Inflation slowed in the United States last month—before the war in Iran sent oil prices spiralling higher and triggered a sharp reappraisal of the Federal Reserve’s expected policy path. According to data published by the Bureau of Labor Statistics this morning, the core consumer price index—with highly-volatile food and energy prices excluded—rose 0.2 percent in February from the prior month, decelerating slightly from January’s 0.2-percent increase, and rising 2.46 percent over the same period last year—marking a five-year low. This was in line with consensus estimates among economists polled by the major data providers ahead of the release. On a headline all-items basis, prices climbed 0.27 percent month-over-month, rising from the 0.2 percent pace set a month earlier, and were up a relatively-sedate 2.41 percent year-over-year.

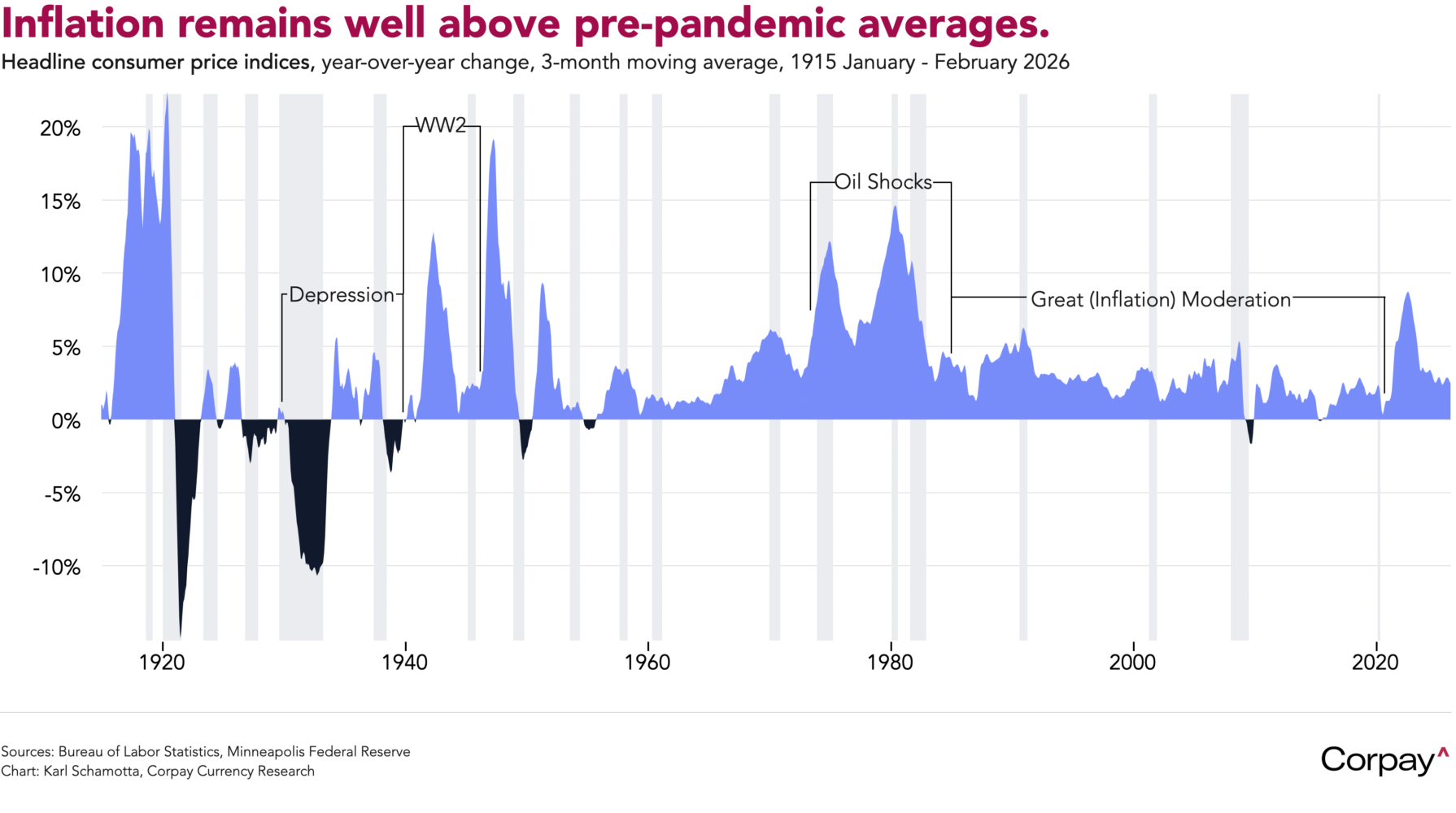

Next month’s print is likely to show headline inflation running above 3 percent on a year-over-year basis, well above pre-pandemic averages, and firmly outside the Fed’s comfort zone. Policymakers will attempt to look through the—likely temporary—impact that dramatic increases in energy costs and methodological factors relating to last year’s government shutdown have on price measures, but will remain wary of a jump in consumer inflation expectations, and are unlikely to deliver a clear easing signal until the psychological blow has passed.

Treasury yields are holding firm on the policy-sensitive front end of the curve, equity futures are pointing to a flat open, and the dollar is inching higher against its major rivals.

Oil prices remain incredibly volatile. After swinging between $120 and $85 a barrel on Monday, Brent crude plunged almost 20 percent—only to jump higher—yesterday when Energy Secretary Chris Wright posted and later deleted a social media claim that the US Navy had successfully escorted a tanker through the Strait of Hormuz. Unconfirmed reports that Iranian forces had begun laying mines in the waterway—something that could disrupt shipping for months—drove a further rise overnight.

The turmoil will continue. Group of Seven leaders are expected to agree in coming hours to release several hundred million barrels from strategic petroleum reserves, but the impact will be limited by the pace at which oil can reach markets. Traders expect a total release of 300-400 million barrels, far larger than anything previously attempted, but most credible estimates suggest logistical constraints will limit the flow rate to less than 1.3 million barrels daily, well short of the 12-15 million barrels currently off the market due to the conflict.

Currency markets are still moving in reaction to changes in energy prices, with the US, Canadian, and Australian dollars outperforming the euro, pound, and yen as investors bet net importers will suffer more deleterious economic effects in the months ahead. On the face of it, this seems a reasonable bet: the euro area, United Kingdom and Japan are all suffering a profound deterioration in commodity-based terms of trade, and will see net export balances tilting in a negative direction if benchmarks remain elevated. We would, however, note that US domestic politics are far more sensitive to gasoline prices, meaning that this episode could have far-reaching consequences for the upcoming mid-term elections and economic policymaking thereafter. US shale producers may have helped insulate overall corporate earnings against big jumps in global energy costs, but consumers still have many more votes, and we can’t rule out an eventual return to the typical inverse relationship between oil prices and the US dollar.