• Geopolitical nerves. US/Israel conflict with Iran has dampened risk sentiment in early Asian trade. USD firmer. NZD slips back. AUD underperforms.

• Lingering risks. Market nervousness may persist for a while. Focus on oil. Risk of a jump up in prices. This could have macro impacts & be USD supportive.

Global Trends

The weekend geopolitical news looks set to dominate the market action, at least through the early part of the week. There is heightened uncertainty following the US/Israel missile attack on Iran, the confirmed death of Iran’s Supreme Leader Ayatollah Ali Khamenei, and Iran’s retaliatory strikes at neighbouring nations. Based on the movement of military assets into the region over the past few weeks an escalation appeared inevitable, yet complacent markets seem to have been caught off guard given the below average level of implied volatility across most asset classes, tight credit spreads, and undervalued oil price.

A (modest) bout of risk aversion has washed through the markets that have reopened. It is reported that oil prices jumped ~10% in over the counter trading over the weekend. Elsewhere, Middle East equity indices declined yesterday, while in FX the USD index perked up this morning and other traditional safe-haven currencies like the JPY held their ground. EUR has dipped (now ~$1.1768), as has GBP (now ~$1.3414), and growth/cyclical currencies such as the NZD (now ~$0.5950) and the AUD (now ~$0.7040) have underperformed. We think the nervousness might cascade through more markets as they reopen for the week. Signals from the various parties suggest there is a chance of a protracted conflict. US President Trump is calling for regime change, not something that can be easily achieved, and there are lingering worries about regional supply routes, especially given ~20% of oil (and a similar proportion of LNG) passes via the Strait of Hormuz.

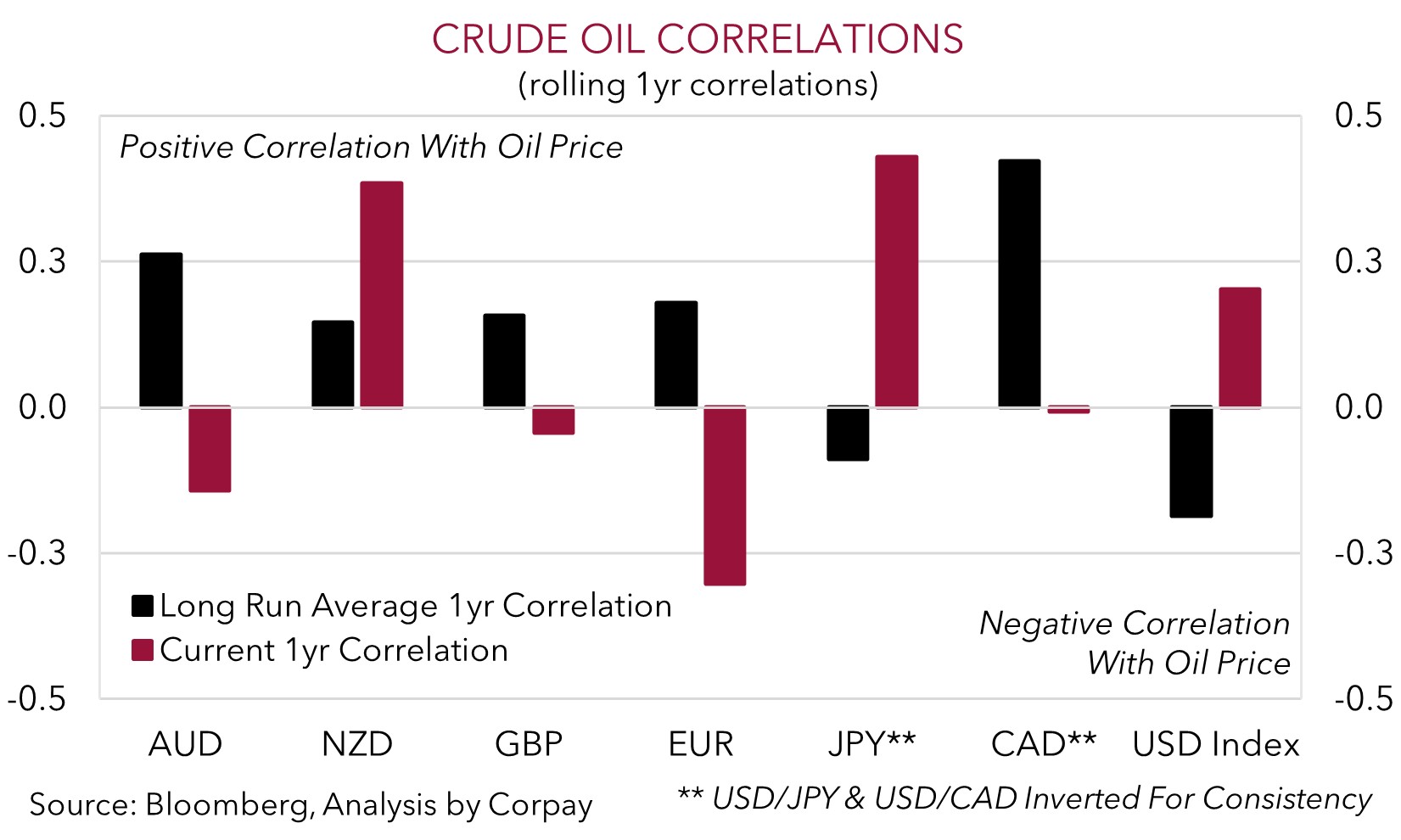

Iran’s Foreign Minister has indicated there is no intention to close the Strait of Hormuz, however trade flows will still be disrupted. In our opinion, a repricing of the risks given the range of possible outcomes, could see the demand/supply mix in global energy markets adjust, pointing to oil prices moving up to at least where fundamentals imply they should be. Our models indicate Brent Crude oil has scope to rise ~10-15% (see chart below). In FX, along with traditional safe-haven demand, this should be USD supportive given the US’ standing as a ‘net energy exporter’ and the USD’s positive correlation to oil prices.

In addition to fluid developments in the Middle East, there are several important macro focal points on this week’s radar such as the US ISM survey (tonight 3am AEDT), the China business PMIs (Weds), Australian GDP (Weds), US retail sales, and the monthly US jobs report (both Friday night AEDT). In our view, signs of stabilization in US activity and/or labour market conditions might compound the geopolitical backdrop and help the USD claw back more lost ground, particularly as it is still tracking below our ‘fair value’ estimate.

Trans-Tasman Zone

The Middle East geopolitical developments have dampened risk sentiment in early Asian trading (see above). This, and a firmer USD have exerted some downward pressure on the NZD (now ~$0.5950) and AUD (now ~$0.7040, ~1.4% below last week’s high). The AUD has also underperformed on the major cross-rates with falls of ~0.3-0.6% recorded against the EUR, GBP, NZD, and CNH, while there have been larger declines posted versus the JPY (-0.9%) and CAD (-1.1%).

As discussed above, the situation in the Middle East remains fluid and there is the potential for risk sentiment to remain on the backfoot given the prospect for an extended conflict, disruption to trade flows through the region, and/or a greater risk premium being priced into oil. In our view, the market jitters could keep the AUD weighed down in the near-term, particularly given its strong start to the year, with it tracking above our model estimate (we see ‘fair value’ now closer to ~$0.6950), the swing to traders being ‘net long’ AUD (as measured by CFTC futures contracts), and the negative growth/inflation implications for parts of Asia stemming from higher energy prices.

It is worth remembering that markets don’t move in straight lines, and the AUD has historically been a volatile currency (on average the AUD trades in a ~1% daily range, and it has swung around in an ~8 cent range the past few calendar years). While more heat may come out of the AUD in the short-run because of external forces, barring a sustained/acute bout of risk aversion, we don’t expect pull-backs in the AUD to be overly deep. This reflects the upward adjustment in Australian interest rate expectations/bond yields following the RBA’s recent rate hike and outlook for more due to sticky inflation pressures across the economy, as well as the fact Australia is also a net energy exporter. This in turn means that higher energy prices can be a supportive for Australia’s terms of trade (i.e. ratio of export to import prices) and the AUD over time. This week in Australia the macro focus will be on the Q4 GDP data (Weds). Signs private sector momentum picked up at the end of last year could reinforce market thinking that the RBA has more work to do to cool inflation, and this might help the AUD level off. Markets are discounting another RBA rate rise by August.