A wave of cautious optimism is washing over financial markets after the United States reportedly offered Iran a 15-point peace plan, reinforcing the belief that Washington is looking for an exit from the conflict. Details of the proposal are unclear, but investors are turning more hopeful* even as the Strait of Hormuz remains effectively closed, attacks continue on both sides, and more American troops are deployed to the theatre, Treasury yields are edging lower, equity futures are setting up for a gain at the open, and the dollar is retreating against a basket of its major rivals.

The pound is little changed after inflation held steady at an 11-month low last month. Consumer prices rose 3 percent in the year to February, matching the prior month’s pace, while the closely watched services measure edged down to 4.3 from 4.4 percent, according to the Office for National Statistics. The data is considered stale, however, having been collected before the war triggered a spike in energy costs and a jump in expectations for the Bank of England’s rate path.

Prices are mean-reverting across asset classes. In the energy complex, Brent for May delivery is trading for less than $100 per barrel, West Texas Intermediate is going for $87, and European natural gas futures are down almost 10 percent as investors bet on a shallower and less prolonged supply disruption. Trading activity is slowing in bond markets, and implied volatility is falling in currencies as tail-risk hedges are unwound. Inflation breakevens and policy expectations are starting to come down across the advanced economies, reflecting a growing sense that the moves of the past two weeks were overdone.

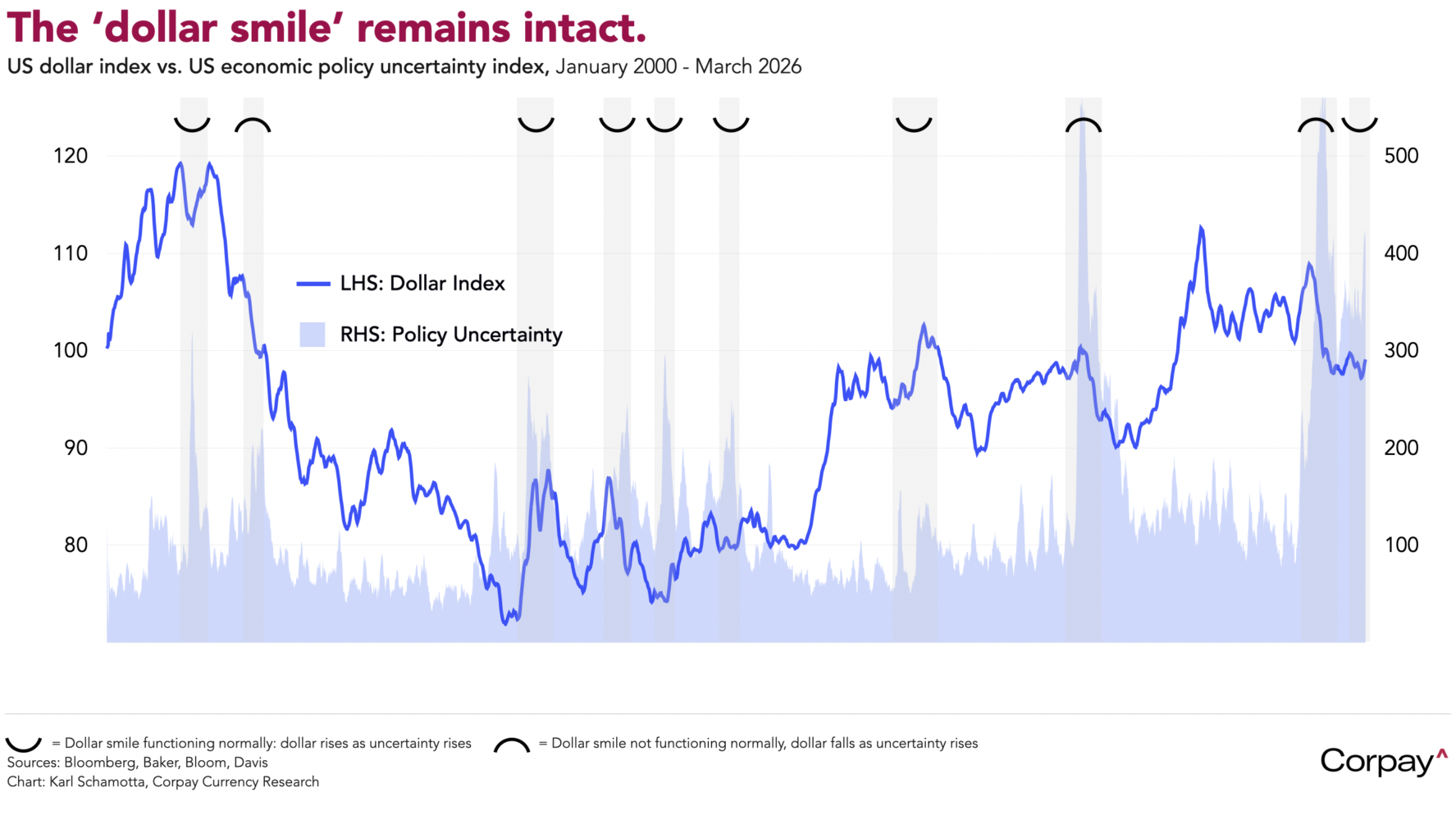

Although short-term reversals are likely, we think this process has farther to go. The unknowns remain formidable: who Washington is negotiating with, whether Tehran is interested in a deal, and what the parties actually hope to achieve. Markets will undoubtedly experience more turbulence. But the Trump administration has a well-established record of backing down when markets tumble, bond yields rise, and approval ratings plunge—as they have in recent weeks. Inflation fears also look overwrought: energy costs account for a far smaller share of consumer spending than in decades past, and the excess demand conditions that characterised the post-pandemic economy are now behind us**. If the conflict settles to a dull roar and labour market data continue to soften, it would not be surprising to see rate cuts back on the table in some economies—the United States foremost among them—and exchange rates reverting to pre-war levels. Once safe-haven flows diminish, the dollar should slide toward the bottom of its ‘smile’ once again.

*Samuel Johnson supposedly called second marriage “a triumph of hope over experience,” and something similar might apply to news of a breakthrough in this administration’s geopolitical maneuverings.

**There may be an element of ‘recency bias’ at work here, with investors—and policymakers—prone to overreaction after the post-pandemic inflation shock. It is important to recognise, however, that there are major differences in underlying demand and supply conditions that make it difficult to compare the two episodes.