• Positive vibes. ‘Glass half full’ markets buoyed by US/Iran comments. US equities rose, oil fell. USD weaker. AUD & NZD claw back some lost ground.

• Economic reality. Still more water to go under the bridge. Impacts of energy supply shock yet to show. More bursts of volatility likely over coming weeks.

Global Trends

After a challenging few weeks for risk sentiment, markets ended March on a more positive note. As has been the case for the past month developments in the Middle East have been in the driver’s seat. Hopes the conflict with Iran may be heading towards a diplomatic ‘off ramp’ after a few encouraging comments boosted the market mood. Media reports President Trump is willing to end the US’ actions even if the Strait of Hormuz remains largely shut were added to by Iran’s President Pezeshkian who indicated they have “the necessary will” to halt hostilities, if demands are met such as authority over the Strait.

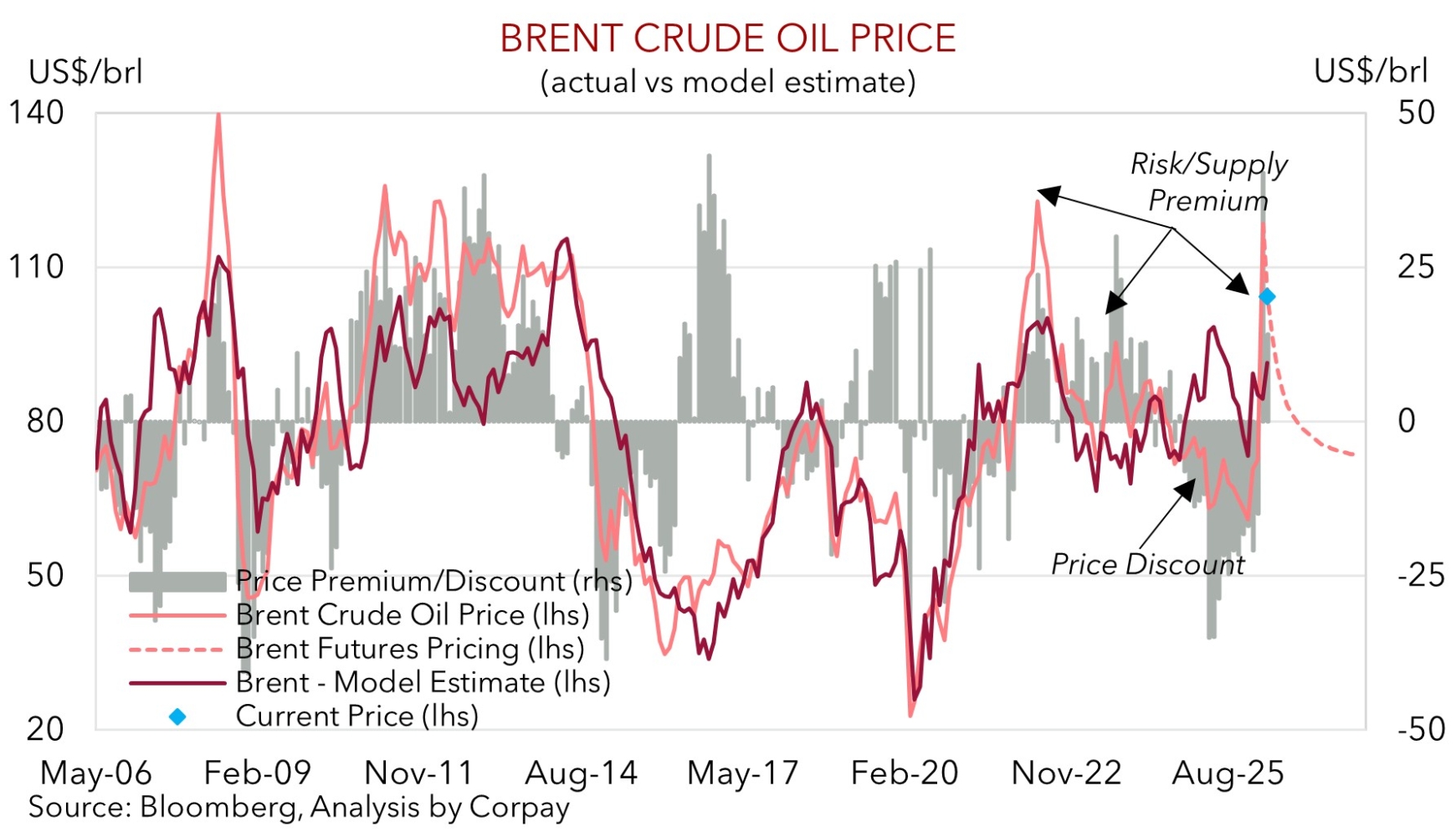

Short-sighted markets were buoyed by the constructive tone, which in part looks to have compounded month/quarter end portfolio rebalancing flows by asset allocators. The US S&P500 rose 2.9% overnight, although this wasn’t enough to stop it recording its largest monthly fall (i.e. 5.1%) since March 2025. Energy prices fell with brent crude oil shedding almost ~5%. That said, at ~US$103.65/brl, brent crude remains ~75% above mid-December levels. Bond yields eased with US rates ~3bps lower across the curve. In FX, the USD index weakened a bit. EUR (the major USD alternative) edged up (now ~$1.1552), as did GBP (now ~$1.3228), while USD/JPY dipped (now ~158.75). The NZD ticked higher (now ~$0.5745), and so did the AUD (now ~$0.6896). However, much like other asset classes the overnight swings only partially unwound moves that occurred over March. The USD index remains near the upper end of the range it has occupied since last May.

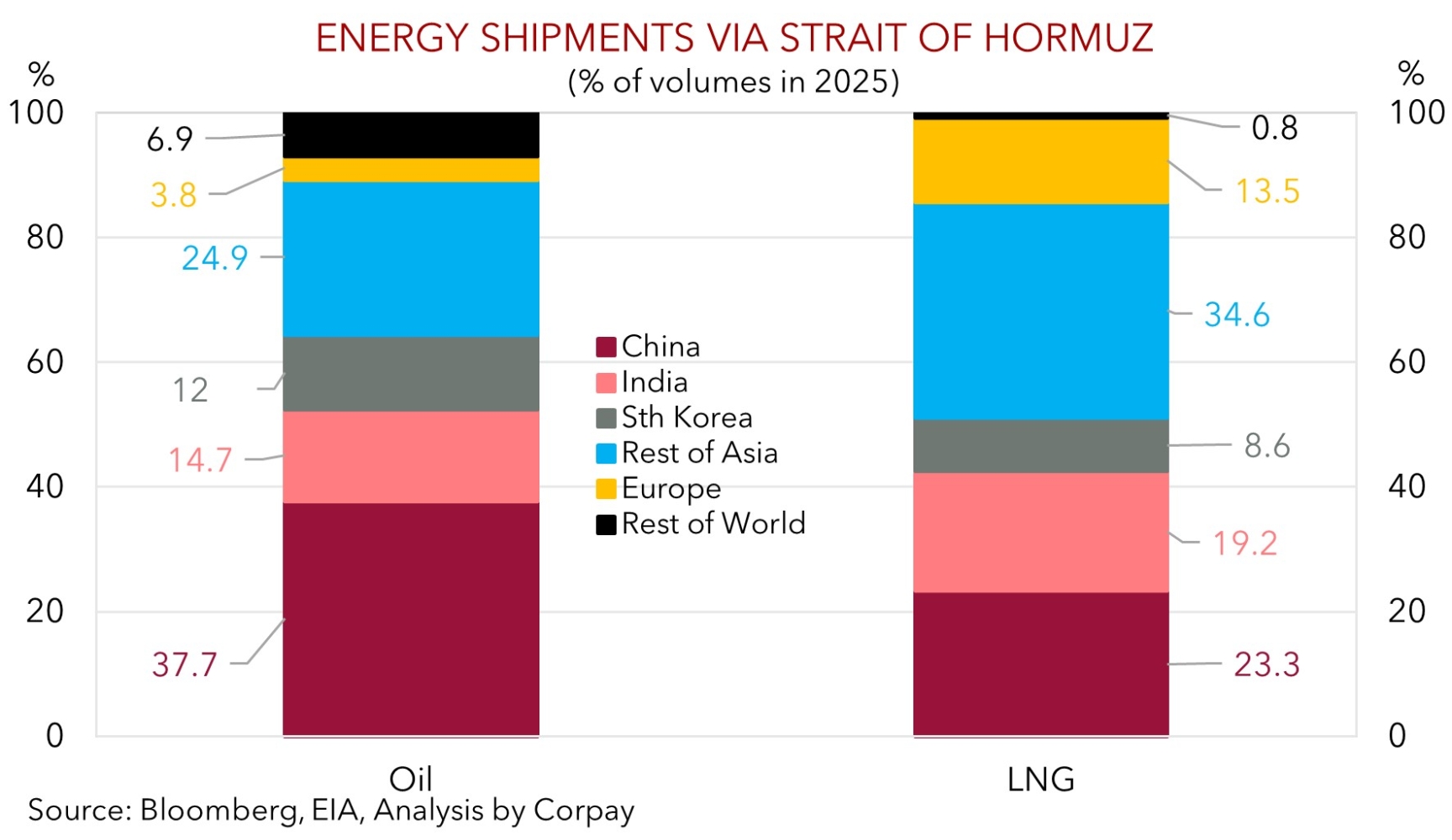

The more positive market vibes may not last. As seen over recent weeks the Middle East situation is volatile. We would also stress that underlying issues important for the global economy remain such as when/if the flow of energy/vessels via the Strait of Hormuz restarts or gets back to where it was before the conflict. Notably, according to President Trump nations reliant on energy from the Middle East should take responsibility for reopening the Strait of Hormuz themselves, suggesting effects on the real world are still closer to beginning than the end. As our chart shows, ~80-90% of the oil/gas shipped via the Strait of Hormuz is sent to Asia, the engine room of the global economy. The surge in energy prices is starting to show up in inflation data with Eurozone CPI jumping from 1.9%pa to 2.5%pa in March. The economic fallout from the conflict is in its infancy. Disruptions to energy supply might take months/quarters to clear up, and this will only begin to improve once the conflict definitively ends. We believe volatile risk markets coupled with the higher level of oil prices (because the US is a ‘net energy exporter’) could keep the USD elevated for a while yet. Tonight in the US, ADP employment (11:15pm AEDT), retail sales (11:30pm AEDT), and the ISM manufacturing index (1am AEDT) are due.

Trans-Tasman Zone

The swings in risk sentiment and more positive tone across growth assets such as equities overnight, combined with a softer USD have helped the NZD and AUD claw back a bit of lost ground (see above). That said, at ~$0.5745 the NZD is still near the lower end of its ~3-month range and ~5.7% from its late-January peak. Similarly, the AUD (now ~$0.6896) is only back where it was tracking last Friday and ~4% from its March multi-year highs. The AUD also ticked up a little on most of the major cross-rates with gains of ~0.1-0.6% recorded against the JPY, GBP, NZD, CAD, and CNH the past 24hrs. By contrast, AUD/EUR (now ~0.5972) tread water close to its year-to-date average.

Looking ahead, there are no local economic releases which are typically market moving scheduled until after the Easter holiday period. The next monthly Australian jobs report is due on 16 April, while in NZ the RBNZ meets next week (8 April) where no change in interest rates is anticipated. As outlined before, the surge in oil/fuel will mechanically push Australian headline inflation much higher in March/April. After that there could be spillovers across parts of the CPI basket like airfares, and if firms in fuel-intensive industries such as agriculture, logistics, construction, and manufacturing pass on higher costs. Given sticky inflation is already an issue we believe the RBA should deliver ~1-2 more rate rises this cycle. Markets continue to factor in a more aggressive outlook with ~60bps of hikes priced in by next February. A May rate rise is assigned a ~67% chance of happening.

As mentioned, more twists and turns are likely in the Middle East, and a lot of the negative economic aftershocks are still in the pipeline. Inline with our warnings in March, we remain of the opinion that there are more downside than upside risks for the AUD in the short-term. In our view, based on the fragile situation in the Middle East, how much more RBA tightening is already discounted, the looming global growth slowdown, and with the negative domestic consequences of higher mortgage rates and fuel costs still to come upside in the AUD could be capped and fundamental downside pressures remain in place.