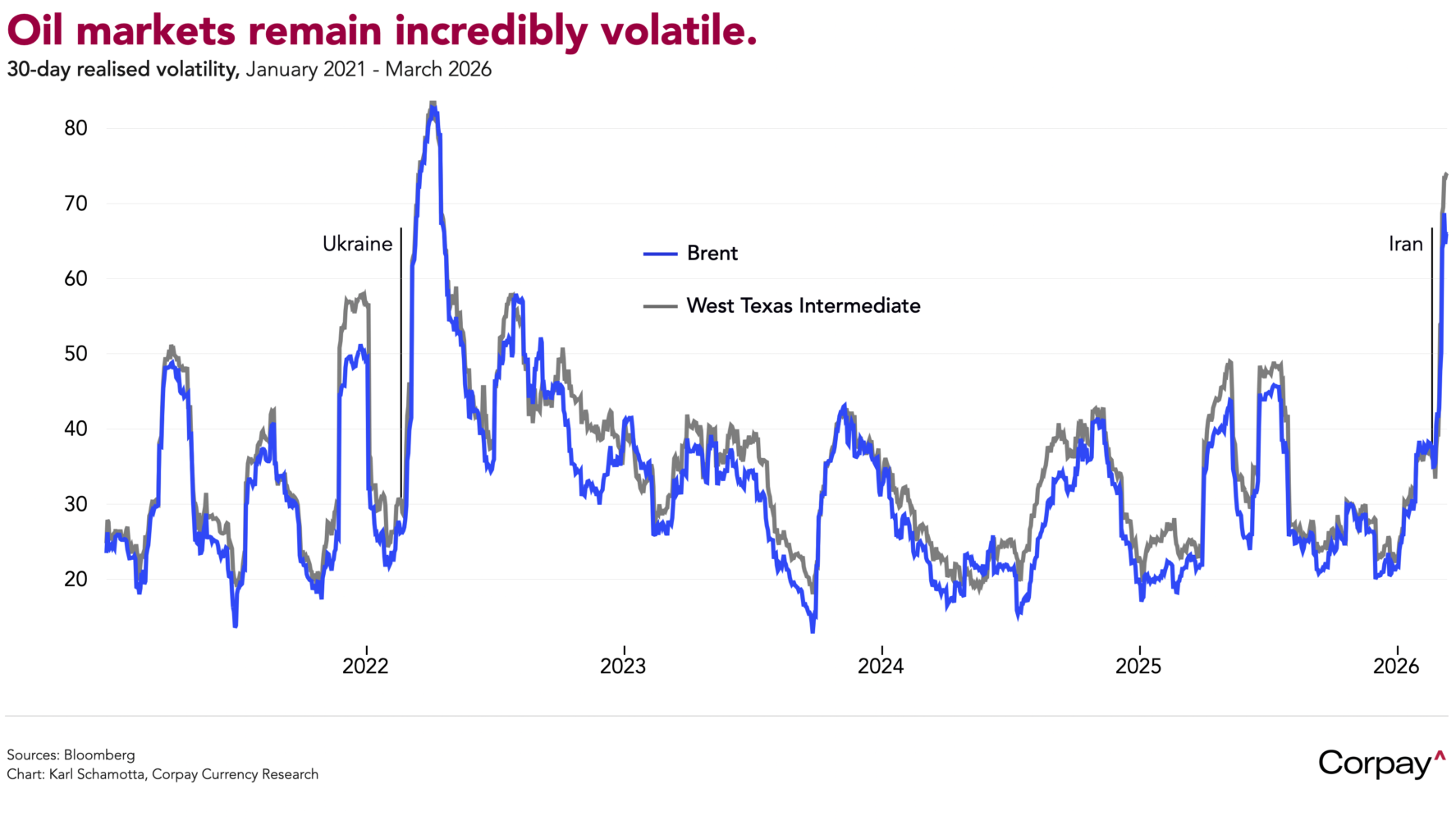

Good morning. The dollar is recovering from yesterday’s losses as crude prices ricochet higher following a series of Iranian strikes on energy infrastructure in the Persian Gulf and near the Strait of Hormuz. Brent and West Texas Intermediate are each up more than 3 percent on the session after a tanker was struck by a projectile in the Gulf of Oman, and drone attacks hit the United Arab Emirates’ Fujairah facilities and the Shah gas field. Crude markets remain remarkably volatile as downstream energy consumers scramble to secure supplies amid continued uncertainty over the scale and duration of the conflict.

The Australian dollar is firmer after the Reserve Bank delivered a well-telegraphed rate increase, almost fully unwinding last year’s easing cycle while signalling a hawkish shift in its reaction function. The economy is running with little slack and goods and services costs have risen sharply in recent months, prompting policymakers to warn of a “material risk” that price growth could overshoot target for longer than previously estimated, and Governor Michele Bullock warned of “second-round effects” on domestic inflation from the war in Iran. Traders are putting coin-toss odds on a third increase in May, with a move fully priced in by August.

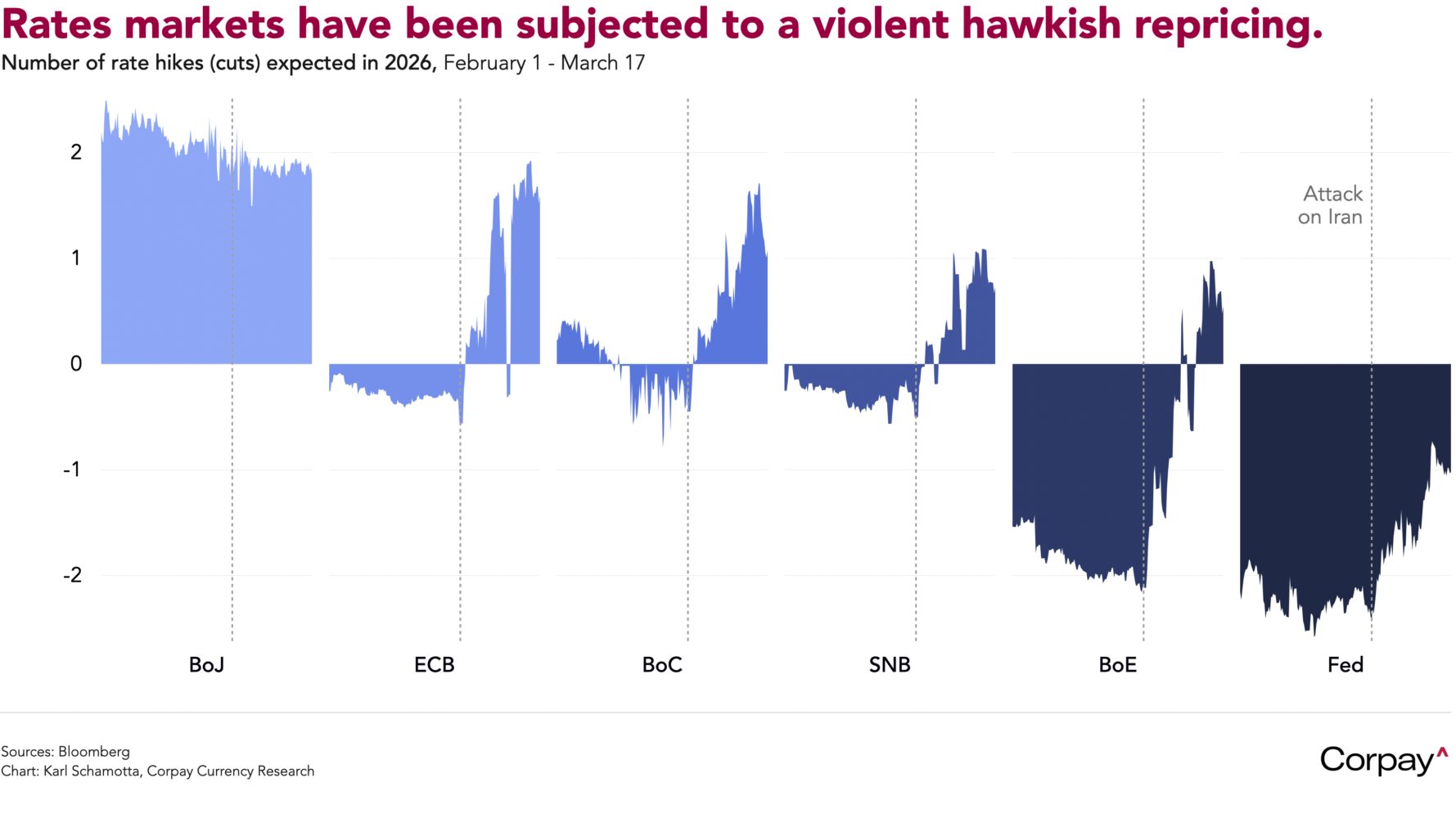

Markets are betting Australia isn’t an outlier. Policy expectations have climbed sharply across most advanced economies this month on anticipated inflationary fallout from the Middle East conflict, and cross-currency rate differentials have shifted dramatically, breaking key technical levels throughout the foreign exchange markets.

This repricing could prove excessive. Unlike in 2022, government household income supports have been withdrawn in most economies, savings cushions are depleted, labour markets are weak, and global manufacturing supply chains are operating near normal levels. Central bankers outside Australia could surprise markets in the coming days by signalling a commitment to following a long-established playbook of looking through commodity-led inflation to prioritise domestic growth. If so, rate curves could adjust lower as investors grow more pessimistic on the outlook, driving a number of major currency pairs back toward pre-war levels.

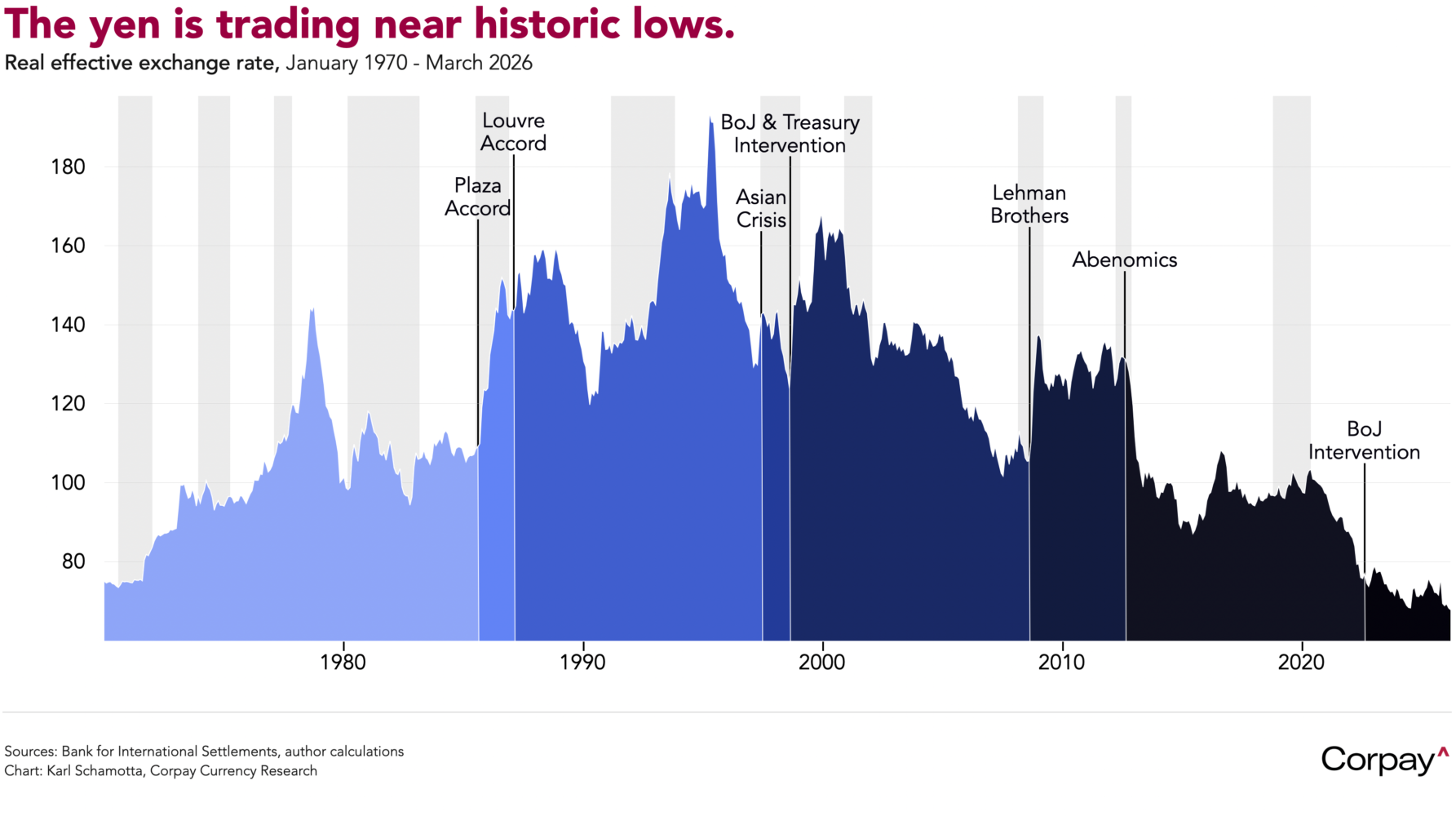

After weakening nearly 2 percent against the dollar since the war began, the Japanese yen is now trading near historic lows in trade-weighted inflation-adjusted terms. Selling pressure could carry the nominal dollar-yen pair through the 160 threshold in the coming days, yet looks unlikely to remain unchecked. Government jawboning is growing increasingly strident—Finance Minister Satsuki Katayama warned yesterday of “bold action” to support the currency, adding that officials were “fully prepared to respond any time” given the impact of exchange rates on households—and Bank of Japan Governor Kazuo Ueda could strike a more hawkish tone after this week’s meeting.

Bottom line: Iran-related inflation fears look overpriced in currency markets, while downside risks to global growth seem underpriced. A more sober reassessment may be approaching—and with it, another round of upheaval in foreign exchange.