• Holding up. Markets held onto yesterday’s gains stemming from the US/Iran ceasefire news. However there wasn’t much additional follow through in FX.

• AUD & NZD. AUD near top of its ~2-week range. But lingering issues are a headwind. RBNZ’s ‘hawkish’ vibes may help NZD recoup more lost ground.

Global Trends

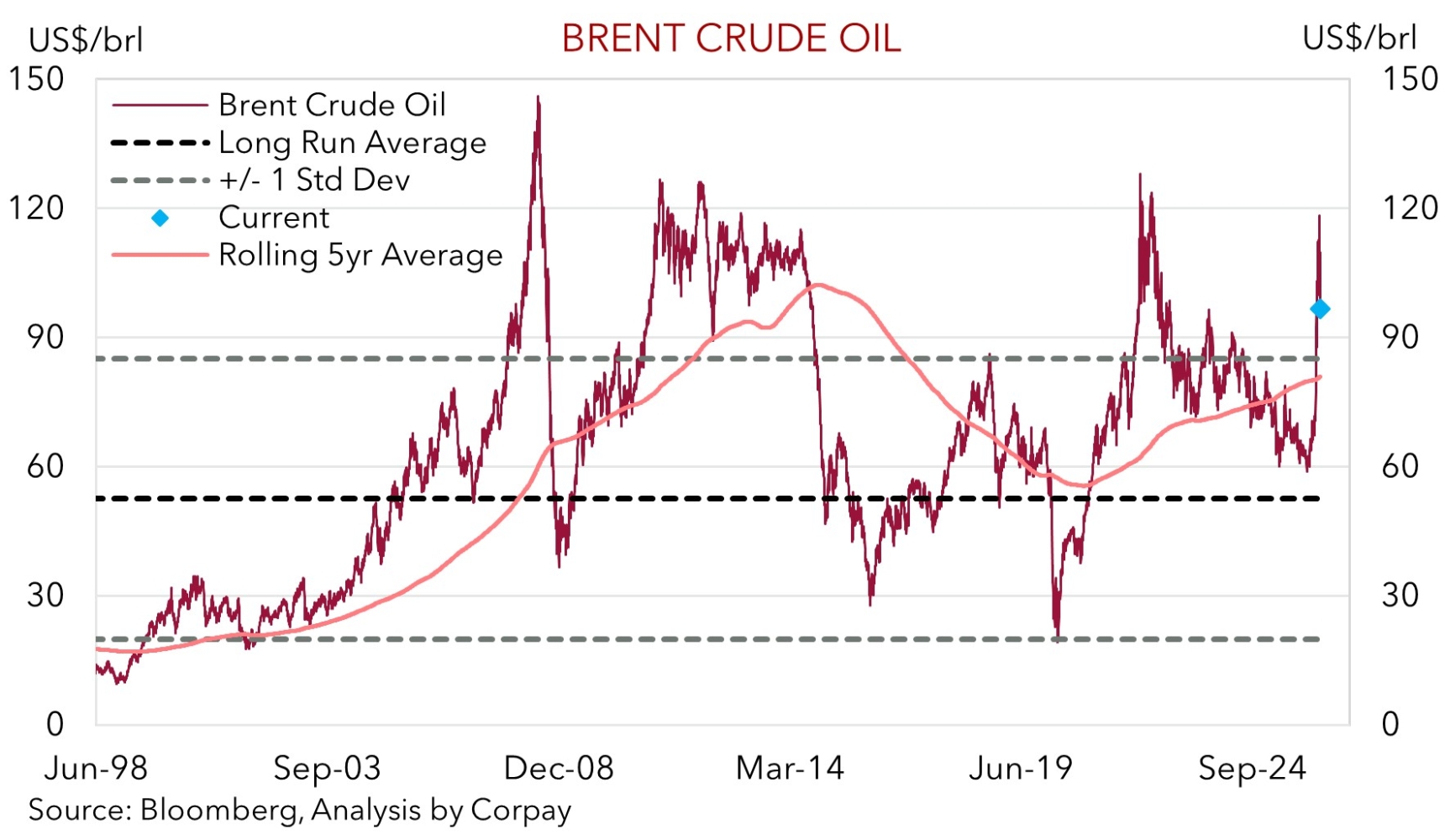

Risk sentiment has remained positive over the past 24hrs on the back of yesterday’s US/Iran ceasefire news. However, in a reflection of how fragile the situation still is most asset classes remained range-bound overnight after yesterday’s knee-jerk repricing as the initial headlines came out. That said, there have still been some meaningful moves such as the: drop in oil (Brent crude is now ~$96.70/brl, ~13% from this week’s peak); ~14% fall in European natural gas prices; decline in bond yields as central bank rate hike expectations were pared back (European 2yr bond yields tumbled ~22-25bps); jump in equities (the US S&P500 rose 2.5% while the EuroStoxx600 and Japan’s Nikkei increased by ~3.9% and ~5.4% respectively); and weaker USD.

Reduced safe-haven demand and the lower oil price (given the US’ status as a ‘net energy exporter’) has exerted downward pressure on the USD. EUR (now ~$1.1666) is at the upper end of its ~1-month range, as is GBP (now ~$1.3401), and USD/JPY lost some ground (now ~158.57). Cyclical currencies like the AUD (now ~$0.7046) strengthened, although as mentioned, this move largely occurred just after ceasefire headlines hit the wires. NZD (now ~$0.5823) was also underpinned by ‘hawkish’ vibes at yesterday’s RBNZ meeting.

As mentioned yesterday, the situation in the Middle East has relatively improved, but things remain fluid and given the volatile participants involved it could deteriorate at any time. Indeed, the fragility of the ceasefire is already being tested with reports Iran closed the Strait of Hormuz in response to attacks on Lebanon by Israel. There are also several questions about the ceasefire agreement given the 10-point plan President Trump received from Iran seems at odds with the 15-point plan put forward by the US. The first round of peace talks are set to take place on Saturday in Islamabad. Moreover, important underlying issues for the global economy remain such as when/if the flow of energy/vessels via the Strait of Hormuz gets back to where it was before the conflict, and how much disruption there has been to supply-chains. We think these issues may take months/quarters to clear up, not days/weeks, and that the economic fallout from the conflict is closer to the beginning than the end. Over the next few months global growth seems set to be weaker and inflation higher than where it was predicted to be before the conflict kicked off. More bursts of market volatility should be anticipated, in our opinion, and in turn the USD may not fall away that much more in the short-term.

Trans-Tasman Zone

Sentiment has remained positive since yesterday’s US/Iran ceasefire news, however as mentioned above, there was limited follow through in FX markets overnight after the initial knee-jerk adjustments. In our mind this reflects the ongoing uncertainty about the economic impacts of the conflict and the fragile nature of the ceasefire. At ~$0.7046 the AUD is hovering just below yesterday’s intra-day peak, which is ~1 cent above its year-to-date average. It has been a similar story on most of the AUD cross-rates with AUD/EUR (now ~0.6040), AUD/JPY (now ~111.72), AUD/GBP (now ~0.5258) and AUD/CNH (now ~4.8148) drifting back a little from their respective highs.

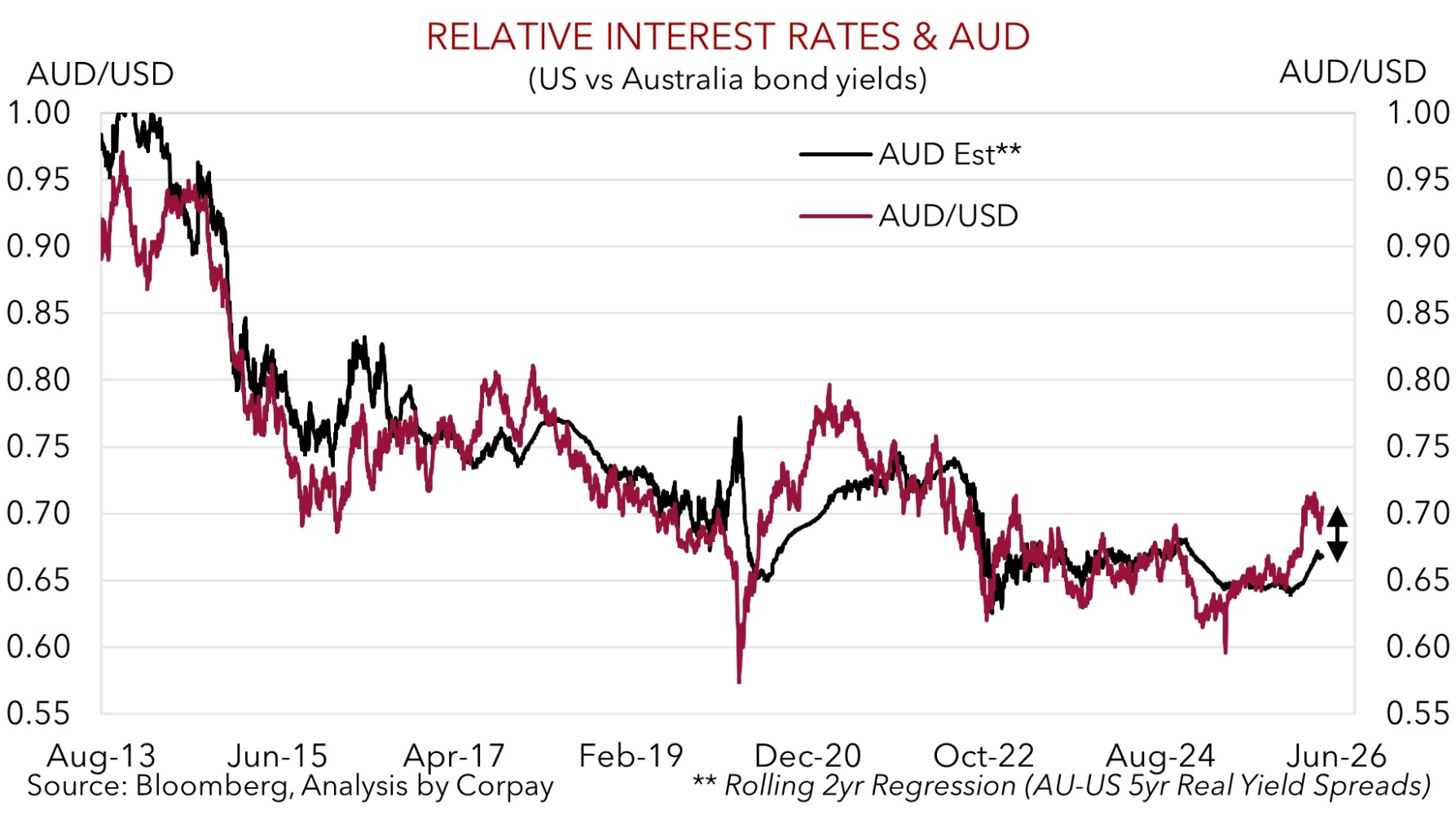

In terms of the AUD, the US/Iran ceasefire is a short-run positive as it lessens a few of the downside risks facing the global economy. But these risks haven’t been extinguished. As flagged, the impact on supply-chains and energy supply could take some time to rectify. This in turn can continue to act as a handbrake on global activity, particularly across Asia which is where ~85-90% of the energy shipped via the Strait of Hormuz is sent. We think given how much more RBA tightening is already factored in (markets are pricing in another ~56bps of RBA hikes by year-end), the lingering global growth headwinds, and with negative domestic consequences of higher mortgage rates and fuel costs in the pipeline, further upside in the AUD could be capped.

Across the Tasman, as expected, the RBNZ kept interest rates on hold at 2.25%. However, the rhetoric about the policy outlook was a bit more ‘hawkish’. The RBNZ was honest in its assessment that in the “near-term” inflation is “expected to increase” and the “economic recovery to weaken” as the conflict in the Middle East disrupts supply chains and energy prices. However, the RBNZ’s tolerance isn’t limitless as signs there are 2nd round price pressures building could mean that “decisive and timely” interest rate hikes may be needed. Markets are pricing in a full RBNZ rate rise by September, with ~92bps of tightening now discounted by March 2027. In our view, the reduction in downside global growth risks (assuming the US/Iran ceasefire holds) and lower energy prices can help the NZD recovery more lost ground over the period ahead. The NZD has been weighed down because of NZ’s status as a ‘net energy importer’. Indeed, the NZD looks to have beaten up too much given it is tracking well below our ‘fair value’ estimate (our models indicate the NZD should be up closer to ~$0.60 and AUD/NZD should be down around ~1.17).