The dollar is on course for its strongest monthly performance since July and Brent crude is tracking what could be a record monthly gain as the US-Israeli war against Iran devolves into a protracted regional conflict. In an interview with the Financial Times last night, US president Donald Trump said “To be honest with you, my favourite thing is to take the oil in Iran but some stupid people back in the US say: ‘why are you doing that?’ But they’re stupid people”. “Maybe we take Kharg Island,” he said, “maybe we don’t. We have a lot of options,” alluding to the fact that thousands of ground troops have been ordered to deploy to the region.

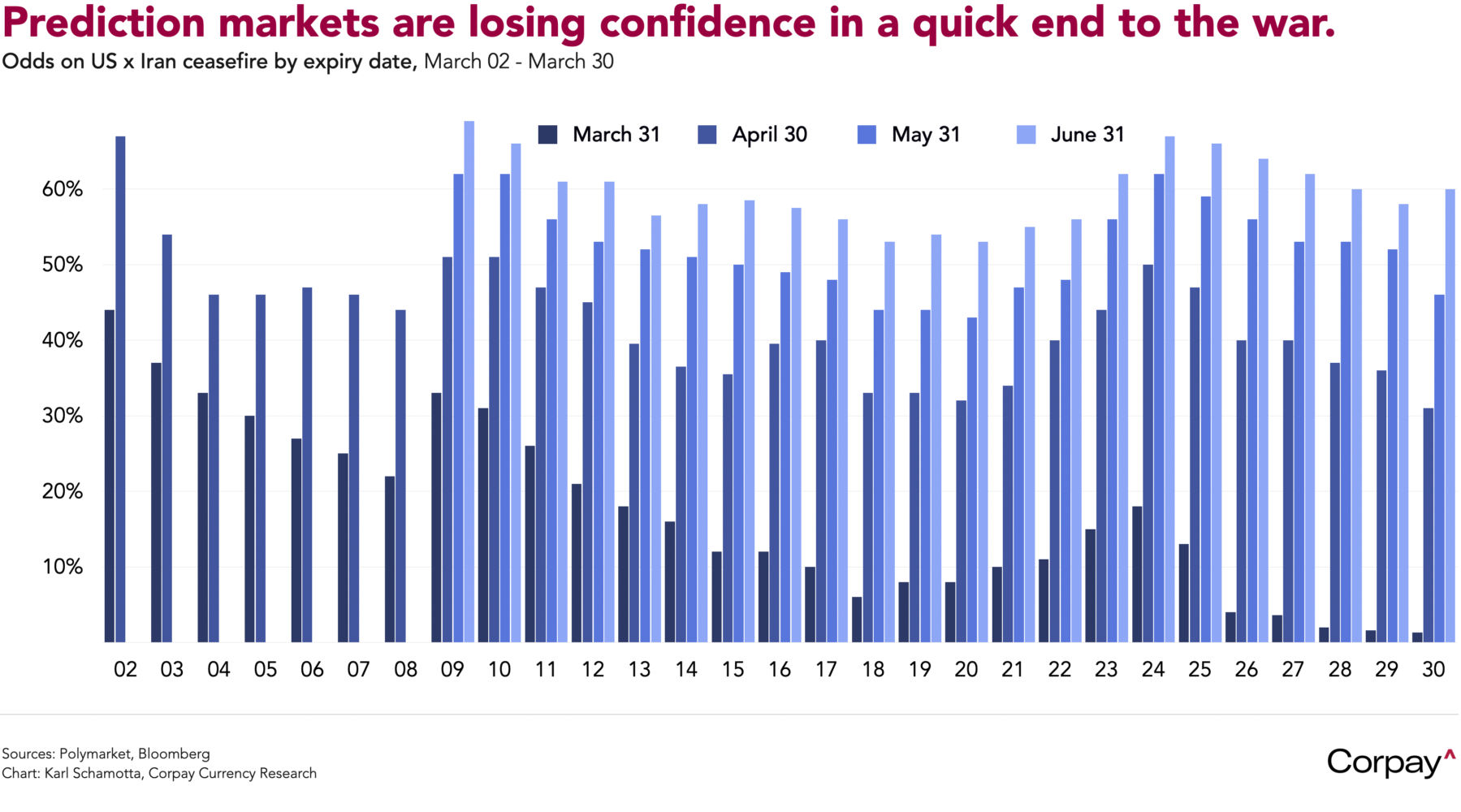

Prediction markets are abandoning bets on the US declaring a symbolic victory before the damage to the global economy becomes severe. Punters on Polymarket have sharply downgraded the likelihood of a ceasefire before the end of April and are placing greater than 70 percent odds on an American ground incursion by then.

The supply buffer in oil markets, already very thin, is narrowing by the day. Tehran has dismissed US negotiating terms as “unrealistic, unreasonable and excessive,” pressing on with missile and drone attacks across the region while maintaining effective control over the Strait of Hormuz—keeping it closed to Western-flagged vessels and those that have not paid transit fees to Iran. Yemen’s Houthi rebels have fired a ballistic missile at Israel, raising the prospect of fresh disruption to Red Sea transit routes and the Bab el-Mandeb strait, another key chokepoint through which roughly a tenth of global seaborne crude passes.

Currency traders have been much more hesitant to take directional positions, given the president’s habit of triggering sharp reversals with social media posts claiming the war is nearing its end. The dollar has benefitted from the rise in uncertainty, climbing on a persistent safe-haven bid since the beginning of March, while most of its rivals—including the Canadian dollar, pound, and euro—are trading below key support levels as participants hedge downside risks.

The Japanese yen is grinding lower even as the threat of official intervention grows more acute. After the currency slipped through the psychologically important 160 threshold against the dollar on Friday, Atsushi Mimura, vice finance minister for international affairs, noted that some market participants believed speculative moves in crude oil futures were spilling into foreign exchange markets, warning “the government will take all possible measures at any time” to shield households and the economy. In our view, the 160 mark doesn’t represent a ‘line in the sand’ for the Ministry of Finance—jumps in realised volatility tend to be better predictors of intervention efforts—but the trigger may have changed, given that Mimura also warned action could come “on all fronts,” dovetailing with reports that authorities are considering stepping into oil markets as well.

The cadence of economic data releases will pick up this week, offering investors a welcome distraction from war-related headlines. Statistical authorities in Europe and Japan will update inflation figures, and Canada will publish its February gross domestic product reading. In the US, surveys from the Conference Board and the Institute for Supply Management, along with the February retail sales and Job Openings and Labor Turnover releases, will culminate on Friday with the March non-farm payrolls report. Economists think roughly 50,000 jobs were added in the month as worker strikes came to an end and weather conditions improved, keeping the unemployment rate steady between 4.4 and 4.5 percent. A disappointing print could lower market-implied odds on a rate hike by year end, while a positive surprise would almost certainly lead to a doubling-down among market participants.

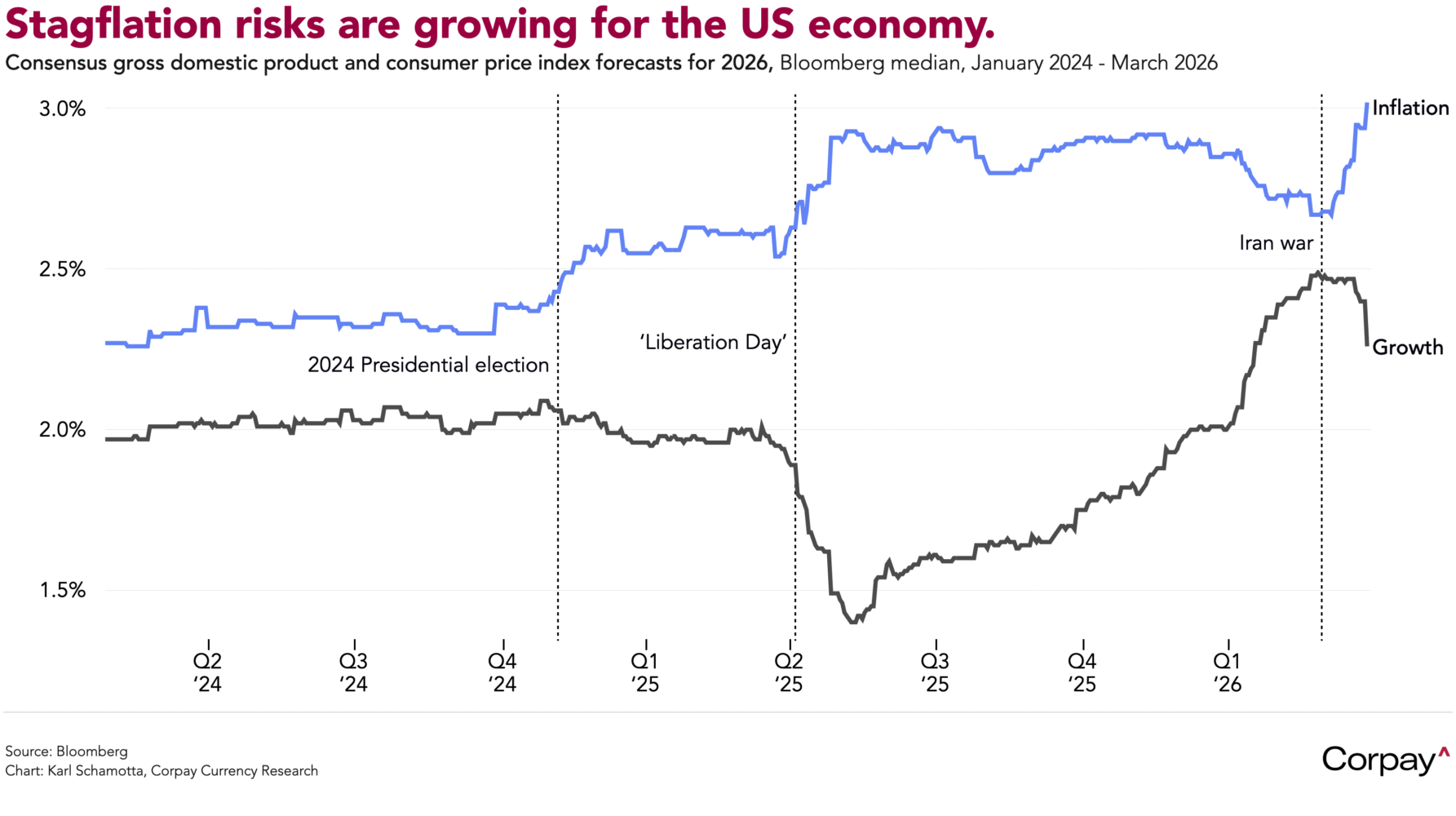

Markets could gain important insight today into how the Federal Reserve sees the balance of risks evolving. Chair Jerome Powell is scheduled to participate in a moderated discussion at Harvard this morning, followed this afternoon by a speech from New York Fed President John Williams, one of the institution’s leading intellectual voices. In the face of surging inflation pressures, several officials have suggested the next move could be an increase rather than a cut, and markets have responded by pricing in higher long-term rates, but the underlying economy is also showing clear signs of slowing momentum. We think the Fed will find itself in a stagflationary bind for a while yet—suggesting a prolonged hold may be more likely than either outcome—but Powell and Williams are well-positioned to bring more clarity to market expectations surrounding the Fed’s reaction function.

Please forgive me for talking our book*, but the case for considering tail risk protection has rarely been stronger. Policy uncertainty is running at multi-decade highs across geopolitical, trade, fiscal, and monetary dimensions simultaneously—a combination that fattens the tails of currency distributions and raises the probability of disorderly moves that fall well outside standard forecasting ranges. While the US political calculus is firmly tilted toward a face-saving compromise with Tehran and gradual reopening in the Strait of Hormuz, the truth is that no one knows how the situation will evolve over the next few weeks. Central bank reaction functions are themselves becoming less predictable as policymakers weigh conflicting inflation and growth signals, meaning the traditional anchor for currency valuations is loosening.

In this environment, structured options strategies make a lot of sense: they allow treasurers to lock in a worst-case rate while retaining participation in favourable moves, effectively converting an unquantifiable risk into a known cost. The asymmetry is compelling: the opportunity cost surrendered on the upside is modest relative to the balance-sheet damage an unfavourable three- or four-sigma move in the exchange rate could do.

It’s also important to move decisively. Waiting for volatility to spike even further before putting protection in place could make it very expensive—or unavailable at sensible strikes altogether.

As Nicolas Nassim Taleb likes to say, “If you must panic, panic early.”

*I really do try to keep such messages out of this note, but this is one of those junctures at which many organisations tend to fall into a “paralysis by analysis” trap, avoiding putting protection in place as they try to game out future outcomes. Quite frankly, no one can predict what might happen next, so it’s only prudent to take out some insurance against extreme moves.