• Solid run. US equities rose on Friday, as did bond yields. USD index tread water. Commodity currencies (AUD, NZD, CAD) strengthened.

• Central banks. No change by RBA (Tues), however tone could be ‘hawkish’. US Fed (Thurs morning) set to cut rates but may not signal another near-term move.

Global Trends

Markets had a relatively quiet end to last week with a string of government shutdown delayed US data points not really moving the needle. In terms of the numbers US equities edged up with the broader S&P500 (+0.2%) within striking distance of its record highs. Bond yields also rose a little with US rates up ~3-4bps across the curve. Despite the more recent rebound the benchmark US 10yr yield remains below its 6-month average. Elsewhere, WTI crude oil nudged back over US$60/brl and copper prices increased (+1.7%).

In FX, the USD index consolidated with EUR (now ~$1.1642) and GBP (now ~$1.3329) treading water, and the interest rate sensitive USD/JPY tracking the lift in bond yields (now ~155.25). NZD drifted a little higher to now be ~3.6% above its November low point (now ~$0.5782) and the AUD extended its upswing (now ~$0.6637, a high since mid-September). The CAD outperformed (USD/CAD is down at ~1.3833) after the Canadian jobs report blitzed analysts’ expectations for the third straight month. Robust jobs growth and drop in Canada’s unemployment rate to 6.5% (a low since mid-2024) has reinforced views the Bank of Canada’s rate cutting cycle might be over. The BoC holds its last meeting of the year this week (Weds night AEDT).

In terms of the US economic releases, the delayed readings on personal spending for September showed activity was positive but sluggish at the end of the quarter, and that price pressures remain contained (the core PCE deflator (the Fed’s preferred inflation gauge) slipped down to 2.8%pa). More timely readings of US consumer confidence indicated sentiment improved in December, however it remains at low levels with labour market worries and cost of living pressures still front of mind for households.

In the US this week the September/October JOLTS job openings data is released (Tues night AEDT) and the Federal Reserve meets (Thurs morning AEDT). The US Fed is divided, and a split decision looks likely, though markets and surveyed economists think the core of the committee should vote in favour of another 25bp interest rate cut. To appease the more ‘hawkish’ members of the committee and get another rate cut over the line this week we believe the statement and Chair Powell’s press conference may indicate that another move in early 2026 is data dependent and not locked in. We believe this combined with where market pricing now sits and an assumption the Fed’s macro projections don’t change that much could see the USD recoup some lost ground in the near-term.

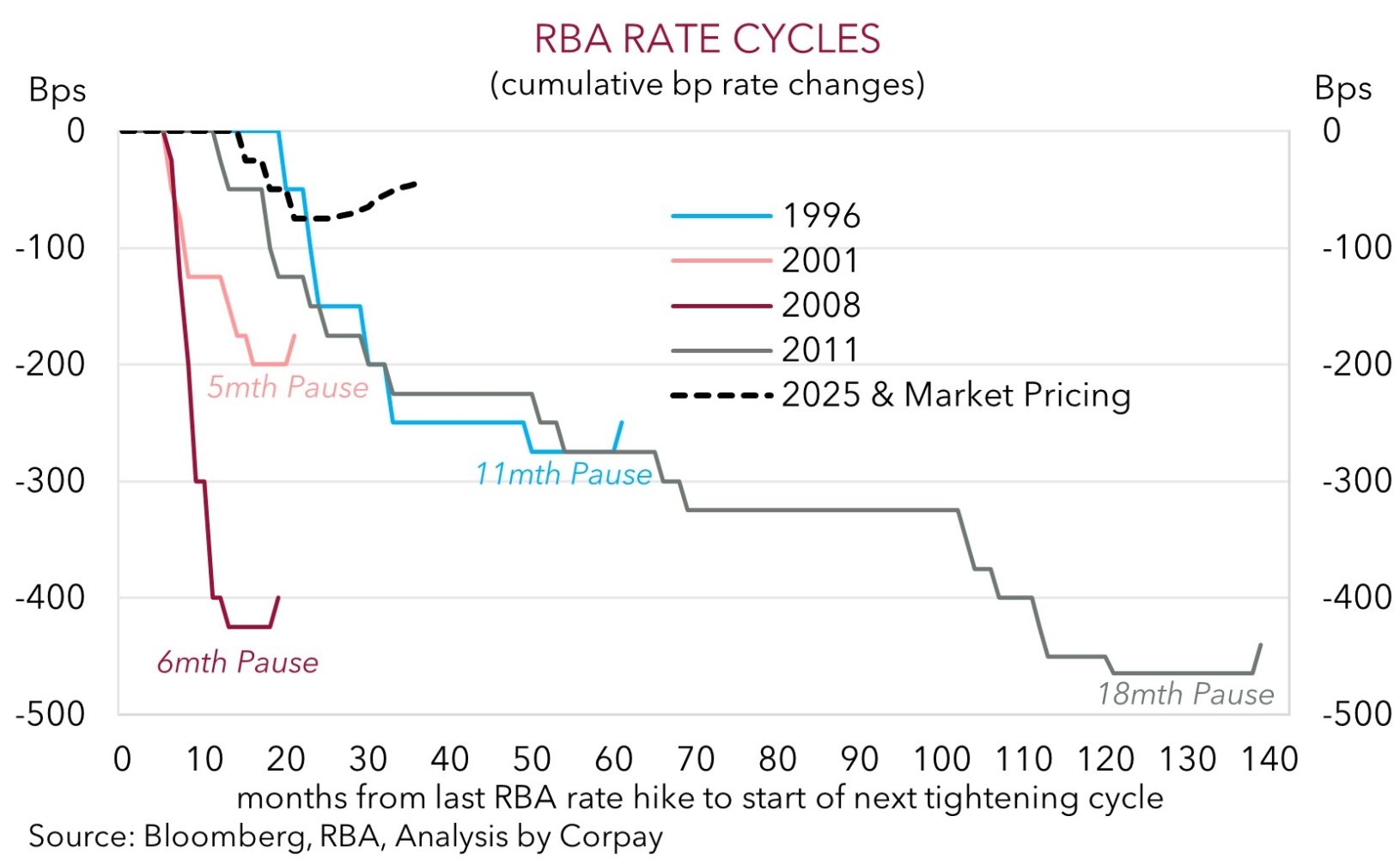

Trans-Tasman Zone

The mix of subdued market volatility and a still upbeat tone across cyclical/risk assets (as illustrated by the lift in equities and base metal prices) supported the AUD and NZD at the end of last week (see above). At ~$0.5782 the NZD is ~3.6% above the low touched around the RBNZ’s late-November meeting where it cut interest rates but gave hints the move could be the last this cycle. New RBNZ Governor Breman hosts her first media briefing later this week (Weds morning AEDT).

The AUD’s (now ~$0.6637) upturn has extended with it tracking around its highest level since mid-September. The backdrop has also helped the AUD on most of the major crosses with gains of ~0.2-0.5% recorded against the EUR, JPY, GBP, NZD, and CNH on Friday. At ~0.5701 AUD/EUR is at a ~4-month high, AUD/GBP (now ~0.4980) is near the upper end of its multi-month range, AUD/NZD (now ~1.1497) is within ~1.5% of its cyclical peak, AUD/CNH (now ~4.6922) is north of its 1-year average, and AUD/JPY (now ~103.07) is at levels last traded in mid-2024.

We feel AUD volatility should pick up this week given the RBA meeting (Tues AEDT), US Fed meeting (Thurs morning AEDT), and Australia jobs data (Thurs AEDT). In terms of the RBA, we and all surveyed analysts expect the cash rate to be held at 3.6%, however based on the run of Australian GDP, employment, and inflation data we think the post-meeting statement and Governor Bullock’s press conference might sound more ‘hawkish’, reflecting the shift in the distribution of risks to the monetary policy outlook (i.e. the chances of a rates needing to rise are higher than the probability of a more rate cuts coming through). Comments suggesting the RBA may be openly thinking about the need to raise interest rates again could, in our opinion, give the AUD some more near-term support. However, this (and another solid Australian jobs report) might generate more of a lasting impact on the AUD cross-rates rather than AUD/USD. As discussed above, we believe the USD could recover lost ground later this week if the US Fed cuts interest rates but sounds a bit more ‘cautious’ about the need to deliver another rate reduction in early-2026. Outcomes compared to expectations drive markets and traders are assigning a ~95% chance the US Fed lowers interest rates by 25bps this week with another move after that not fully factored in until June.