Good morning. Oil prices jumped and currency markets slid back into risk-aversion mode last night when Donald Trump claimed the US-Israeli war against Iran was “nearing completion” but failed to offer a clear timeline and threatened more attacks. In a 19-minute address from the White House, the president said “We are on track to complete all of America’s military objectives shortly, very shortly,” yet “We are going to hit them extremely hard. Over the next two to three weeks, we’re going to bring them back to the Stone Ages, where they belong”. Both global crude oil benchmarks are up more than 7 percent relative to yesterday’s close, the US dollar is punching higher, Treasury yields are climbing, and stock futures are sliding as a stagflationary shock to the US and global economies grows more likely.

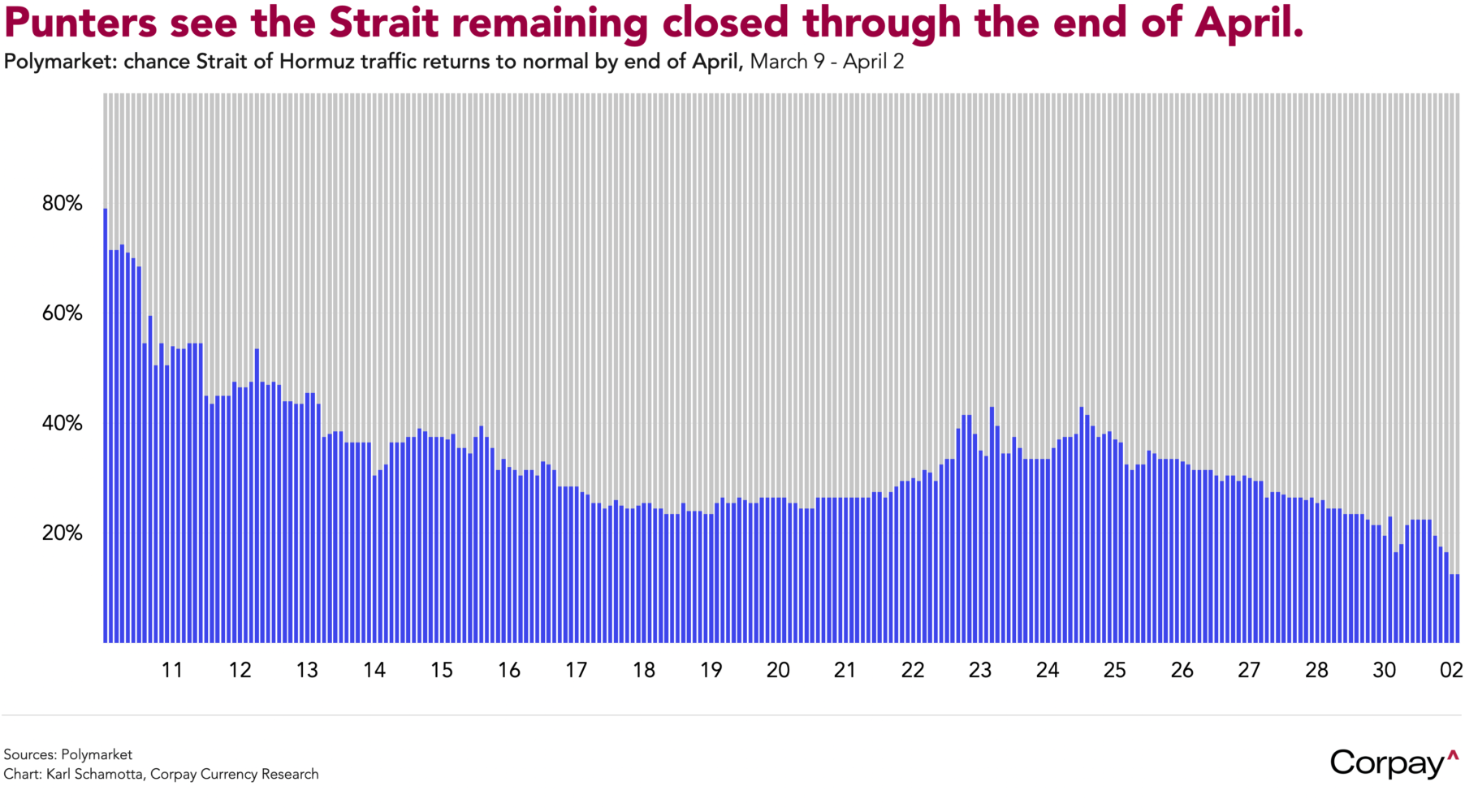

Punters* are betting on a prolonged disruption in the Strait of Hormuz. According to data published by the Polymarket prediction market, bettors are assigning just 13 percent odds to a reopening of the Strait by the end of April, and only 38 percent by the end of May, implying a prolonged period of painfully-high energy prices.

This looks overdone. In my view**, the geopolitical calculus still points to a unilateral US declaration of victory and a pullback in airstrikes, followed by an end to Iranian attacks on shipping. With gas prices above $4 a gallon, midterm elections looming in November, and his self-imposed timeline for ending Operation Epic Fury all but expired, the president has every domestic incentive to claim that the core strategic objectives of the campaign—the destruction of Iran’s navy, missile infrastructure, and nuclear enrichment capacity—have been met, even if the regime remains intact and emboldened. Participants in larger, more established, and more sophisticated markets are well aware of this, and are broadly avoiding directional positions that could turn sour if hostilities were to end.

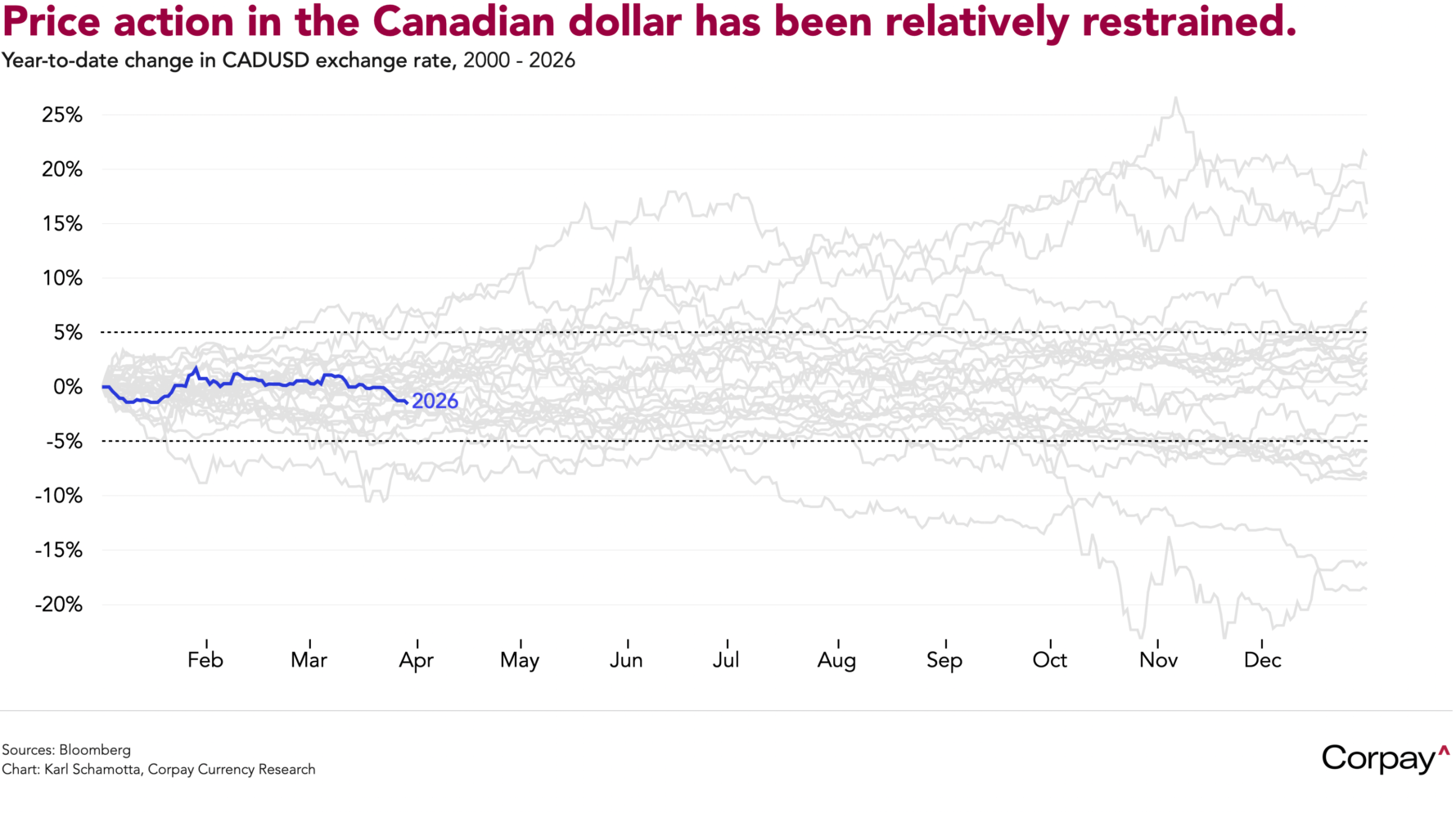

The Canadian dollar has traded in a remarkably narrow band since the outbreak of the war on Iran in late February, drifting modestly lower despite the dramatic upheaval in global energy markets. On one hand, surging crude oil prices—up more than 40 percent from pre-conflict levels—have provided a natural tailwind for the loonie, given Canada’s status as the world’s fourth-largest oil producer and a net energy exporter. Yet that support has been almost perfectly offset by a renewed wave of safe-haven demand for the US dollar, which staged its largest two-day rally in nearly a year when hostilities began, while lingering uncertainty from Washington’s tariff regime and the Bank of Canada’s increasingly constrained monetary policy outlook have further capped any meaningful appreciation. For now, traders are lacking the conviction needed to push it decisively in either direction, but that could change—likely in a bullish direction—in the event of a shift in the narrative surrounding the war.

Liquidity conditions will deteriorate over the coming days as the Easter holidays thin out trading. US bond markets close early today, equity markets shut tomorrow, and both reopen on Monday. Most European and Asian markets are closed tomorrow and Monday. Foreign exchange markets will remain open throughout, but volumes will be low and price action could be erratic—conditions that, on the margins, tend to support safe-haven currencies like the dollar and Swiss franc.

Against that backdrop, tomorrow’s non-farm payrolls report could move exchange rates. The data won’t yet capture the war’s impact on employment, but will shed light on how healthy labour markets were before it hit. Earlier in the week, the Institute for Supply Management said its manufacturing employment index was little changed at 48.7, yesterday’s ADP payrolls number came in stronger than expected, and today’s initial jobless claims print did the same, leading economists to think roughly 65,000 jobs were added in March***. Unemployment is expected to hold at 4.4 percent, with any material jump likely to have an outsized impact on Federal Reserve policy expectations.

*”Punter” is British slang for a person who gambles or makes risky investments. I didn’t know until this morning that it also refers to the person on a football team with the lowest likelihood of getting injured, and am now considering a career change.

**I’ve been wrong so far. This business is a humbling one.

***The “whisper” number—the unofficial estimate circulated by trading desks—is likely closer to 40,000.