An uneasy sense of calm is settling on currency markets this morning as signs emerge that the conflict in the Middle East may be approaching a negotiated end. According to the New York Times, Iranian intelligence officials have made indirect contact with their US counterparts to “discuss terms for ending the conflict,” dovetailing with a shift in tone from president Trump, who said in a Sunday interview “What we did in Venezuela, I think, is the perfect scenario,” —suggesting that he is willing to step back from earlier demands for regime change in Tehran.

Selling pressure eased in yesterday’s session after the president offered to insure vessels transiting the Strait of Hormuz and said the US Navy could escort critical energy shipments through the waterway. Shipowners and commodity trading firms expect such measures could take weeks to deploy—but markets have drawn comfort from the implicit assurance that logistical disruptions might be measured in weeks rather than months.

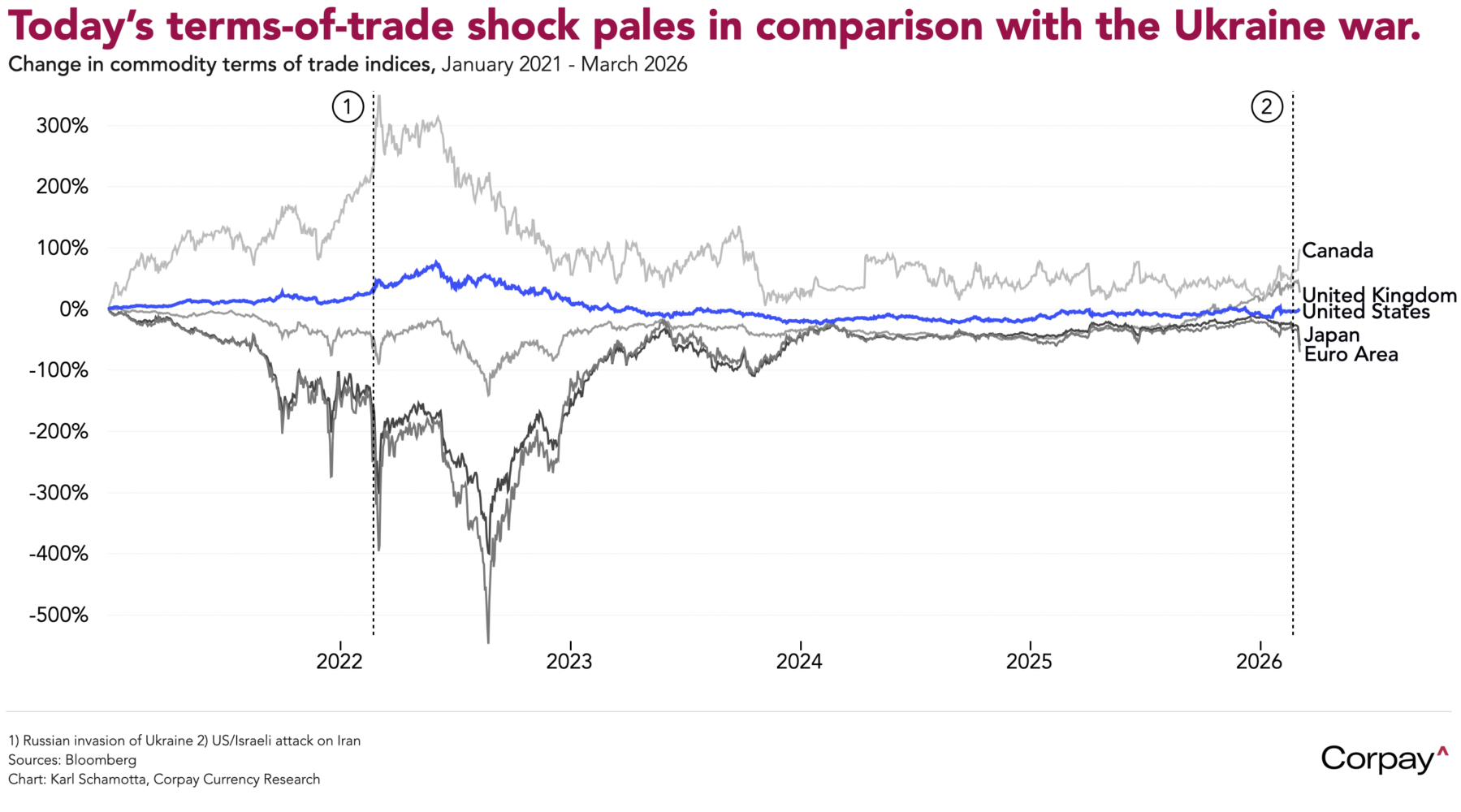

Oil and gas prices are still in rarefied territory, with Brent and West Texas Intermediate for prompt delivery trading roughly 15 percent above Friday’s close and European natural gas benchmarks up nearly 35 percent—yet futures curves suggest markets expect the spike to prove temporary. Elsewhere, the picture is one of tentative stabilisation: Treasury yields are holding steady, US equity futures are pointing to modest gains at the open, and the dollar’s advance is losing momentum as traders unwind short positions in currencies most exposed to an energy-price shock. By the standard of the commodity terms-of-trade disruption that followed Russia’s invasion of Ukraine in 2022, today’s move remains relatively modest.

The psychological impact could soon look overdone. US gasoline prices may have jumped at the fastest pace since 2005 over the last two business days, but the share of consumer spending going to energy costs remains extremely low, and there’s very little evidence to suggest that a sustained unanchoring in inflation expectations is underway.

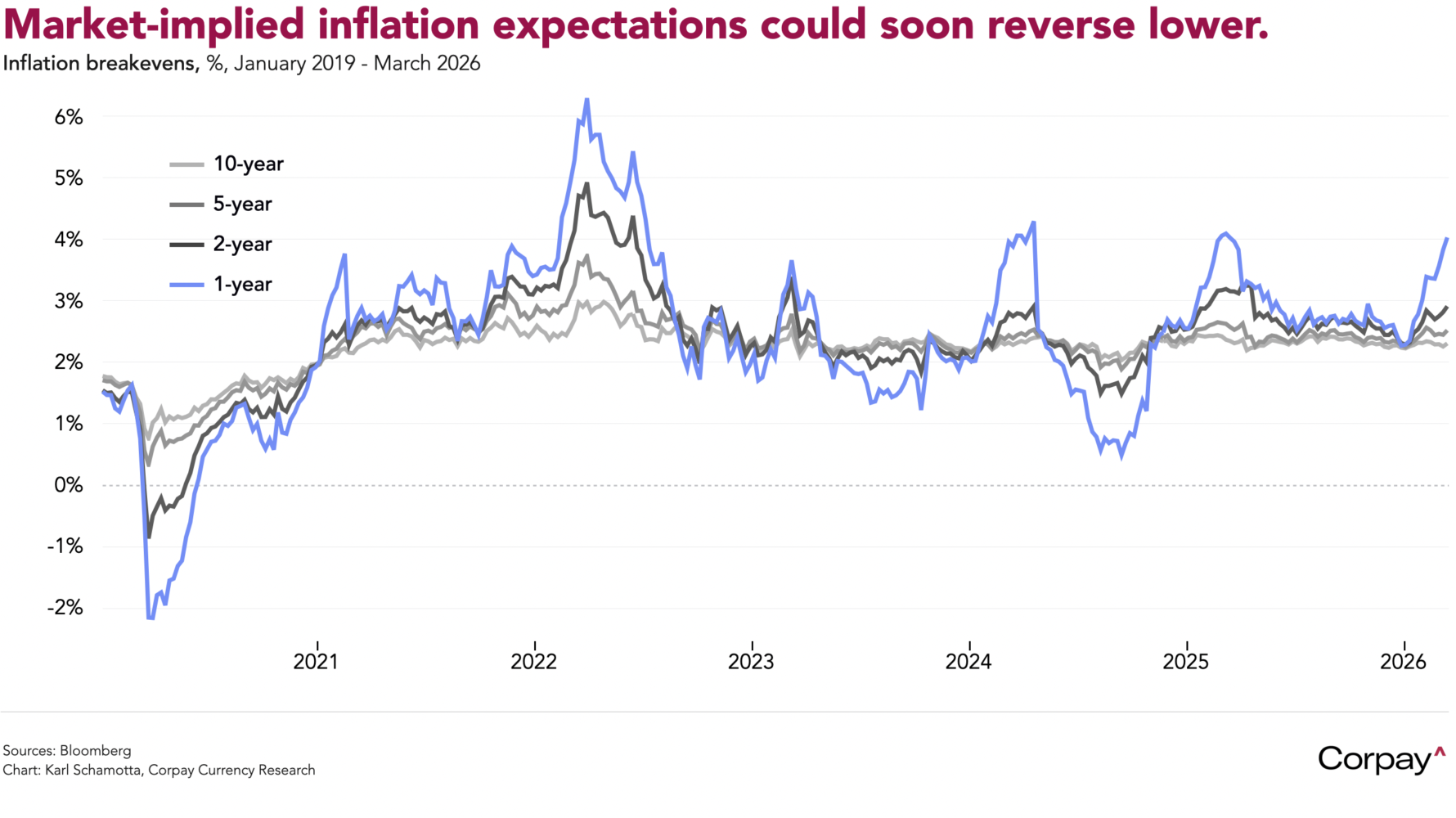

Markets may have been premature in pricing out Federal Reserve rate cuts so aggressively. Breakevens—the spread between nominal Treasury yields and their inflation-protected equivalents—have risen sharply from their early-year lows, but could retreat as investors come to see the price impact as short-lived and contained. If so, the case for renewed easing would reassert itself

Bottom line: tail risks remain substantial, and measures of implied volatility are likely to remain elevated for a prolonged period, but there are good reasons to think that a “mean reversion” process could soon get underway in currency markets, returning a number of pairs to levels that prevailed ahead of the weekend attack. Moves like this are—of course—impossible to time with any precision, but hedgers should consider laying off some exposure if current levels are more attractive than last week’s.