• Improved mood. Despite ongoing Middle East issues & high oil prices risk sentiment has improved. Softer USD & a RBA hike supports the AUD.

• RBA hikes. Another 25bp rate rise delivered yesterday. Inflation pressures point to another move. Markets already pricing that in. Growth set to slow.

Global Trends

The market mood has picked up over the past couple of sessions, as illustrated by the uptick in equities (US S&P500 +0.3%) and modest dip in bond yields (the US 10yr rate declined ~2bps) overnight. However, the underlying issues that previously weighed on people’s minds remain, especially the precarious situation in the Middle East and elevated oil prices (Brent crude is now near ~US$104/brl, ~77% above its mid-December low). The Strait of Hormuz remains effectively shut with only a handful of vessels making the crossing. Iran continues to attack neighbouring nations, and from the US side a top counterterrorism official resigned because “Iran posed no imminent threat to our nation” and President Trump sent out an angry social media post raging about the lack of support from NATO partners as well as Japan, Australia and South Korea.

In FX, the USD index drifted a bit lower with EUR (the major USD alternative) edging up (now ~$1.1540) and USD/JPY consolidating (now ~159, upper end of its 1-year range). GBP also nudged up (now ~$1.3357), and although NZD tread water (now ~$0.5858, just below its 1-year average) the AUD rose (now ~$0.7105) after the RBA raised rates by 25bps and kept the door open to more policy tightening down the track (see below).

As discussed, and observed, over recent weeks, the situation in the Middle East remains fluid and a source of market volatility. More twists and turns are likely over the period ahead. Sustained high oil/energy prices are a downside risk for global growth and upside risk for inflation. This is normally a difficult environment that generates safe-haven demand for the USD. Moreover, due to the US’ switch to becoming a ‘net energy exporter’ elevated oil prices have also become USD supportive. Looking ahead, the Bank of Canada (12:45am AEDT) meets tonight and the US Fed decision is tomorrow morning (5am AEDT, press conference 5:30am AEDT). No change in rates by the US Fed is anticipated, but updated economic forecasts will be released. The growth/inflation crosscurrents leave policymakers in a tricky spot. On net, the implication could be that the uncertainty sees the US Fed hold steady for a while until more clarity on underlying trends emerges. In our view, this type of ‘on hold’ message might be a positive for the USD.

Trans-Tasman Zone

Despite the lingering issues in the Middle East and elevated oil prices, market sentiment has relatively improved over the past few days. This, a slightly softer USD, and another RBA rate rise has helped the AUD claw back some lost ground. At ~$0.7105 the AUD is up where it was tracking late last week and a little above its 1-month average. The AUD has also ticked up on the cross-rates with gains of ~0.2-0.5% recorded against EUR, JPY, GBP, NZD, CAD, and CNH the past 24hrs. AUD/EUR (now ~0.6157) is within striking distance of its ~15-month high, AUD/JPY (now ~112.97) is not that far from its multi-decade peak, AUD/GBP (now ~0.5320) is in the region it last traded in in early-2024, and AUD/NZD (now ~1.2129) is at the top of the range occupied the past ~13-years.

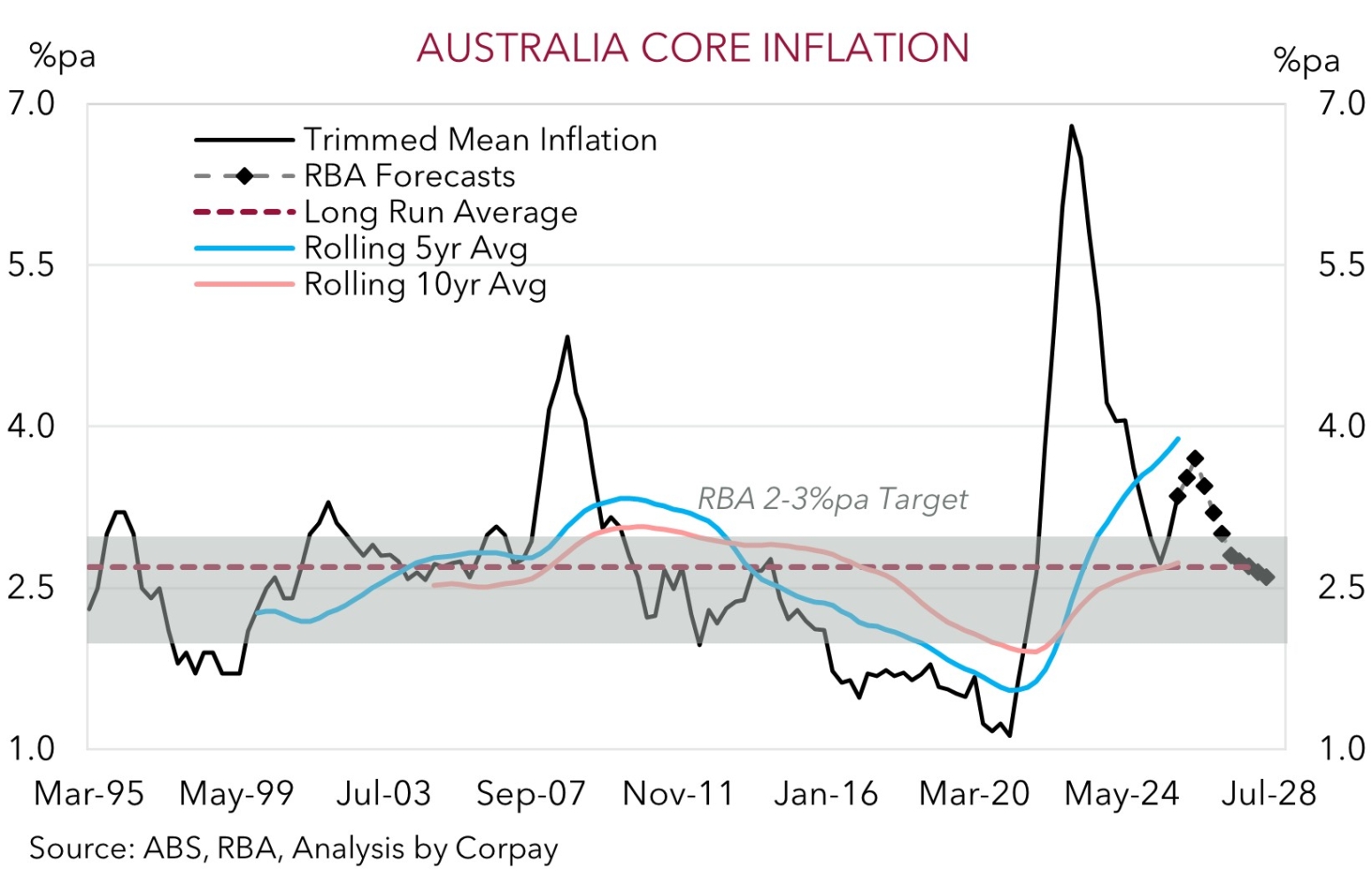

The RBA is taking fewer chances when it comes to its renewed battle against inflation with the latest 25bp hike lifting the cash rate back up to 4.1%, just 25bps off the ‘peak’ reached in the 2023/24. The decision wasn’t unanimous with the Board voting 5-4 in favour of a move. But the dissents related to timing (i.e. waiting until the next meeting) not the direction of rates. According to the RBA “there is a material risk that inflation will remain above target for longer than previously anticipated” due to domestic capacity pressures and oil related Middle East developments. These are ‘hawkish’ concerns that mean the door to another rate rise is open, in our view. Another 25bp hike as soon as the next meeting on 5 May could be on the cards. We think the more ‘restrictive’ policy settings should help cool inflation, but it will come at the cost of slower growth and looser labour market conditions down the line. This is the (unfortunate) price that needs to be paid.

On net, we believe that given how much RBA tightening is still factored into the Australian interest rate curve (markets are discounting another ~43bps of hikes by year-end), the issues in the Middle East (which are set to be a drag on global growth), and with the negative domestic economic consequences of higher mortgage rates and fuel costs set to manifest over coming months, further upside in the AUD could be somewhat limited, and downside risks are lurking. Moreover, the AUD is ~2-3% above our ‘fair value’ estimate, and higher than where various yield/interest rate differentials suggest it should be. Too many positives appear to be baked into the AUD. As a reminder, we believe the higher level of interest rates and wider yield spreads point to a higher average range for the AUD than what we saw the past few years, but not necessarily more AUD appreciation because of the worsening global/domestic growth trajectory. For more see Market Musing: RBA – Inflation battle continues.