• Risk reversal. Comments by Pres. Trump saw oil prices fall & sentiment improve. USD weaker. AUD ticked up, but AUD also underperforms on crosses.

• Fragile markets. Situation in Middle East remains fluid. More volatility likely. Impact on global economy from the energy supply shock still in the pipeline.

Global Trends

Markets continue to be whipped around by developments in the Middle East, although the mood and moves were more positive overnight on the back of a shift in thinking that the conflict could be nearing an end. Yesterday’s bout of risk aversion reversed course when, just before US markets opened for trading, President Trump posted that the US and Iran have had “very good and productive conversations regarding a complete and total resolution” of hostilities, and as a result military strikes against Iranian power plants and energy infrastructure have been postponed for five days. Officials from Iran denied they had been in talks, however media reports indicating other nations (particularly around the region) are attempting to deescalate the war and comments by officials such as the UK Prime Minister they are “aware of negotiations” suggest there is truth to it.

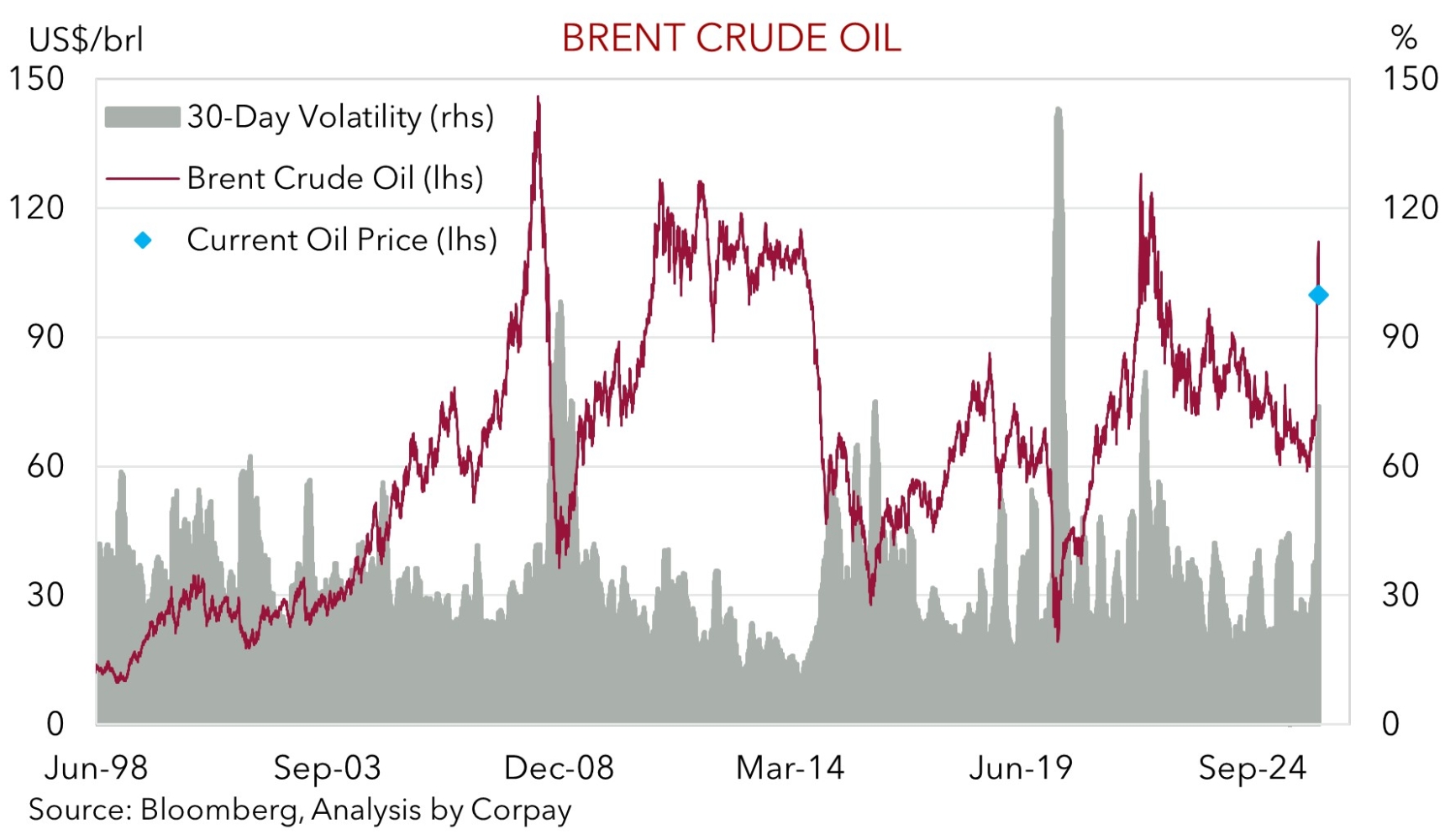

Markets often hear what they want to hear. Because of the news there was a sharp drop in energy prices (Brent crude fell 11%, though as our chart shows at ~US$101/brl it remains at a high level). Bond yields declined as inflation concerns were modestly unwound with US rates falling ~4-5bps across the curve. But much like oil this only partially retraces recent moves with the US 10yr yield (now ~4.34%) still in the upper end of its multi-month range. Equities rose, however some of the initial knee-jerk euphoria faded as time rolled on with the S&P500 ending the day ~1.2% higher (still ~5.4% below where it was at the start of February). In FX, the USD index lost ground with EUR climbing over ~$1.16 and USD/JPY dipping towards ~158.40. The NZD strengthened (now ~$0.5859), although it is only back where it has tracking on Friday. The AUD nudged up to where it closed last week (now ~$0.7011) but the relatively stronger recovery in most other currencies meant it underperformed on the crosses.

As outlined before, and observed yesterday/the past month, the situation in the Middle East is fluid and will be an ongoing source of volatility. Sentiment has improved but things remain fragile. More twists and turns are likely. Indeed, the fallout across the real economy is in its infancy. The disruption to energy supply might take months/quarters (or even years in some markets) to resolve, not days/weeks. The scar tissue from unfolding events may not heal for some time. Hence, downside risks for global growth and upside risks for inflation remain. This is normally a tricky environment for cyclical assets. Bursts of volatility, coupled with the higher level of oil prices (because of the US’ ‘net energy exporter’ status) can be an underlying support for the USD for a while yet, in our opinion.

Trans-Tasman Zone

The relatively more upbeat market mood, stemming from the various comments (particularly those by President Tump) which have raised the chances of a resolution to the conflict with Iran, have generated some support for the NZD and AUD (see above). At ~$0.5859 the NZD is back where it was tracking on Friday and broadly in line with its 1-year average. In her latest speech new RBNZ Governor Breman noted policymakers won’t rush to raise rates in response to the Middle East conflict as a “short-lived disruption” can be “looked through” and changes in rates generally take ~6-9 quarters to impact domestic inflation. Markets are pricing in a full RBNZ rate rise by the July meeting, with ~3 hikes discounted by December.

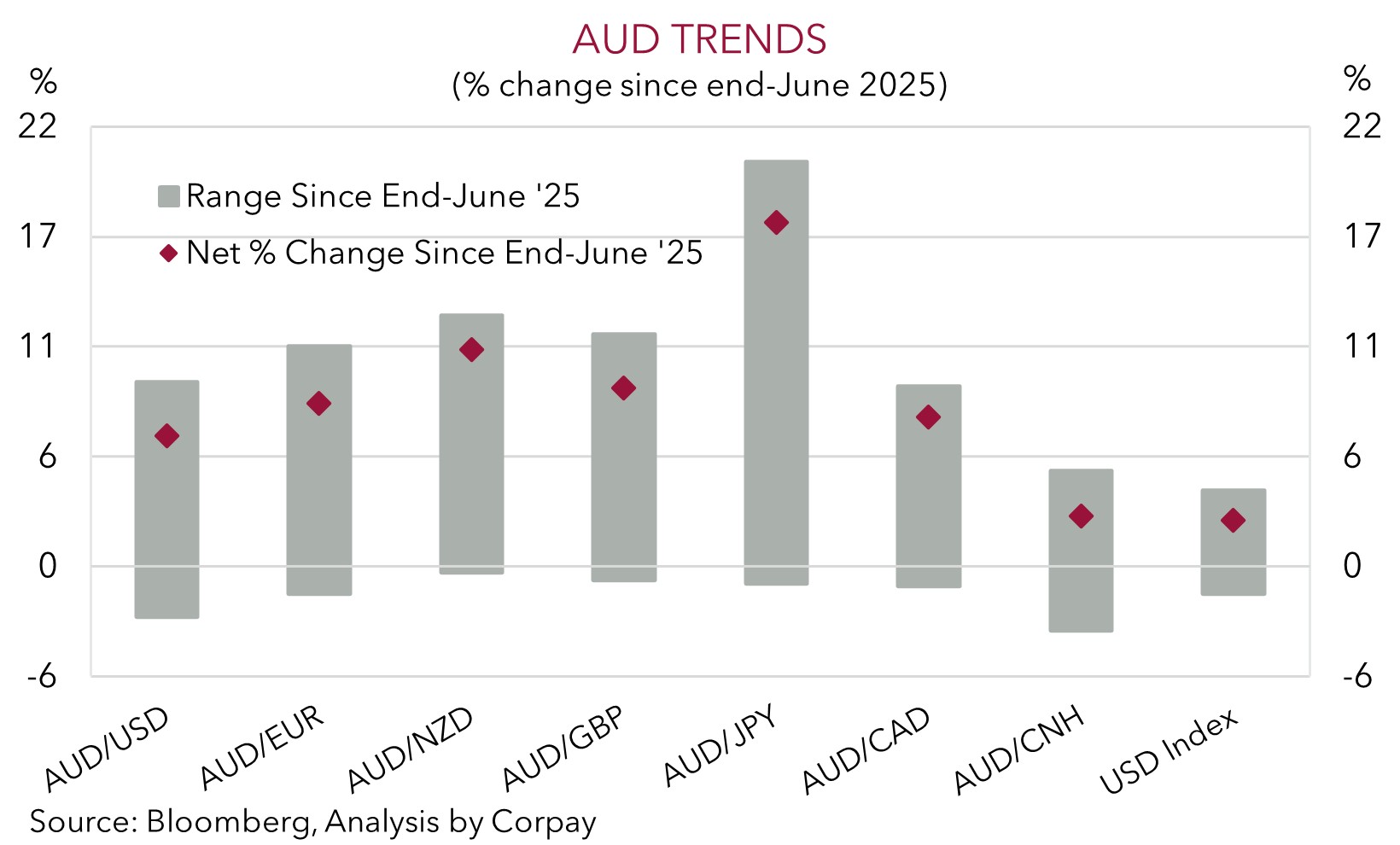

The AUD has traded in a wider than average ~2.2% range over the past 24hrs, but on net it has ticked up to where it ended last week (now ~$0.7011). Relative weakness on some of the major cross-rates due to a stronger rebound in other currencies has acted as an AUD headwind. The AUD has weakened by ~0.4-0.8% versus the EUR, JPY, GBP, and NZD compared to this time yesterday, with AUD/CNH slipped back ~0.1%.

Locally, the next major macro signpost is tomorrow’s monthly CPI figures for February (Weds 11:30am AEDT). The data predates the Middle East conflict, hence the surge in petrol/fuel prices will only start to show up in next month’s release. The jump in petrol will mechanically propel headline inflation much higher in March/April. After that there could be spillover impacts across other parts of the CPI basket like airfares, and if firms in fuel-intensive industries such as agriculture, logistics, construction, and manufacturing start to pass on higher costs. Markets are factoring in a ~60% chance of another RBA rate hike in May, with ~71bps of tightening baked in by year-end.

The improvement in risk sentiment might give the AUD some more near-term support, in our view. However, as mentioned, more twists and turns are likely in the Middle East, and the negative economic impacts are still in the pipeline. Upside potential in the AUD looks to be capped. We remain of the opinion that based on how much more RBA tightening is priced into the Australian interest rate curve, the fragile situation in the Middle East, the looming global growth slowdown, and with the negative domestic economic consequences of higher mortgage rates and fuel costs still yet to manifest, there are more short-term headwinds than tailwinds for the AUD. Added to that, the AUD is ~2% above our ‘fair value’ estimate, and higher than where various yield/interest rate differentials suggest it should be.