The Federal Reserve’s preferred inflation measure landed in line with expectations in January, but left markets mostly unmoved, given that it predated the Iran conflict and was stale on arrival. Data released by the Bureau of Economic Analysis this morning showed the core personal consumption expenditures index rising 0.4 percent from the prior month, accelerating slightly to 3.1 percent on a year-over-year basis, matching economist estimates. The overall personal consumption expenditures index climbed 0.3 percent relative to the prior month, and was up 2.8 percent from a year ago, down slightly from December’s 2.9 percent pace. Personal income rose 0.4 percent month-over-month, up from 0.3 percent, and inflation-adjusted household spending held at 0.1 percent, with both matching forecasts. Separate data updates saw fourth-quarter gross domestic product unexpectedly revised lower to 0.7 percent and January durable goods orders slowing more than anticipated.

Markets expect inflation to climb sharply in the months ahead. Average US gasoline prices are up 65 cents a gallon since the war in Iran kicked off, and one-year breakevens—which measure the gap between nominal Treasury yields and their inflation-linked equivalents—have jumped to their highest levels since 2022, signalling that investors think rising fuel costs will translate into higher headline inflation measures.

The Canadian dollar is down sharply after Statistics Canada reported a larger-than-expected drop in employment last month. The economy shed 83,900 jobs across the private and public sectors, pushing the unemployment rate from 6.5 to 6.7 percent in February, disappointing economists who had expected a more modest increase, and suggesting that uncertainty is sapping momentum. Rate differentials between Canada and the US are narrowing as traders scale back expectations for a return to tightening from the Bank of Canada later this year, but a rate hike remains priced in for October, indicating—to us at least—that further adjustment is necessary.

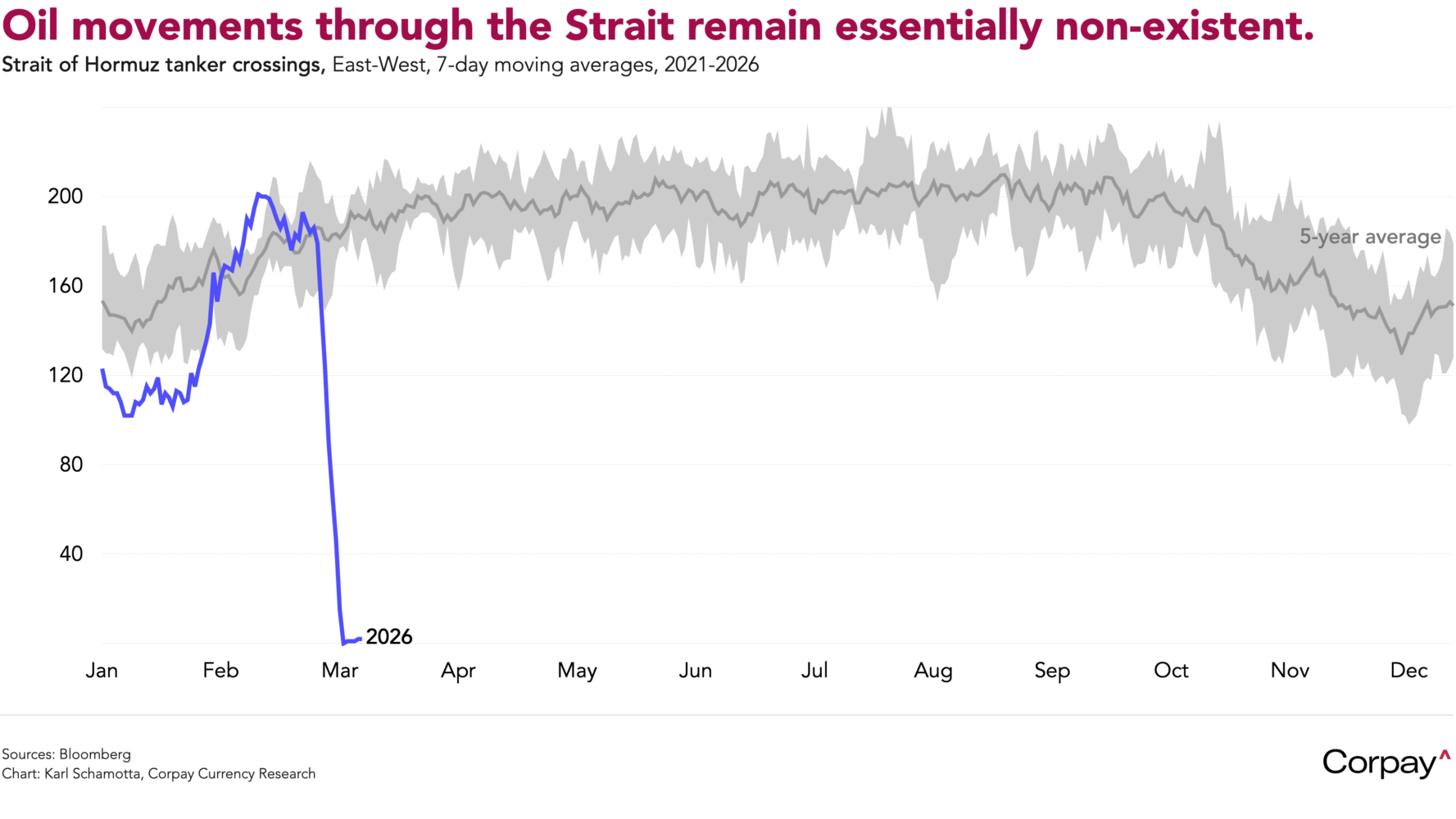

The US dollar is advancing more broadly as market participants bet on a slower easing cycle from the Fed and build short positions against those currencies most exposed to higher energy costs. With shipping through the Strait of Hormuz reduced to a trickle, inventories falling and downstream buyers growing desperate, importers are coming under sustained selling pressure, driving the euro below the psychologically important 1.15 level and the yen toward the 160 mark that has previously prompted official intervention.

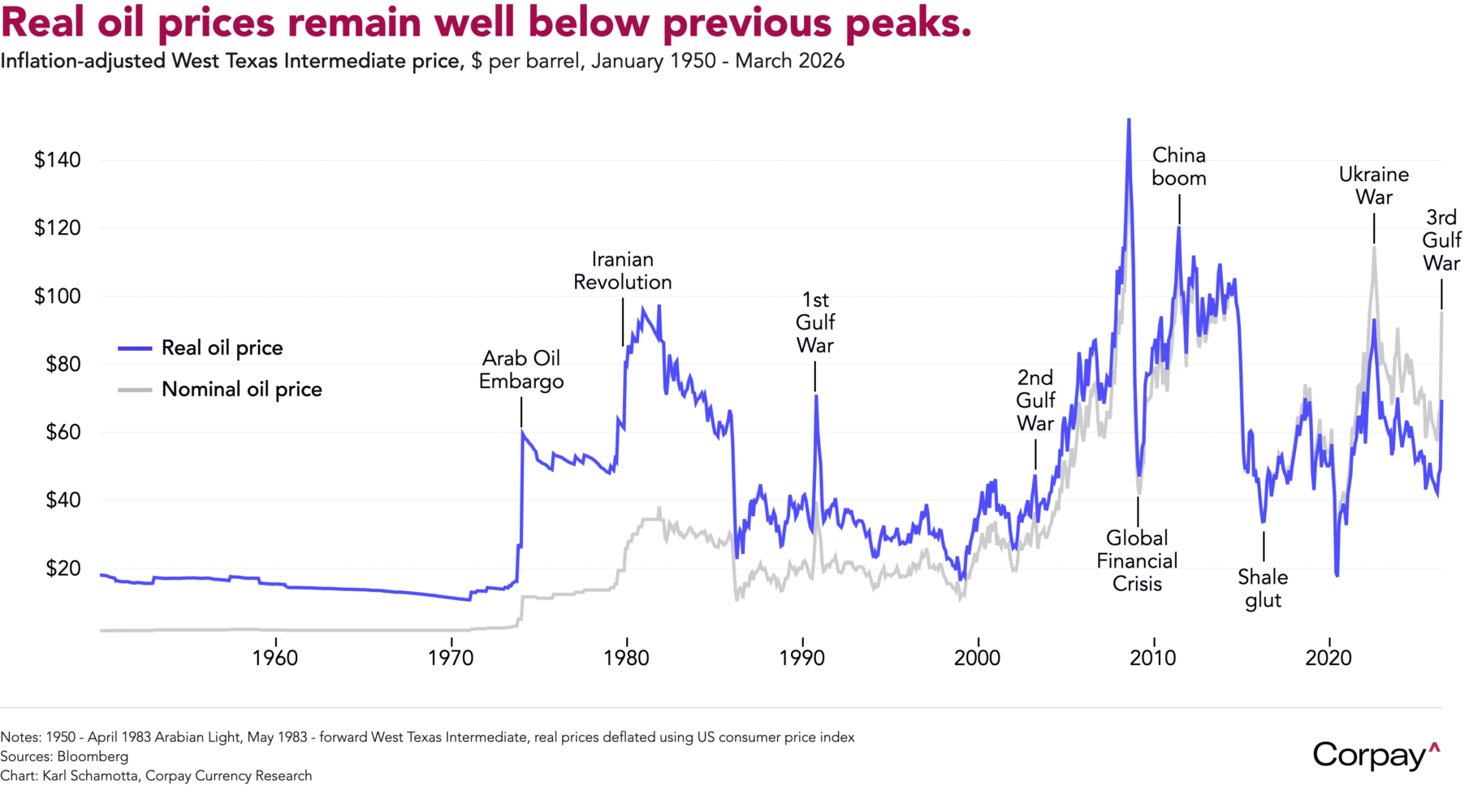

This is not an oil shock—not yet. Oil intensity, the ratio of consumption to economic output, has fallen sharply in recent decades as transport and manufacturing have grown more efficient and activity has shifted towards intangible services, meaning that the real economy is better insulated than in previous cycles. Inflation-adjusted levels also remain well below previous peaks.

But for every day the Strait remains closed, the costs grow: consumer inflation expectations could become unanchored, growth could suffer as income shifts from consumers to producers, and political pressure could mount on the president as voters rebel. We could be letting hope triumph over experience (as Oscar Wilde observed about second marriages), but we think market participants should be prepared for a diplomatic face-saving agreement that eases tensions and triggers a violent reversal in major currency pairs. Market orders and currency options should be very much part of the hedgers toolkit at this juncture.