Good morning. Risk appetite is deteriorating across the financial system as the Middle East conflict shows little sign of easing ahead of President Trump’s deadline for resuming military strikes against Iranian power plants and energy infrastructure tomorrow. Although there are clear signs of political exhaustion in Washington, Iran yesterday rejected the administration’s maximalist overtures, and Axios is reporting that the Pentagon is preparing options for a major escalation, possibly including the deployment of ground forces. Brent crude is back above $107 a barrel, West Texas Intermediate is climbing through $94, and European natural gas futures are pushing higher as prospects for an immediate reopening of the Strait of Hormuz dim.

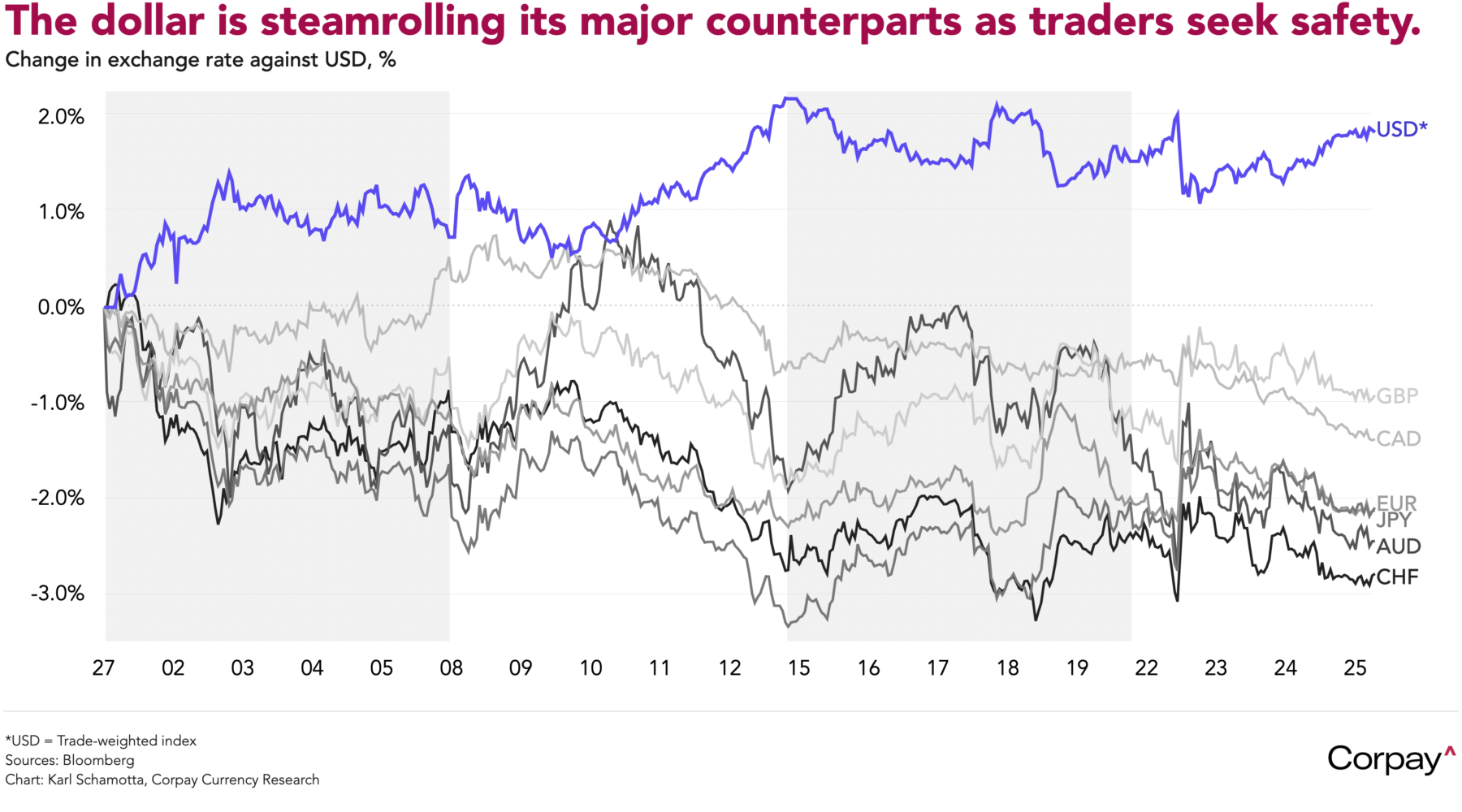

Currency markets are seeing frenetic trading action within relatively-tight ranges. On a trade-weighted basis, the dollar looks set to end the month roughly 2 percent higher (a modest gain by the standards of previous conflicts) as demand for liquidity overwhelms the structural case for weakness. Net energy importers in Europe and Asia are firmly on the defensive as traders downgrade growth expectations in the face of a severe terms-of-trade shock. Intervention threats from the Swiss National Bank are offsetting the franc’s safe-haven appeal, pushing it lower against all of its major counterparts. And the Canadian dollar is outperforming its rivals while trading with a weakening bias against the greenback as wide rate differentials—driven largely by domestic economic frailty—nullify a brighter export outlook.

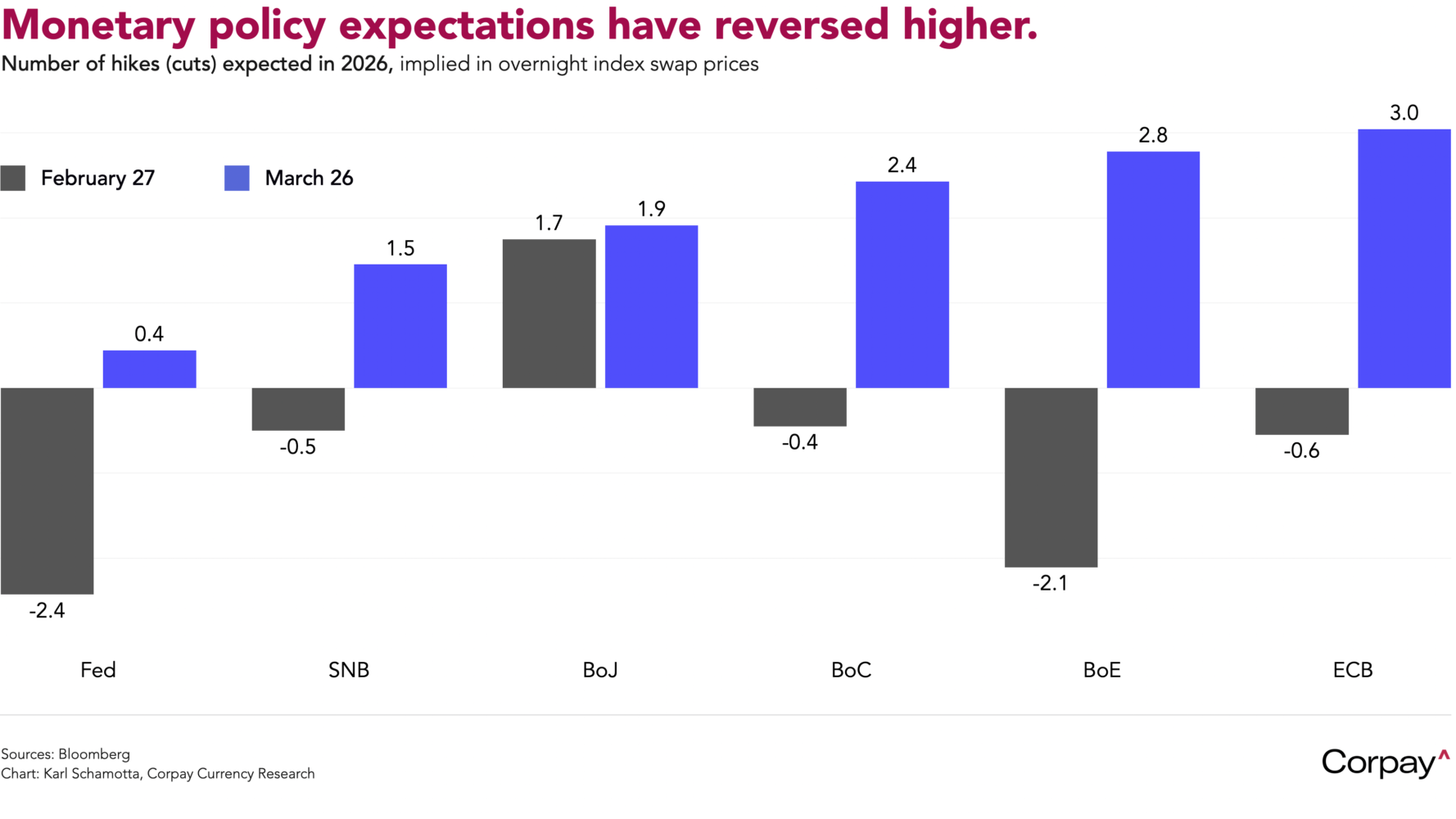

Monetary policy expectations and front-end government bond yields remain elevated, with investors bracing for a near-term inflationary overshoot while paying less heed to the possibility of a longer-term growth downturn. After beginning the year in neutral, markets are putting nearly 20-percent odds on a rate hike from the Federal Reserve by year end, and expect at least one move from the Swiss National Bank, two from the Bank of Canada, and three each from the Bank of England and European Central Bank. In my view, this looks overdone: after a long history of overtightening into growth slowdowns, policymakers in most major economies are more likely to leave rates on hold than to raise them for now. The risk of policy mistakes grows, however, for every day that energy flows out of the Middle East remain blocked.

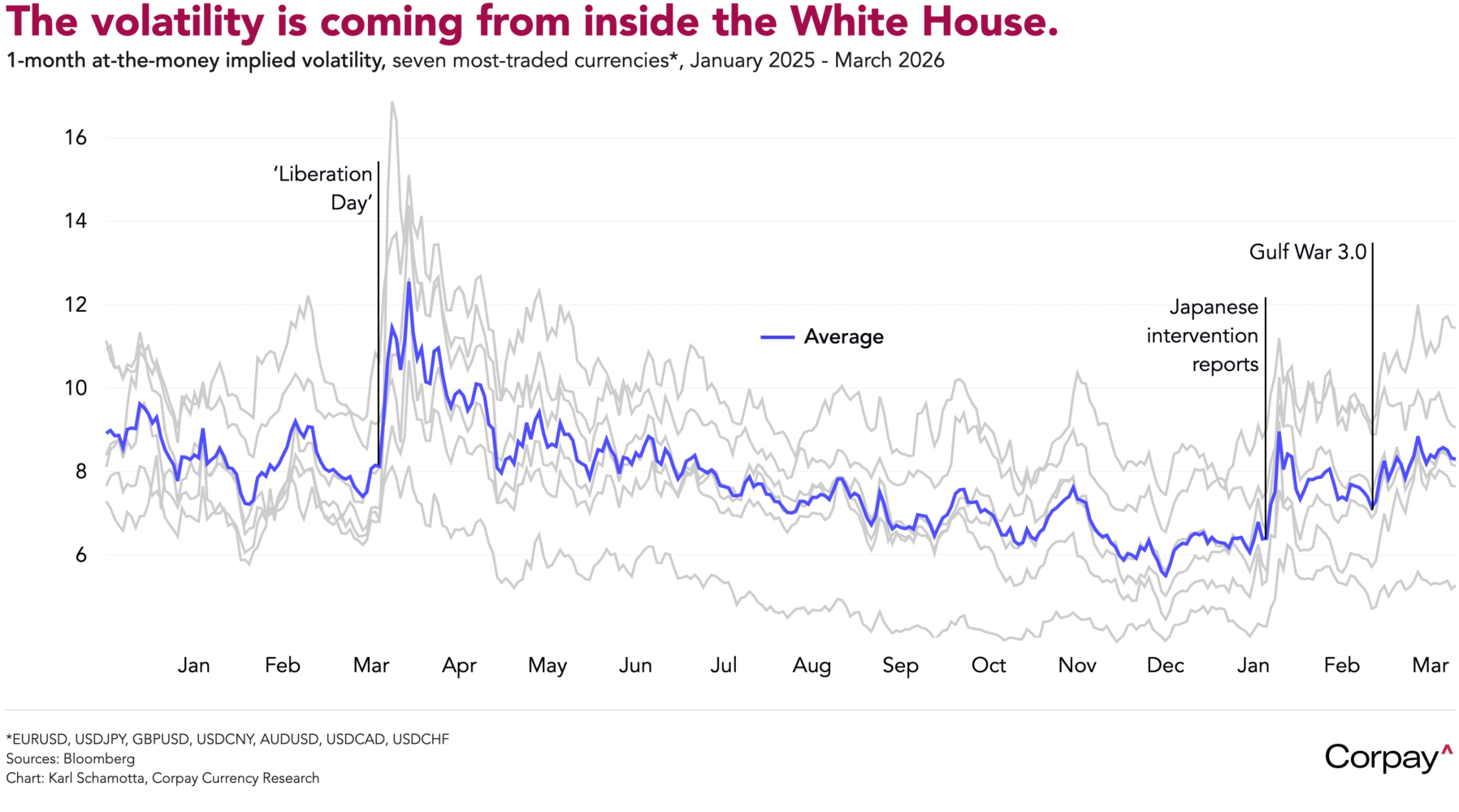

Another bout of turbulence could hit tomorrow evening, when President Trump is scheduled to speak at the Future Investment Initiative Priority Summit in Miami at 5:30 pm, giving him an opportunity to outline next steps in the war with Iran. At this juncture, it is impossible to know what he will say, but it is worth noting that every major volatility shock in currency markets over the past 15 months has originated from a member of the Trump administration, and most have been timed to land when North American markets are closed.