After being ‘strategically timid’ during its last tightening cycle the RBA looks to be taking fewer chances when it comes to its renewed battle against inflation with another 25bp rate hike announced today. This follows the rate rise delivered at the last meeting in February and lifts the cash rate back up to 4.1%, just 25bps off the ‘peak’ reached in the 2023/2024 inflation fight (chart 1).

Today’s decision wasn’t unanimous with the RBA Board voting 5-4 in favour of a hike. This was more evenly split than anticipated with markets pricing in a ~70% chance of a move. It was a matter of when, not if, the RBA acted again. Indeed, Governor Bullock confirmed the split and discussion was “centered on timing” not the direction of rates.

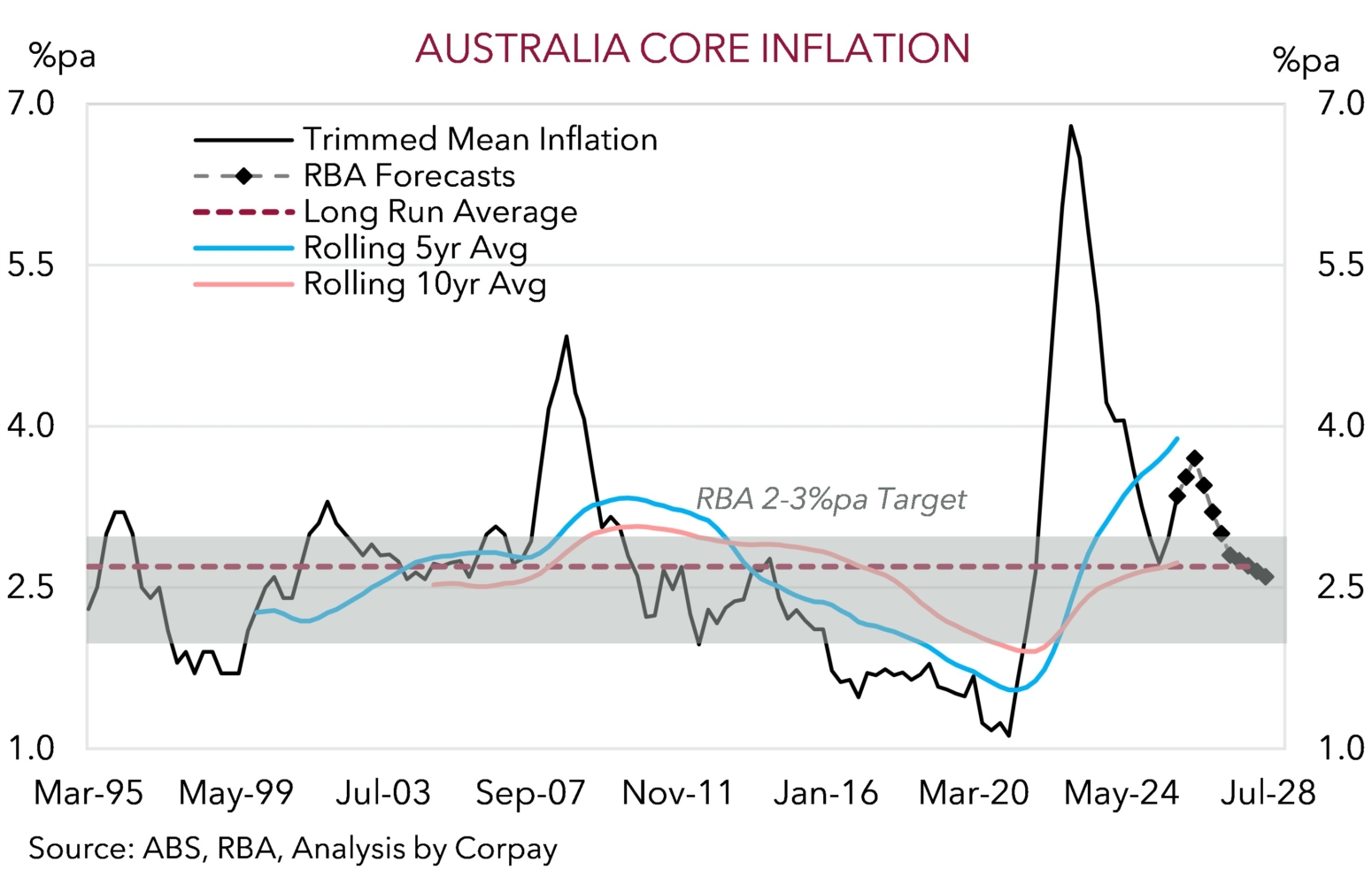

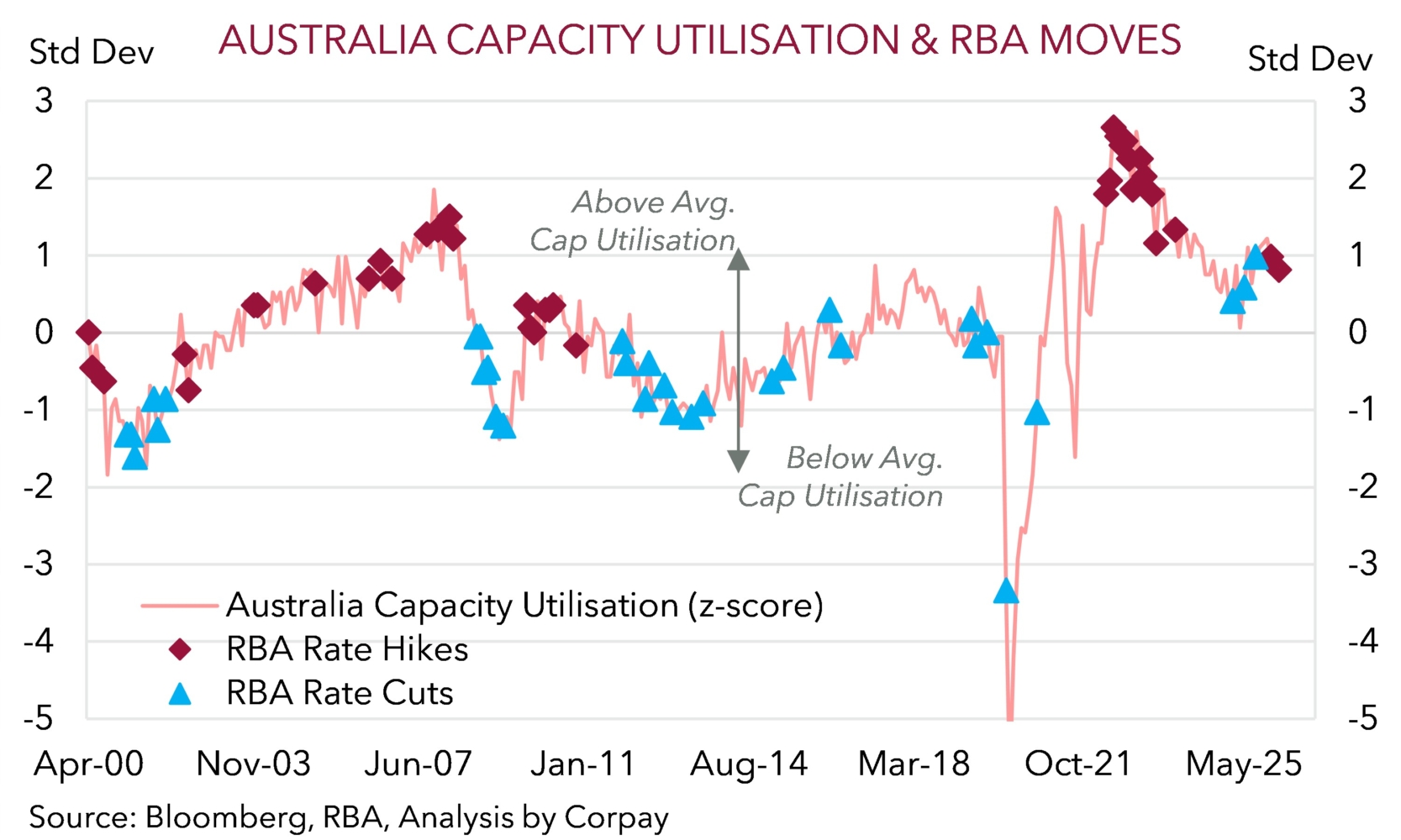

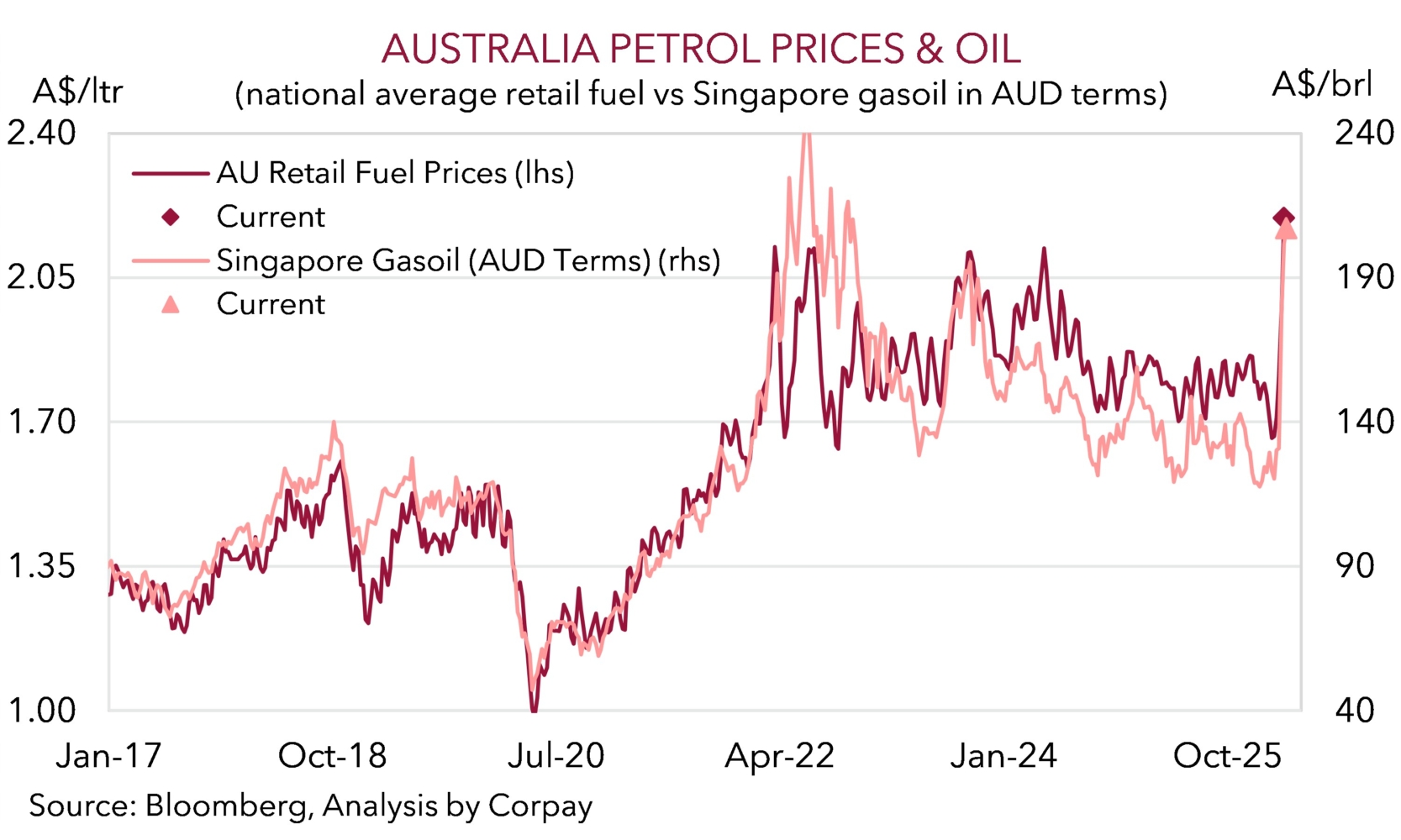

A key question now is whether the RBA’s policy U-turn has further to run? According to the RBA inflation is “too high” and “there is a material risk that inflation will remain above target for longer than previously anticipated” due to domestic capacity pressures stemming from demand outstripping supply and oil related Middle East developments (chart 2). Going forward the Board will be “attentive to the data” and evolving risks. Given the Board also continues to stress it is “focused on its mandate” to deliver prices stability and full-employment, and “will do what it considers necessary to achieve that outcome”, the door to another rate rise remains wide open, in our view.

We think the more ‘restrictive’ policy settings in place should help cool inflation (albeit at the cost of slower economic growth and looser labour market conditions) but a bit more tightening might be needed to definitively get the job done. Another 25bp interest rate hike as soon as the next meeting on 5 May could be on the cards because the Australian economy is operating at a high level (as illustrated by above average capacity utilisation and low unemployment), momentum across the private sector has improved, and inflation (which is already high) will be compounded by the energy/fuel price surge (chart 3 and 4). That said, we also believe markets might have jumped the gun by factoring in more than two more rate rises by December. If realised, this would put the cash rate above the previous ‘peak’, and given the RBA continues to emphasize its strategy of trying to lower inflation while attempting to preserve job market gains remains in place, we aren’t convinced the Board will be more aggressive than it was before.

The AUD (now ~$0.7075) has been whipped around intra-day by push/pull RBA headlines, although we would note the swings haven’t been as large as those brought on by offshore developments over the last little while. On net, we continue to think that given how much RBA tightening is still factored into the Australian interest rate curve, the issues in the Middle East (which are set to be a drag on global growth), and with the negative domestic economic consequences of higher mortgage rates and fuel costs set to manifest over coming months, further upside in the AUD could be somewhat limited, and there are more short-term downside risks. For the Australian economy higher energy prices support the terms of trade and national incomes because of LNG exports. But for Australians already feeling the cost-of-living squeeze it is a negative shock.

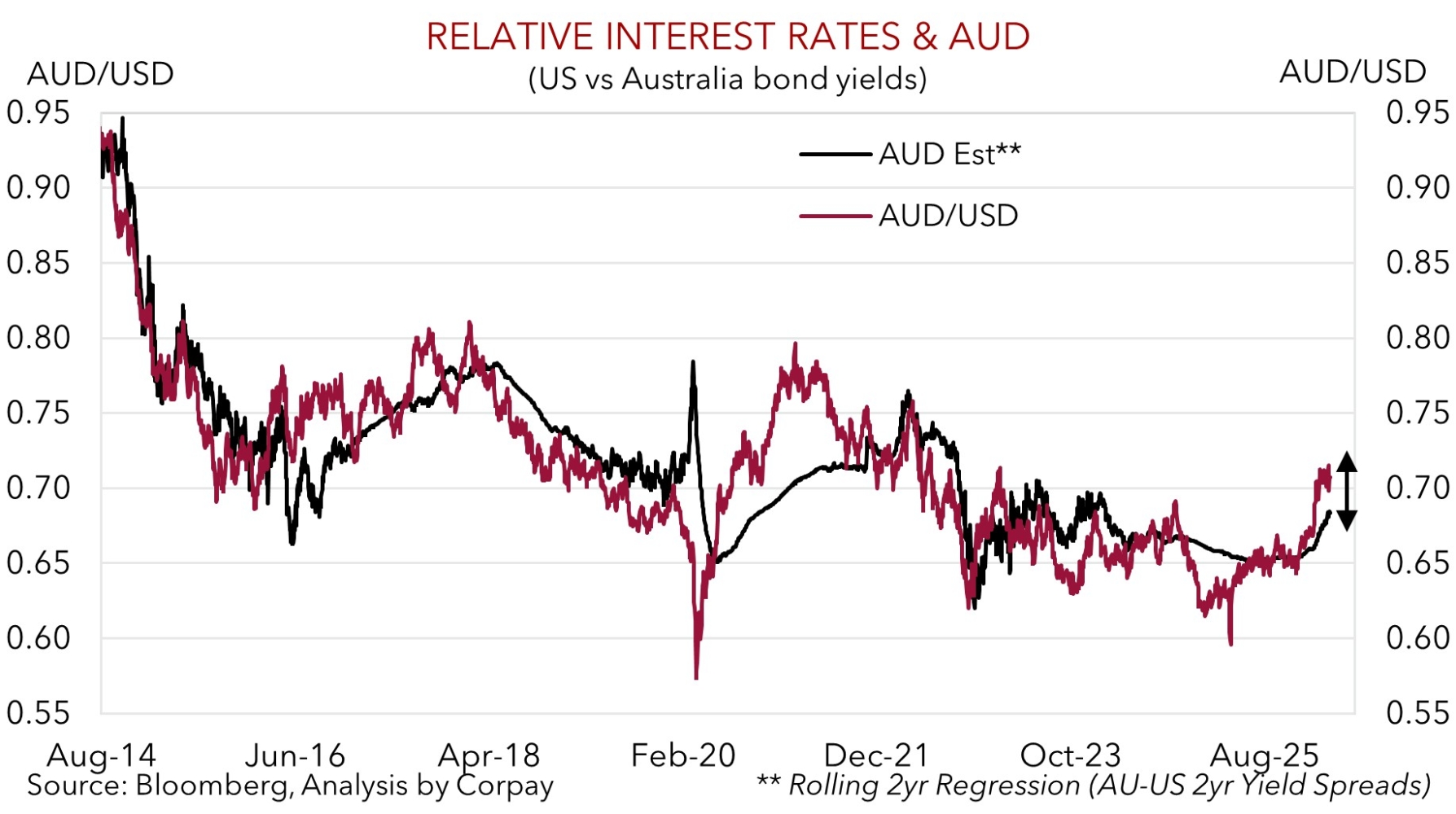

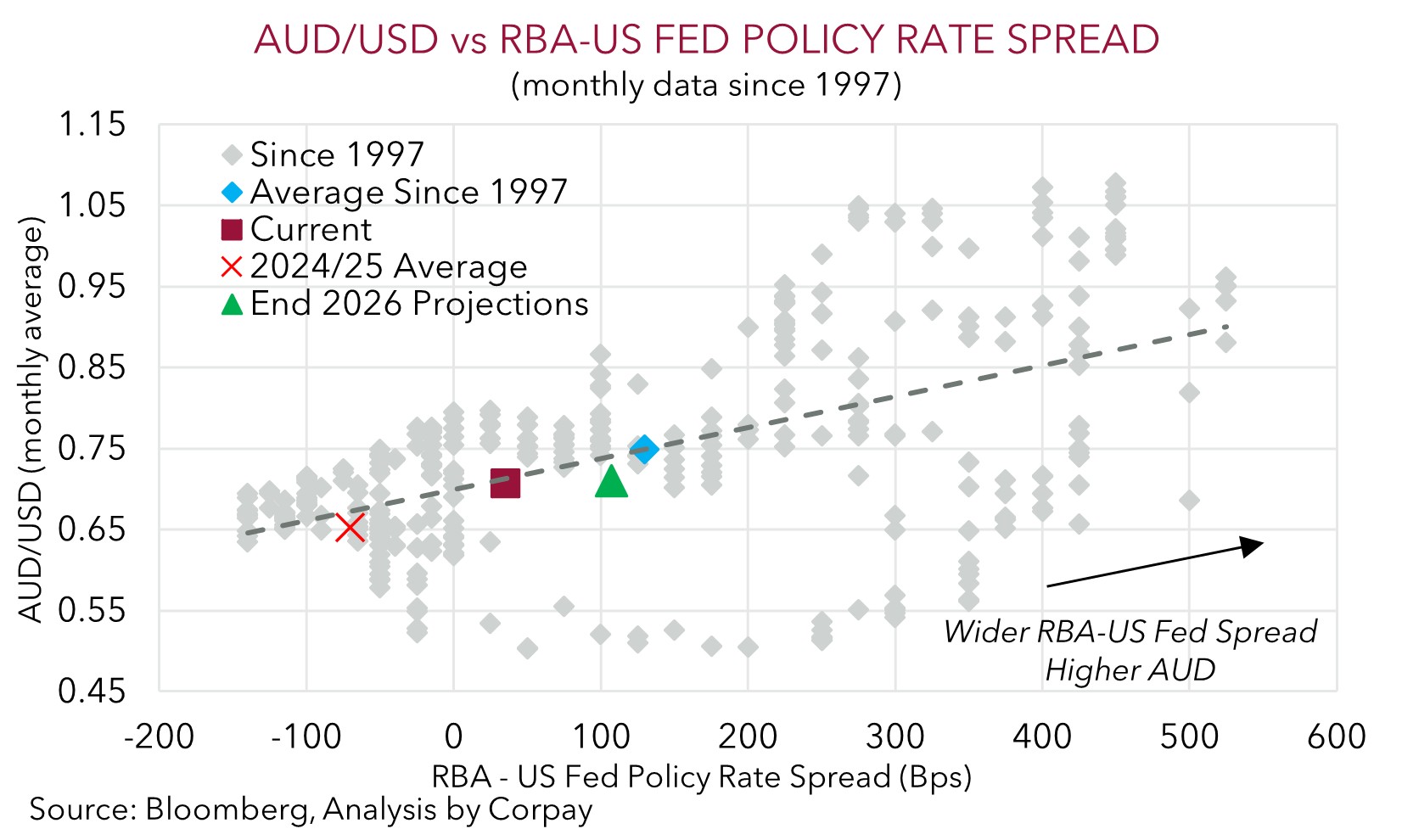

Moreover, the AUD is ~2% above our central ‘fair value’ estimate, and higher than where various yield/interest rate differentials suggest it should be (chart 5). As a reminder, we believe the higher level of interest rates and wider yield spreads point to a higher average range for the AUD than what we saw the past few years, but not necessarily much more AUD appreciation because of the worsening global/domestic growth outlook (chart 6).