Good morning. Currency markets are still struggling to navigate conflicting signals from the Middle East. Iran’s deputy foreign minister reportedly told Sky News Arabia that Tehran might be willing to surrender its enriched uranium stockpile in “return for something good”, but an empty tanker was struck off the coast of Kuwait overnight, pointing to a widening campaign against Gulf shipping. Against that backdrop, ten-year Treasury yields are rising for a fourth consecutive day, equity futures are little changed, and the dollar is edging higher. The euro, sterling and yen are all on the defensive, yet holding above key technical levels for now, and the Canadian dollar—caught between a stronger greenback and firmer oil prices—is treading water.

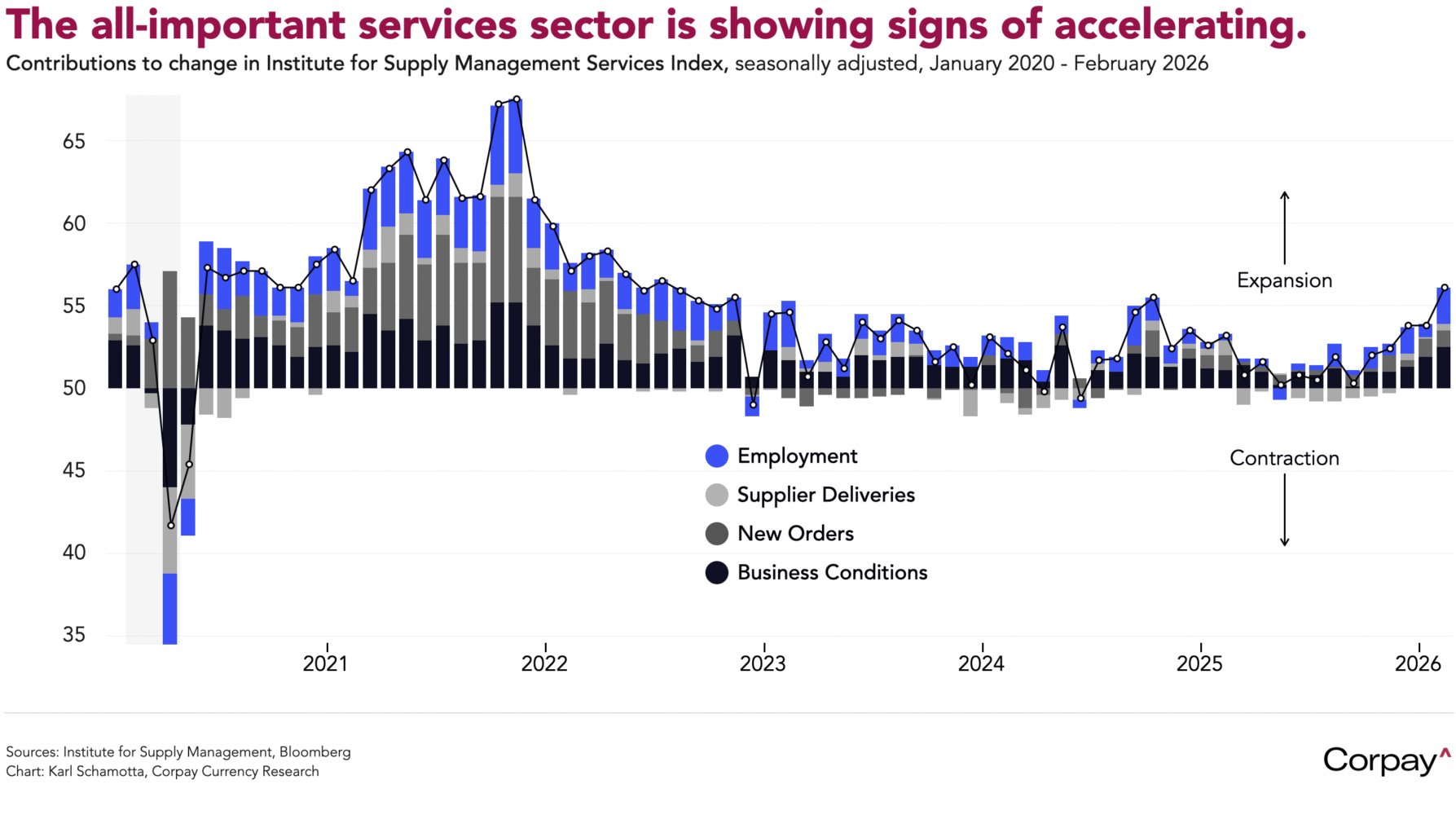

Incoming data continues to support an optimistic view on US growth and a hawkish stance on monetary policy. The Federal Reserve’s Beige Book, released yesterday, pointed to a firming in economic activity even as businesses flagged an uncertain policy environment, and the Institute for Supply Management’s services index for February came in well ahead of expectations, rising to 56.1 from 53—topping all forecasts on broad-based gains in current activity, new orders and employment. The services sector drives roughly two-thirds of US economic activity, and creates the bulk of new jobs, implying that it should be overweighted in forecasting frameworks relative to still-soft manufacturing industries.

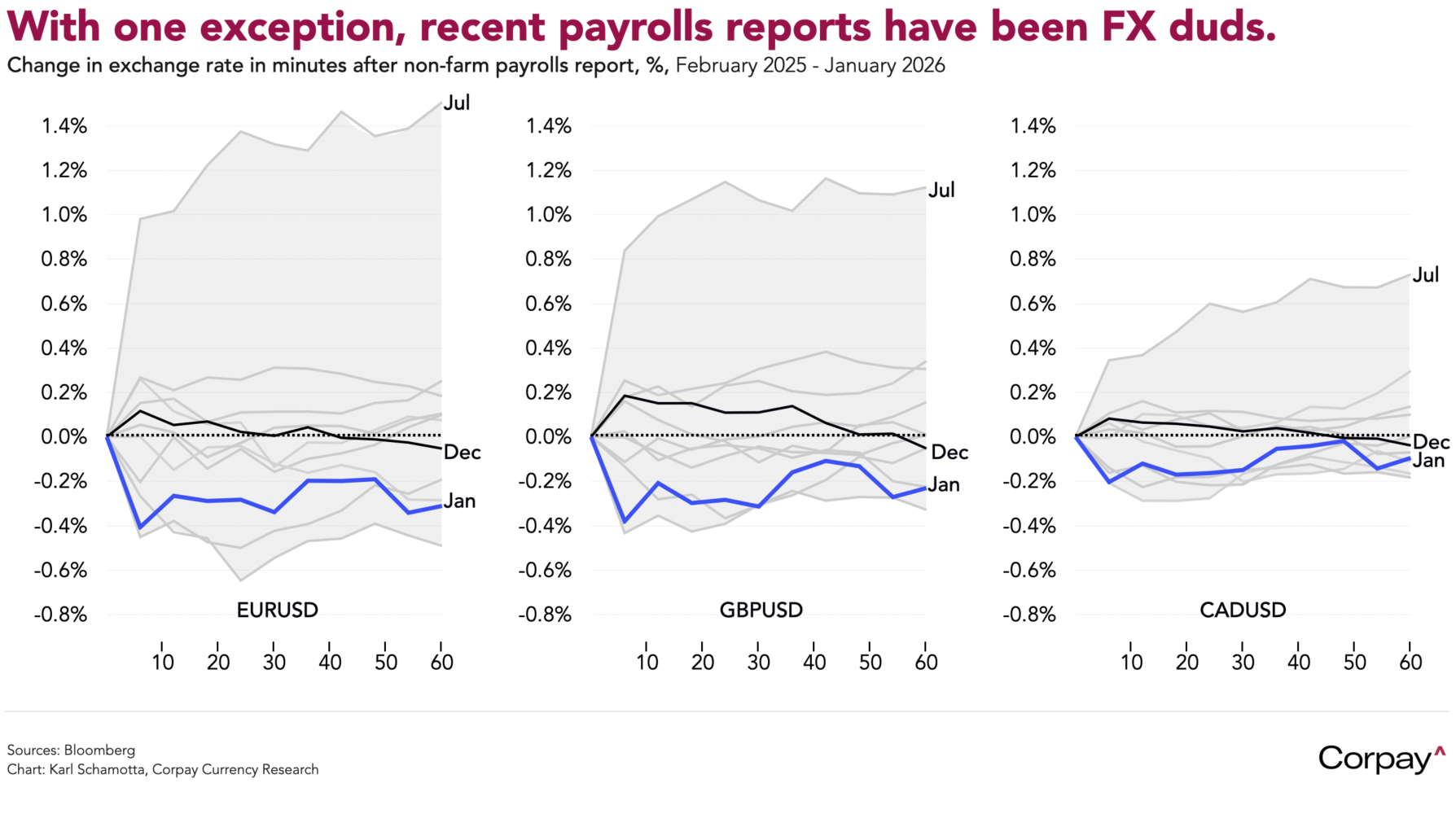

Expectations are drifting higher ahead of tomorrow’s non-farm payrolls report, with investors marking up their forecasts and discounting downside risks. On paper, the consensus thinks roughly 55,000 positions were added against an unchanged unemployment rate, but the “whisper number” circulating on trading floors is likely inching higher, particularly after this morning’s better-than-anticipated jobless claims number. A strong print would reinforce the hawkish repricing already under way and extend the dollar’s recent advance. We are marginally more cautious than most—the survey week coincided with an unusually cold spell, which may have weighed on hiring—but we have to admit that payrolls releases over the past year (July print aside) have largely met expectations, and have failed to move currency markets, with most major pairs settling only modestly off pre-release levels.

The risk of a parabolic rise in energy prices remains. US and Israeli forces have made progress in reducing Iran’s capacity to launch ballistic missiles, but Tehran still commands thousands of drones, sea mines and proxy forces capable of wreaking havoc across the region. A prolonged closure of the Strait of Hormuz, or a sustained campaign against energy infrastructure, could yet drive crude and natural gas prices well beyond thresholds that have historically acted as a brake on global growth. The foreign exchange implications are asymmetric: the yen, the euro and sterling stand out as the major currencies most exposed to another wave of selling. The Canadian dollar and the Norwegian krone, by contrast, would find support—both economies are leveraged to higher oil prices through export revenues, and both currencies tend to correlate more closely with crude benchmarks as prices rise. The dollar’s response would be more nuanced: although safe-haven demand would provide a natural floor, sharply higher energy costs would cloud the growth outlook, complicate the Federal Reserve’s path and risk inflaming domestic political tensions—factors that would cap any sustained advance.

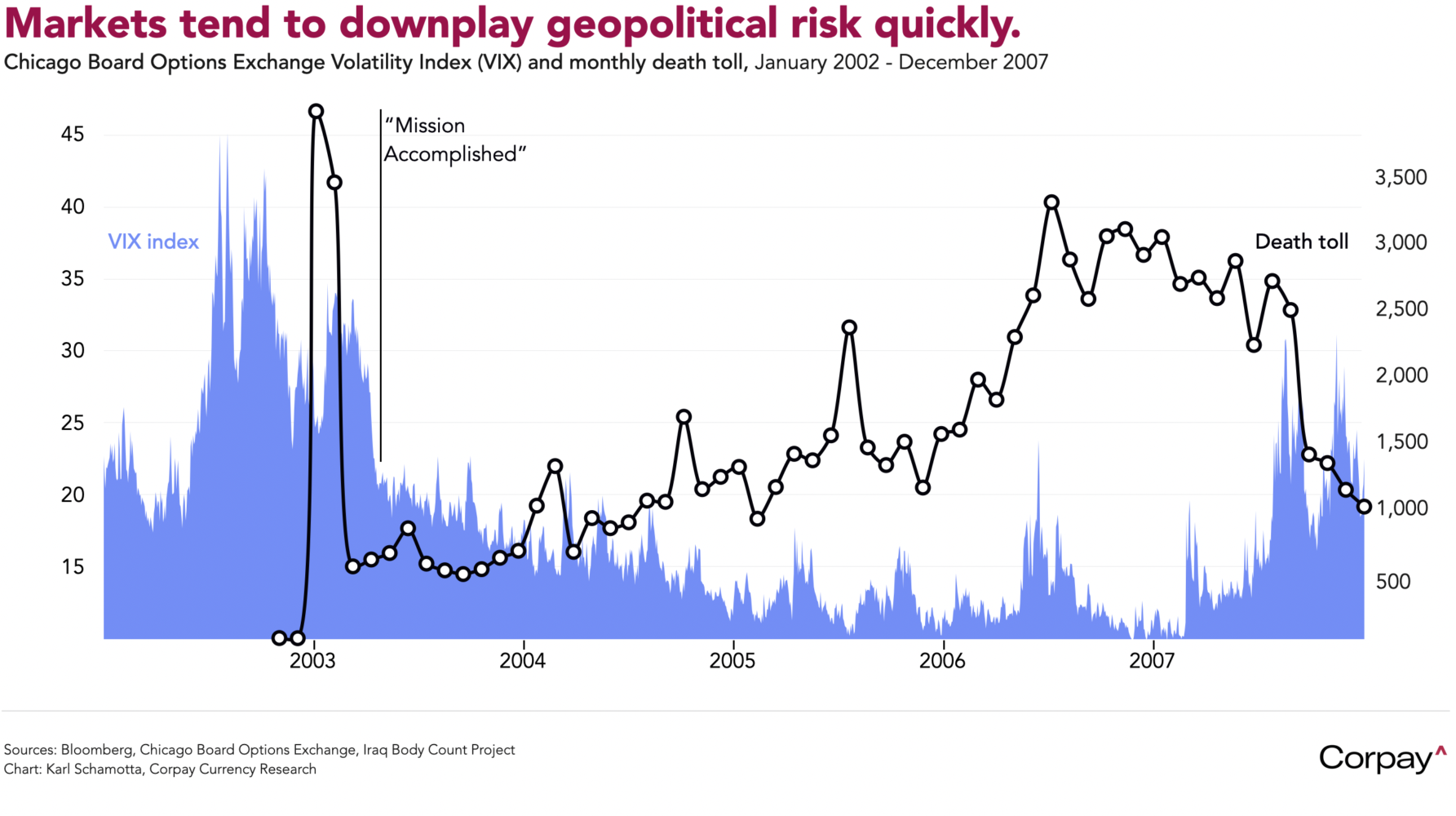

But markets appear to be discounting that risk. Momentum in spot rates has fallen sharply in recent days, and term structures across commodities, rates and volatility products are all pointing to a disruption measured in weeks rather than months. This follows a well-established playbook: in the 2003 invasion of Iraq, for example, the VIX surged in the run-up to American troops crossing the border, then collapsed as President Bush declared victory from the deck of the USS Abraham Lincoln, continuing to drift lower through the years that followed, even as the body count rose—the bulk of the casualties came after investors lost interest.

Bottom line: With the tail risk of an energy shock that falls hardest on the yen, euro and sterling looming large—and US data surprising to the upside—the case for a move out of the dollar looks less than compelling. Hedgers should remain wary nonetheless, given that markets have a well-established habit of pricing swift resolutions to geopolitical crises—a “melt up” in risk-sensitive currencies remains a strong possibility.