• Negative vibes. Ongoing concerns about the Middle East conflict weighed on sentiment. Equities lower, oil & yields higher. USD firmer. AUD under pressure.

• Twists & turns. Situation in Middle East remains uncertain. More volatility likely. Impact on world economy from energy supply shock still in its infancy.

Global Trends

Middle East related concerns weighed on risk sentiment once again with markets questioning the chance of a diplomatic solution to end the conflict. According to various reports, the US has proposed a 15-point peace plan and is aiming for a quick resolution, while Iran responded with its own 5-point. The two sides still look far apart. That said, in a glimmer of hope, after ramping up threats of new military action President Trump announced talks are going “very well” and the deadline for Iran to strike a deal and avoid the US “obliterating” its energy infrastructure has been extended by 10 days to 6 April. The situation is clearly in flux. Time will tell if this latest deadline holds or is pushed out again.

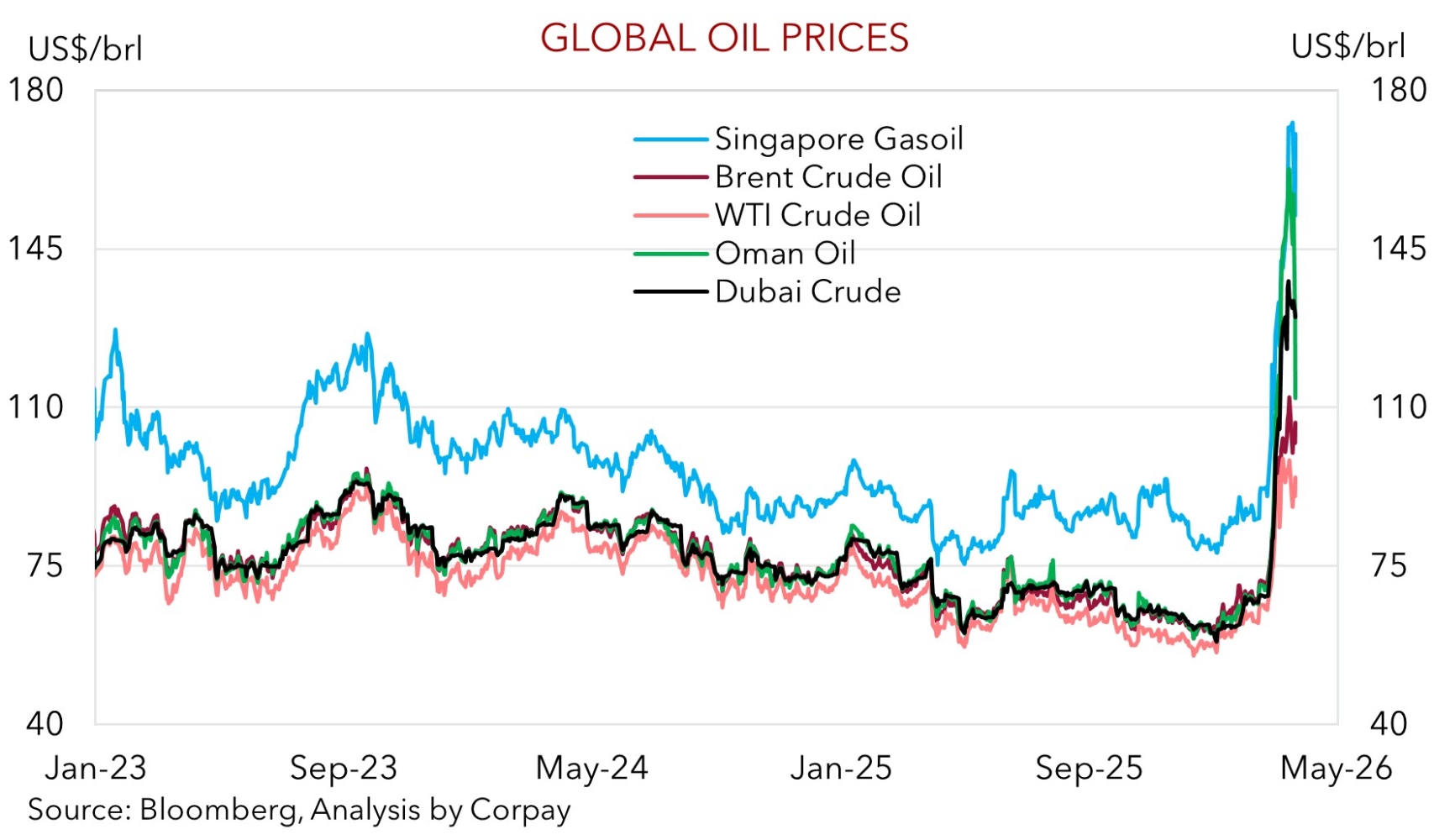

In response to the nervousness about the conflict and what the disruptions to global energy markets might do to the global economy energy prices rose (Brent crude is back up near US$107/brl); equities fell (the S&P500 declined 1.7%, and is now ~7.3% from its February peak); bond yields increased due to heightened inflation risks and upward repricing in interest rate expectations; and in FX the USD edged up. EUR has slipped back (now ~$1.1527), as has GBP (now ~$1.3331), while USD/JPY ticked slightly higher (now ~159.69). Cyclical currencies such as the NZD (now ~$0.5762) and AUD (now ~$0.6890) lost altitude.

As discussed/observed repeatedly over the past month, the situation in the Middle East is fluid and will be an ongoing source of market volatility for a while. More twists and turns that impact short-term sentiment are likely. However, we would also note that the fallout across the real economy is only in its early stages. The disruption to energy supply might take months/quarters (or even years in some instances) to clear up, not days/weeks. The scar tissue from unfolding events may not heal for an extended period. As a result, downside risks for global growth and upside risks for inflation remain in place. This is normally a challenging environment for cyclical assets. We believe fragile risk sentiment combined with the higher level of oil prices (because of the US’ ‘net energy exporter’ status) should continue to be USD supportive over the near-term.

Trans-Tasman Zone

Jitters about the global economy because of the ongoing conflict in the Middle East, elevated energy prices, and disrupted energy supply weighed on risk sentiment overnight (see above). This, and the firmer USD, exerted more downward pressure on the NZD and AUD. At ~$0.5762 the NZD is at its lowest point since mid-January and about 1 cent below its 1-year average. The AUD (now ~$0.6890) is ~4.1% from its early-March cyclical peak and at levels last traded in late-January. The backdrop also saw the AUD underperform on the crosses with falls of ~0.5-0.7% recorded against EUR, JPY, GBP, CAD, and CNH. In level terms AUD/EUR (now ~0.5975) is at a 1-month low, as is AUD/GBP (now ~0.5169), while AUD/CNH (now ~4.7659) is approaching its 100-day moving average.

The Australian economic data calendar is light over the period ahead, with no releases that are typically market moving due until after the Easter holiday period. Markets continue to price in more RBA interest rate rises with the odds of a move in May now assigned a ~70% chance, and ~70bps of additional hikes factored in by year-end. When speaking yesterday RBA Assistant Governor Kent (who isn’t a voting Board member) stressed the Middle East conflict risks further fueling price pressures across the Australian economy and that policymakers are “very much focused on inflation”. As outlined previously the jump in petrol will mechanically propel Australian headline inflation much higher in March/April. After that there could be spillover impacts across other parts of the CPI basket like airfares, and if firms in fuel-intensive industries such as agriculture, logistics, construction, and manufacturing start to pass on higher costs.

As mentioned, more twists and turns are likely in the Middle East, and a lot of the negative economic impacts still haven’t manifested in the real world. As we repeatedly warned the past few weeks, there are more downside than upside risks for the AUD in the near-term. We remain of the view that based on how much more RBA tightening is factored into the interest rate curve, the fragile situation in the Middle East, the looming global growth slowdown, and with the negative domestic economic consequences of higher mortgage rates and fuel costs still in the pipeline the AUD may remain on the backfoot for a while yet.