• US tariffs. US Supreme Court rules against Pres. Trump. US tariffs being rejigged. USD softer. AUD & NZD a little firmer. AUD still near multi-year peak.

• Macro trends. Over medium-term reworking tariff policies may be US growth & USD supportive. This week AU inflation data due. RBA Gov. Bullock speaks.

Global Trends

US tariff developments were in focus on Friday and the weekend. The US Supreme Court struck down tariffs imposed by President Trump under the International Emergency Economic Powers Act (IEEPA). The 6-3 decision was somewhat anticipated given President Trump’s move to bypass Congress (which has control over taxes) when implementing these levies last year; hence the knee-jerk market reaction was relatively muted. The USD dipped a little, but it was already under a bit of pressure because of weaker government shutdown impacted US GDP data and softer US PMIs, while US equities rose (S&P500 +0.7%) and bond yields ticked up (US 10yr +1bp). The US economy expanded at a tepid 1.4% annualised pace in Q4, though the prolonged shutdown meant government spending was a sizeable drag which should mechanically rebound in Q1.

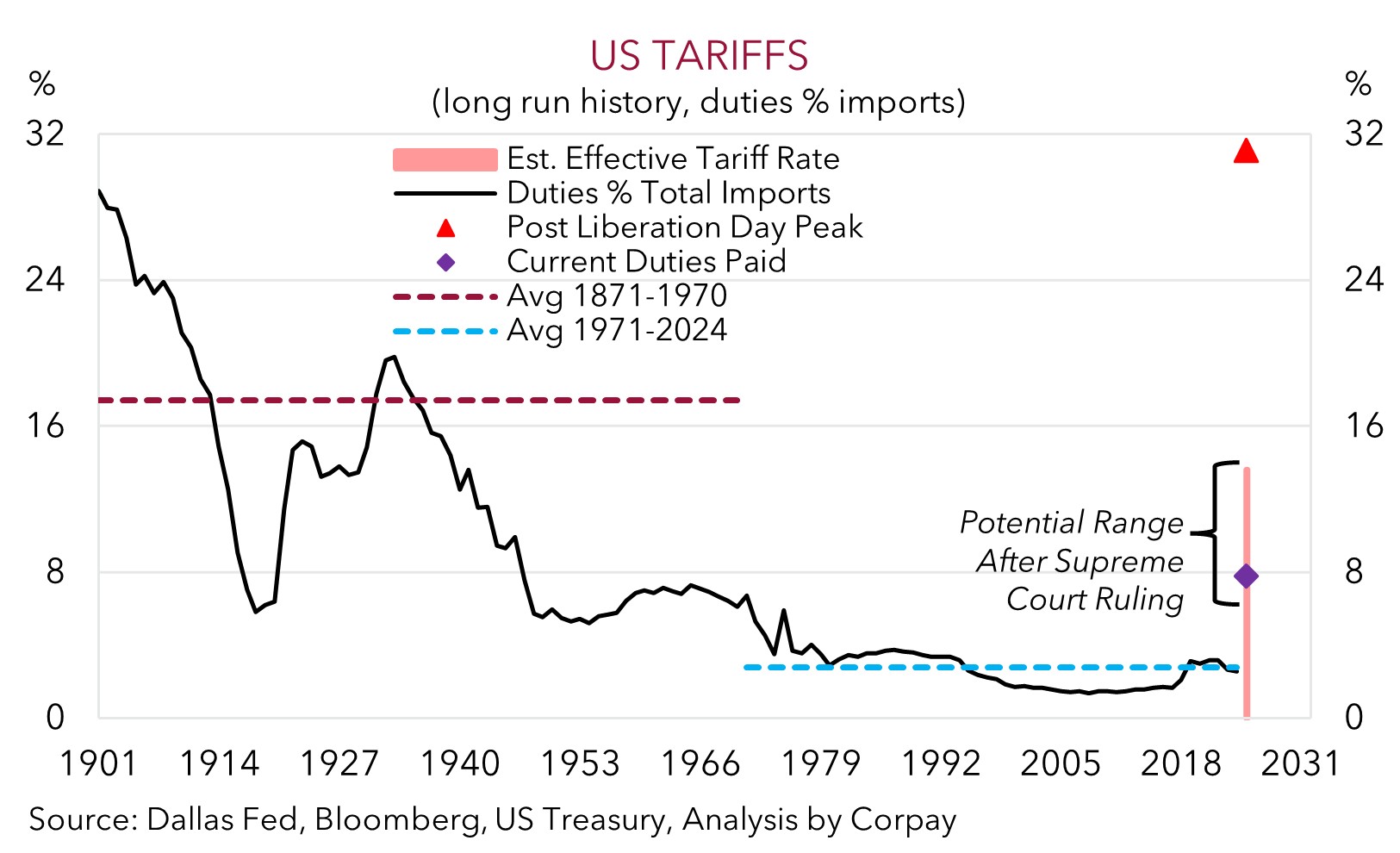

In response, and in an effort to preserve his trade agenda, President Trump initially announced a 10% tariff on all imports under Section 122. This was subsequently raised to 15%. These tariffs are a stop-gap and can stay in force for up to 150 days. New country and product specific investigations have been announced under other mechanisms, setting up the probability of tariffs remaining over the medium-term. On balance, the US’ Effective Tariff Rate (i.e. the average across all imports) may lift a little while the temporary blanket tariffs are used, but it could end up being lower than it has been down the track because of constraints created by the path that needs to be used. As the chart shows, things are a long way from ‘peak tariff’ hit around ‘Liberation Day’.

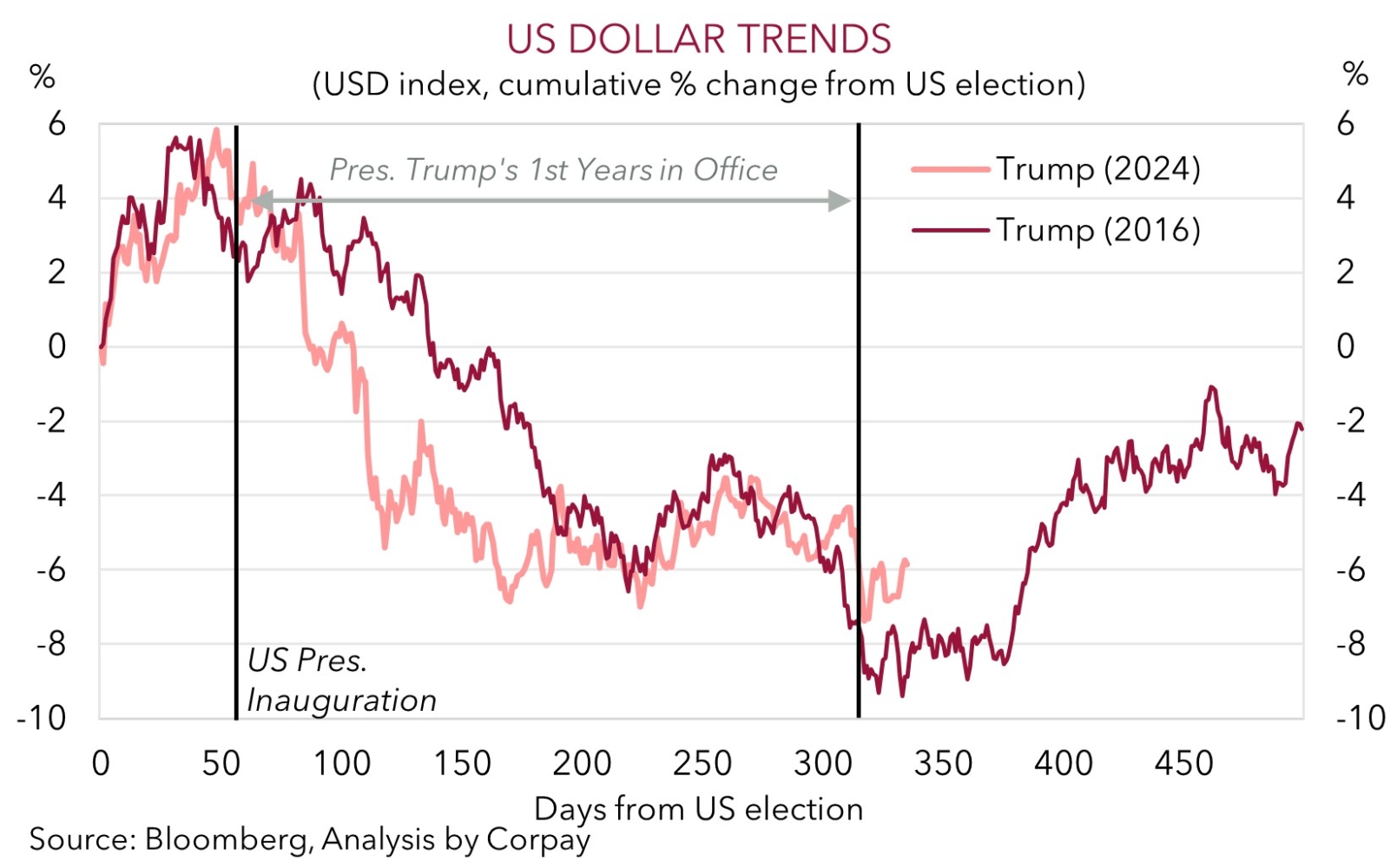

There are a lot of moving parts, and more news/headline driven volatility is likely over the period ahead. President Trump holds his State of the Union address this week (Weds 1pm AEDT). In the short run, the USD may remain on the backfoot, however, longer-term, we think the reworking of the US’ tariff policies could end up giving the USD a boost. (1) The Supreme Court decision shows checks and balances remain in place. This might ease global investors’ worries about allocating funds to the US. (2) Concerns about US growth due to the higher import duties, and what this means for jobs, has weighed on the USD over the last year because it opened the door to more US Fed rate cuts. This drag might lessen going forward (or reverse course if tariff refunds are paid out), and it may mean the US fiscal impulse because of tax cut extensions etc is larger. This, and a snapback following the US government shutdown, points to potentially stronger US growth, which would be helpful for jobs, limiting the US Fed’s ability to lower rates much more. Interestingly, a levelling off and recovery in the USD (which is tracking below our ‘fair value’ model) also started to happen around this point in President Trump’s first term (see second chart below).

Trans-Tasman Zone

USD tariff and macro developments have been in the spotlight the past few days (see above). As outlined, the slightly softer USD, coupled with last week’s positive Australian labour market report has helped the AUD (now ~$0.7083) tick up a bit, with the AUD still hovering near the upper end of its multi-year range. The NZD has also nudged up (now ~$0.5982) following its weaker run in the wake of the ‘not as hawkish’ as anticipated RBNZ guidance. On the crosses, the AUD has outperformed with gains of ~0.2-0.4% recorded against the EUR, JPY, GBP, NZD, CAD, and CNH at the end of last week. At ~0.60 AUD/EUR is around levels last traded in March 2025; AUD/NZD (now ~1.1840) is at the top end of the range occupied since mid-2013; AUD/JPY is near cyclical highs (now ~109.76); AUD/GBP (now ~0.5251) is close to a ~19-month peak; and AUD/CNH (now ~4.8877) is within striking distance of its multi-quarter top.

In Australia this week, the January monthly CPI inflation data is due (Weds), and RBA Governor Bullock speaks (Weds night). Data wise, headline inflation will be boosted by the unwinding of the remaining electricity subsidies, but it could be offset by softer fuel and travel prices and some policy changes that may weigh on health and childcare prices. Core inflation is projected to remain above the top of the RBA’s target band (mkt 3.3%pa). If realised, this and more ‘hawkish’ rhetoric by Governor Bullock might reinforce market expectations looking for another RBA rate hike, with another move close to fully factored in by June and ~44bps of tightening baked in by year-end.

From our perspective the upward repricing in RBA interest rate expectations may have largely run its course as an AUD tailwind. Outcomes compared to expectations drive markets. Based on this framework, with the negative impacts from higher interest rates set to materialise across the Australian economy later this year, and prospect of a rebound in the USD due to the rejigging of the US’ tariff policy (see above), we remain of the opinion that ~$0.71-0.72 might be a ceiling for the AUD. Equally, the shift up in the level of interest rates and swing in interest rate differentials in Australia’s favour could also limit how deep and long-lasting AUD pull-backs may be without an acute bout of risk aversion. On net, we see the AUD tracking in a higher average range than what it has over the past few years (recall, over 2024/25 the AUD averaged ~$0.6520).