Financial markets are turning cautiously optimistic this morning as oil prices stabilise and investors position for a raft of central bank decisions. Several tankers registered to non-aligned countries crossed the Strait of Hormuz overnight, even as Iran continued its attacks on Israel and its Gulf neighbours, while Donald Trump said the US could end the war in the “very near future”*. West Texas Intermediate is trading below $95 a barrel, Brent at $103, equity futures are pointing to a second consecutive daily advance, Treasury yields are slipping, and the dollar is edging lower against a basket of its major counterparts.

Foreign exchange and rates traders will be on tenterhooks over the next 48 hours as monetary policymakers weigh the competing forces unleashed by the war. Following the Reserve Bank of Australia’s rate increase earlier this week, all six remaining major advanced-economy central banks—the Federal Reserve, Bank of Canada, Bank of Japan, Swiss National Bank, Bank of England, and European Central Bank—will deliver decisions and set out their views on how the balance of growth and inflation risks is evolving. In our view, today’s energy shock is more likely to destroy demand than to create it, and the traditional monetary policy playbook—which suggests looking through commodity price spikes to still-weak underlying economic fundamentals—should dominate communications strategies in most cases.

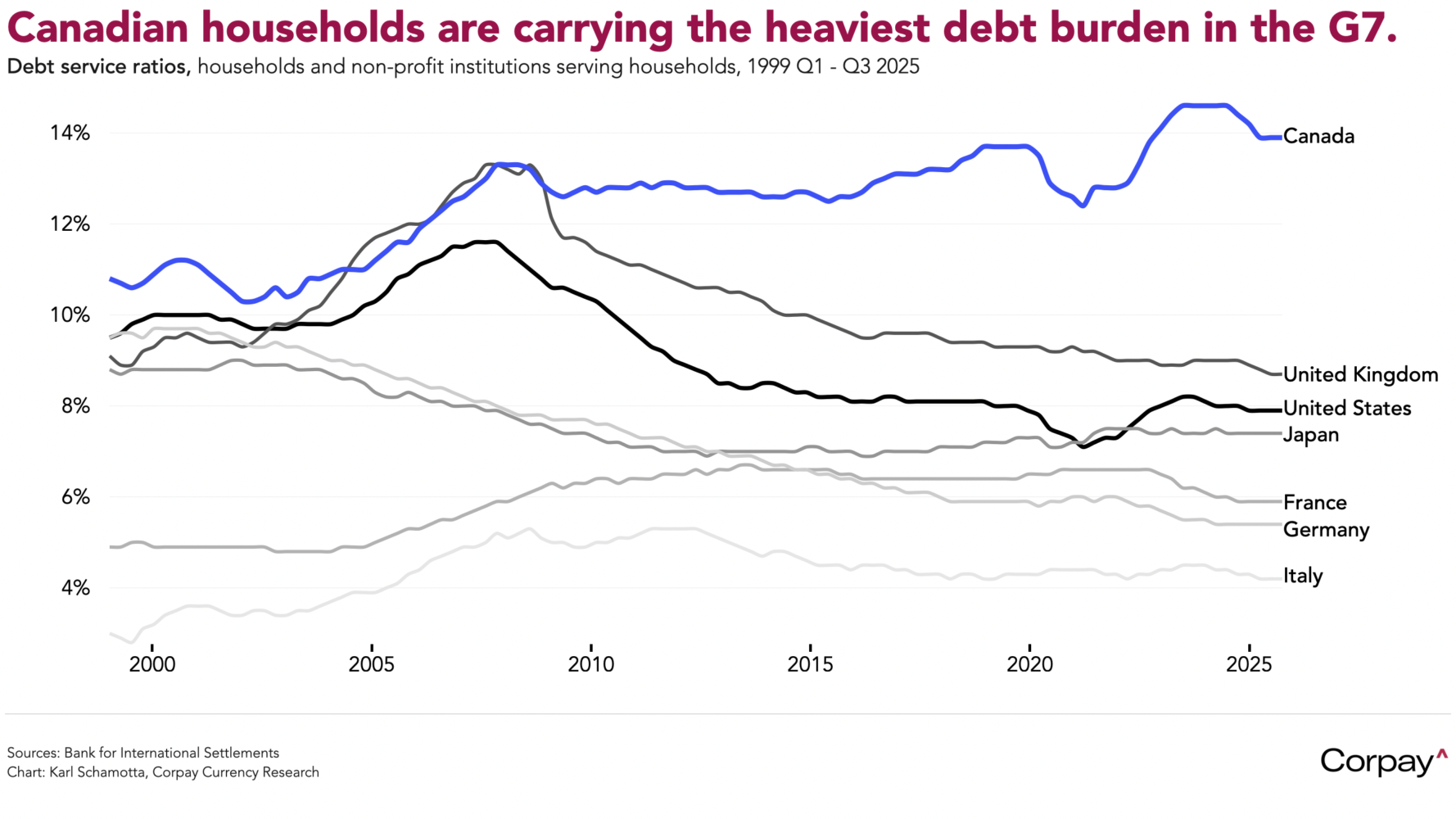

The Bank of Canada is expected to hold rates steady this morning and could maintain a cautiously-dovish tilt in its communications. Higher oil and gas prices will bolster energy sector revenues and lift downstream demand in the months ahead. Against that, elevated trade uncertainty, tepid business investment, and slack labour markets indicate the economy retains ample spare capacity, and higher input costs will squeeze household spending power at a time when consumers are anxious about employment prospects, unnerved by tariffs, contending with declining home values, and carrying the heaviest debt burden in the G7**. Language in the statement language and post-decision press conference could acknowledge upside inflation risks while hinting at a continued bias toward sitting on the sidelines, pushing the Canadian dollar slightly lower against the greenback.

In theory, this afternoon’s Federal Reserve decision should be thoroughly priced in. Data releases since the last meeting have shown price pressures running slightly too hot for comfort and the labour market cooling—but not cracking—reinforcing the case for staying on hold. The ‘dot plot’ is likely to show the median policymaker raising inflation forecasts, lowering growth expectations, and projecting one rate cut this year—closely matching what is now priced into financial markets.

To an unfortunate degree, reporter questions during the post-decision press conference are likely to focus on the central bank’s fight to defend its independence. A judge recently threw out the Trump administration’s subpoenas, ruling that its lawyers had produced essentially no evidence of criminal activity during the Fed’s renovation project, yet Jeanine Pirro, US attorney for the District of Columbia, has said she will appeal—giving Senator Thom Tillis grounds to delay confirmation of Kevin Warsh as the next chair.

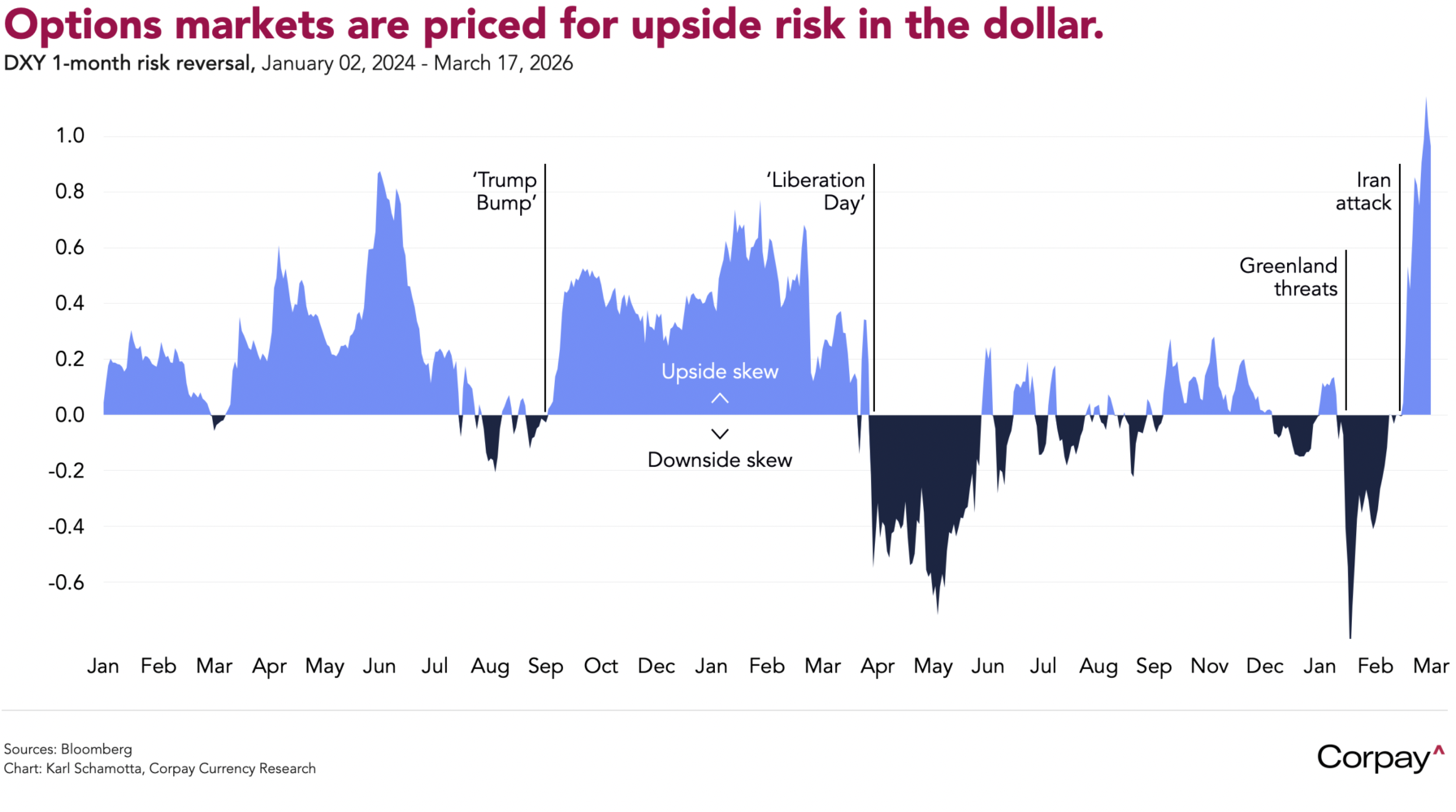

In practice, signs of a more hawkish bias could emerge, with Chair Powell explicitly flagging “two-sided risks” to the policy path as the economy absorbs the impact of the war in Iran. Should it become clear that the threat of an oil-driven inflation shock has led more officials to discuss raising rates, easing expectations could be pushed further along the curve, lending the dollar support—particularly if the European Central Bank, Bank of England, and Bank of Japan strike a more dovish tone in their own guidance. The greenback’s upside looks limited, but options markets are positioned for further gains, meaning that momentum could wrong-foot traders in the event of a hawkish surprise.

Taken in sum, exchange rates could get bouncy in the coming hours, justifying an attentive approach from currency hedgers. As we have repeatedly warned, recent moves should be viewed as a temporary deviation from trend, and trading opportunities may prove short-lived.

*He actually said “If we left right now, it would take ten years for them to rebuild. But we’re not ready to leave yet. But we will be leaving in the near-future; we’ll be leaving, pretty much, in the very near future”. Your mileage may vary.

**Note that the “debt service ratio”—the share of household disposable income devoted to servicing outstanding debt—used here is based on the Bank for International Settlements’ internationally-consistent methodology, not the Statistics Canada series more commonly deployed in Canadian economic analysis.