now ~99.35) not that far from its year-to-date peak. AUD/NZD (now ~1.1322) remains elevated with relative economic and interest rate trends still firmly in Australia’s favour, in our view.

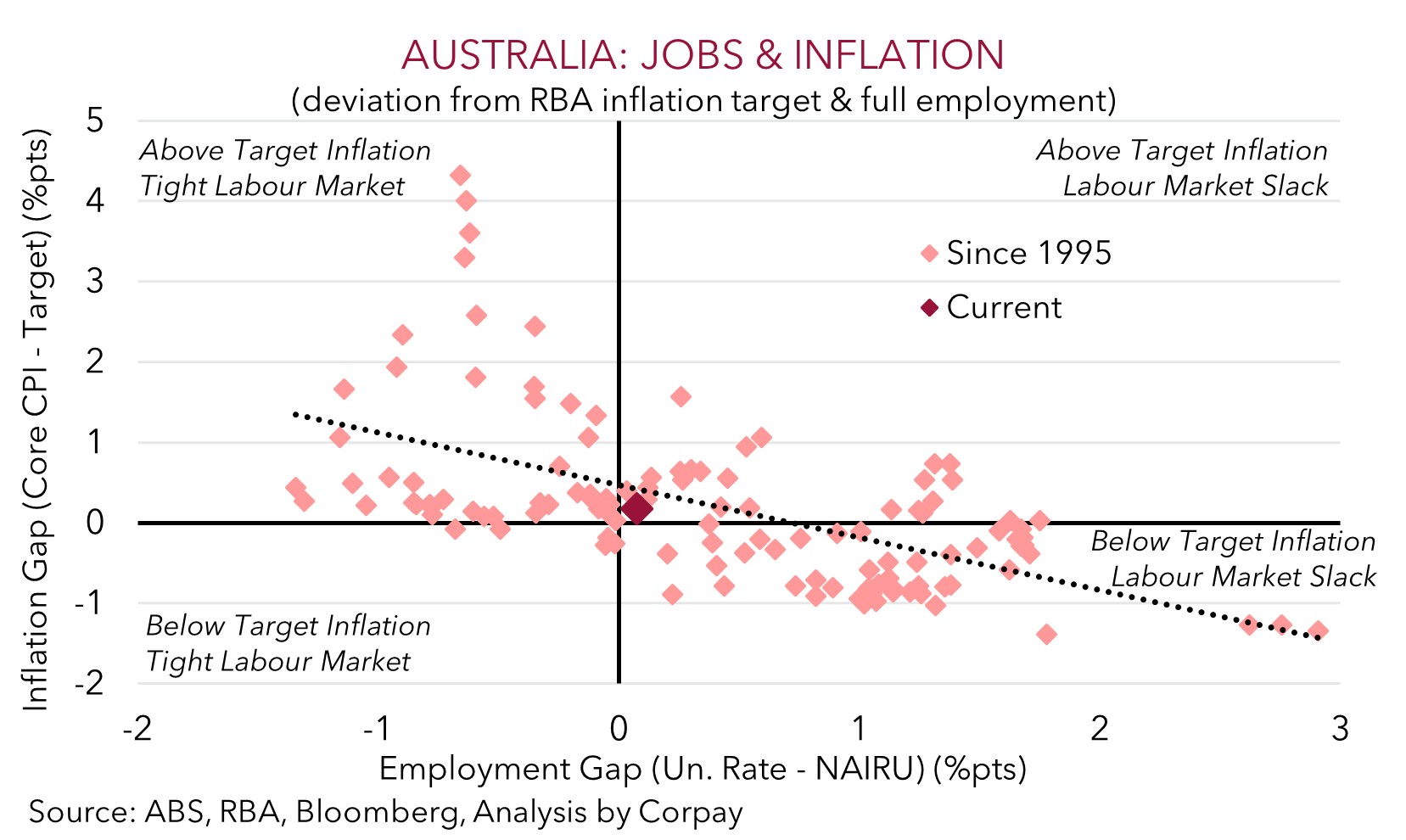

RBA Governor Bullock speaks today (11:05am AEDT). The event has a Q&A so there may be opportunity to gauge Governor Bullock’s thoughts on the tension between inflation and labour market developments. As our chart shows, it is an interesting time with core inflation still lingering above the RBA’s target while labour market conditions are cooling. On the latter, as outlined earlier this week, we think markets may have jumped to aggressively to last week’s jobs report and are pricing in too high a chance of a RBA rate cut in November (the market is assigning it a ~60% probability). In our judgement, broader measures don’t show a significant loosening in the jobs market with the average of the unemployment rate over Q3 broadly in line with the RBA’s ~4.3% projection. Furthermore, based on the monthly indicator Q3 inflation (due 29 October) may come in above the RBA’s forecasts. We think confirmation in the quarterly CPI that the inflation pulse remains firm could temper the markets enthusiasm about near-term RBA rate cuts, which if realised may give the AUD a helping hand.

That said, ahead of the quarterly Australian CPI the AUD (and NZD) will have to contend with tonight’s US inflation data (11:30pm AEDT). As mentioned above, we think US core inflation risks underwhelming consensus predictions because of ‘services’ prices. If this ends up being the case we think expectations looking for a series of US Fed interest rate cuts should be reinforced and this in turn might generate downward pressure on the USD.