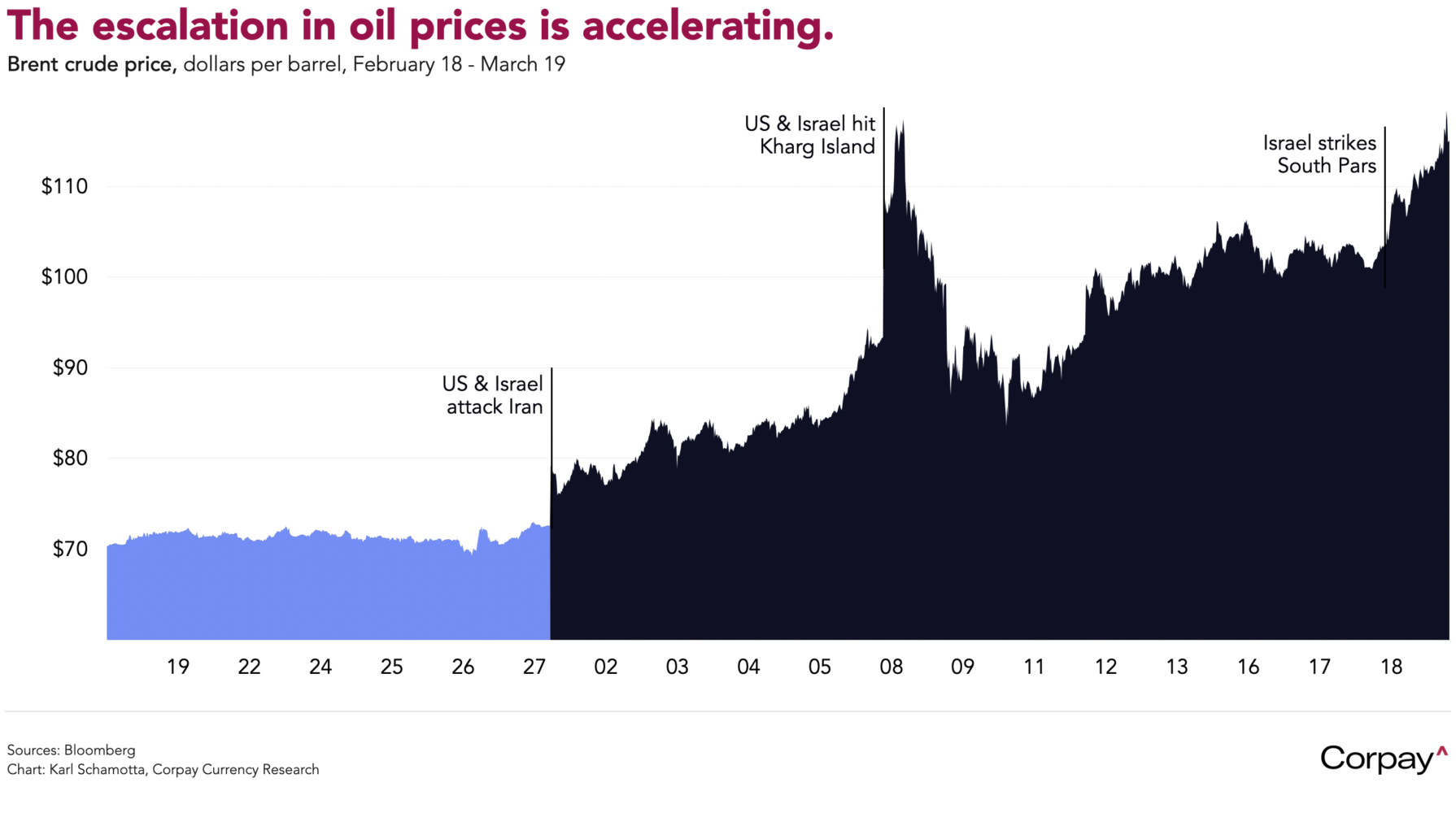

Global energy benchmarks are approaching last weekend’s panic-driven highs as the Middle East conflict shows signs of spiralling out of control. Brent is trading above $115, West Texas Intermediate is flirting with $100, and European natural gas futures are up another 25 percent after Iran struck infrastructure targets in Kuwait and Saudi Arabia and carried out missile attacks on critical natural gas facilities in Qatar, causing what officials described as “significant damage” in retaliation for yesterday’s Israeli strike on the South Pars gas field. Treasury yields are pushing higher, US equity markets are in retreat, and the dollar is holding firm as measures of implied volatility climb.

Grappling with the mounting economic and political costs of the conflict, President Trump made an apparent effort to defuse the situation in a social media post last night. On Truth Social, he claimed the “United States knew nothing about this particular attack”, and said Israel would not repeat it, but then threatened to “massively blow up the entirety of the South Pars Gas Field at an amount of strength and power that Iran has never seen or witnessed before” if the Iranians hit Qatar again. The war has driven a sharp rise in gasoline costs, is historically unpopular, and is imposing a rapidly-ballooning toll on the US fiscal position: the Pentagon has reportedly requested a $200 billion supplemental budget increase—enough to wipe out most of the tariff revenue collected over the past year, even before refunds are issued.

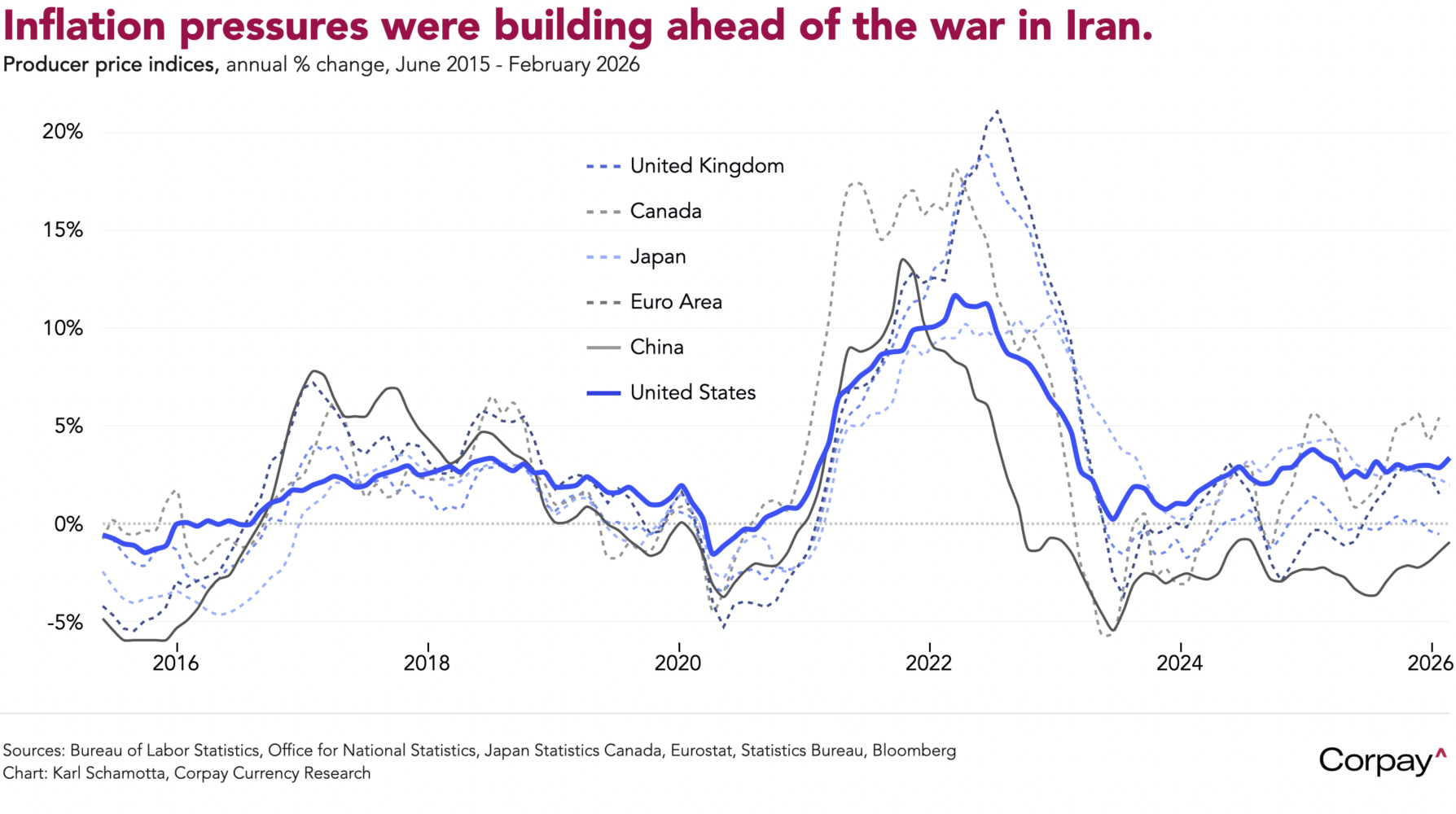

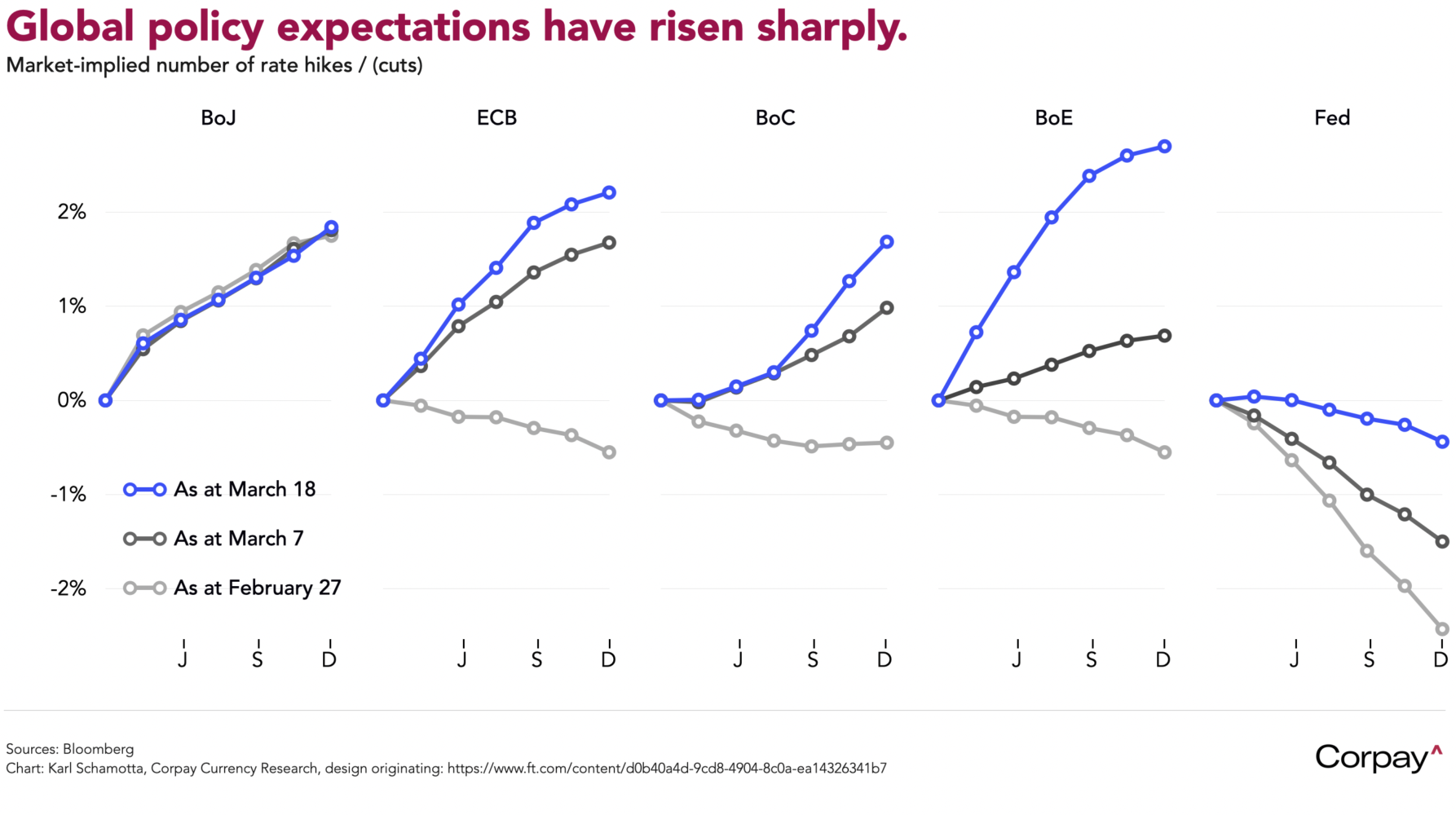

The Federal Reserve appears intent on waiting for clarity on the conflict’s impact before adjusting its policy stance. The dot plot accompanying yesterday’s decision was less hawkish than markets had feared: 12 of 19 officials still see at least one cut this year, unchanged from December. Chair Powell, however, noted that inflation was coming down more slowly than anticipated—data published earlier in the day showed producer prices rising at nearly twice the expected pace before the war—said rates were already near neutral, and warned that “several” participants thought the next move could be an increase. Higher energy prices would push up headline inflation, he acknowledged, though it was too soon to gauge the scope and duration of the economic effects. More pointedly, he suggested that a sequence of temporary supply shocks—of the kind that have buffeted the economy since the pandemic—could gradually destabilise inflation expectations and ultimately necessitate tighter policy.

Canada’s central bank took a different tack in yesterday’s decision, opting to emphasise the economy’s weakness as a counterweight to higher energy prices. Governor Tiff Macklem pledged to look through the war’s immediate impact on headline inflation, noting that the risk of higher energy costs spreading quickly to other goods and services looked contained while domestic demand remained subdued. The Canadian dollar softened modestly in the hours after the announcement as rate differentials widened against it, and now looks likely to follow historical patterns in exhibiting a weaker correlation with oil prices at elevated levels.

The yen is trading with a slightly firmer bias after the Bank of Japan left its policy rate unchanged as expected and struck a decidedly-hawkish tone, keeping an April hike in play. Governor Kazuo Ueda acknowledged risks on both sides of the inflation outlook, but appeared relatively sanguine on the likelihood of an energy-driven growth shock, suggesting the board is tilting toward prioritising price stability as the fallout from the Iran war ripples across the economy. In an unusual step, the policy statement included explicit language reaffirming the bank’s intention to continue raising rates if prices evolve in line with forecasts—a signal that, combined with Ueda’s insistence that every meeting remains “live,” left little doubt about the direction of travel.

The British pound is trading sharply higher after the Bank of England turned unmistakably hawkish, saying that it “stands ready to act” should energy prices feed through into broader inflationary pressures—marking a dramatic pivot from February’s guidance that rates were “likely to be reduced further”. The shift was underscored by Swati Dhingra, one of the Bank’s most reliably-dovish voices, conceding that a rate rise may prove necessary if the energy supply shock persists. Swap markets are now pricing in two quarter-point increases by year-end, and gilt yields are climbing as rate differentials tilt back in the pound’s favour.

Across the Channel, the euro is marking time ahead of this morning’s rate decision, which is likely to leave policy expectations anchored well above pre-war levels. President Christine Lagarde is expected to follow Jerome Powell’s lead in striking a cautious, non-committal tone, and fireworks in currency markets look unlikely. For now, energy markets will remain the dominant force driving price action in the euro.

Bottom line: Even as most central bankers have given short shrift to soaring energy prices, policy expectations have climbed sharply across most advanced economies since the war’s outbreak nearly three weeks ago, forcing interest rates higher, tightening financial conditions, and triggering significant moves in currency markets. This looks unlikely to last. Energy markets have the potential to become truly dislocated if the current level of disruption persists, and the political consequences for the Trump administration could grow untenable. That said, there is little evidence of serious planning for the economic fallout, none of the combatants are showing signs of stepping off the escalation ladder, and the conflict could drag on far longer than almost anyone predicted at the outset. For now, hedgers should take a page from the central bank playbook: position for an eventual normalisation in rates, while taking out tail-risk insurance against bigger moves.