• Oil swings. Pull-back in oil prices has supported risk sentiment. Will it last? Situation in Middle East remains fluid. More volatility likely over period ahead.

• RBA Hawks. AUD/USD at top of its range. RBA Dep. Gov ‘hawkish’ yesterday. Will it move next week? More than 2 hikes now priced in by September.

Global Trends

After a torrid end to last week and negative start on Monday sentiment has improved over the past few days. Volatility has continued with the situation in the Middle East still tricky to navigate. However, while there are still underlying issues in place traders (as they typically do) have been hearing what they want to hear, and risk markets have rebounded. Comments yesterday by President Trump indicating the war is “very complete, pretty much”, coupled with reports nations were looking at releasing strategic oil reserves to mitigate supply concerns, and the prospect of tankers being escorted through the Strait of Hormuz helped somewhat sooth investor fears. Though social media posts by US Administration members indicating a tanker had been successfully escorted but which were subsequently deleted did cause a bit of havoc in markets overnight.

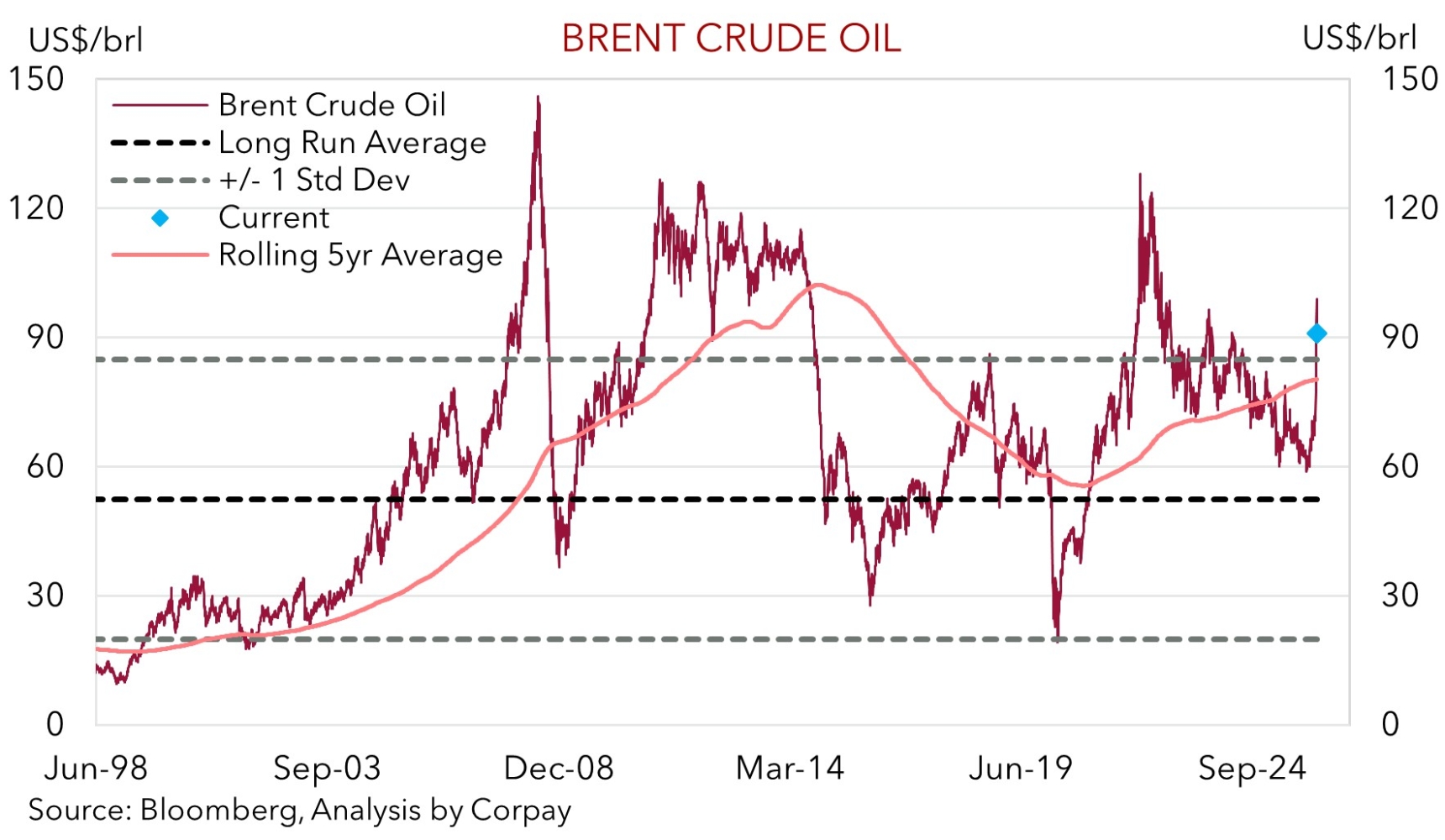

Oil prices have fallen from Monday’s peak (Brent Crude was at one stage near US$120/brl), but they are also well above overnight lows, and on balance look to have settled near ~US$91/brl. As our chart shows, this is an improvement from a few days ago, however oil prices are still elevated from a historical perspective (and ~54% above the mid-December low). The net decline in oil prices since Monday has helped support broader risk sentiment (European equities rose ~1.6-3% overnight and US equities consolidated). US bond yields ticked up (the 10yr rate rose ~6bps), and in FX, inline with its positive correlation to oil, the swings in energy prices have seen the USD whip around the past 24hrs. EUR (the major USD alternative) has nudged back over ~$1.16, USD/JPY (the second most traded pair) is above ~158, and GBP is just under ~$1.3420. NZD has edged up the past few sessions (now ~$0.5929), while improved sentiment and ‘hawkish’ comments from RBA Deputy Governor Hauser that further opened the door to another rate hike next week helped AUD outperform with AUD/USD near the upper end of its range (now ~$0.7120).

As seen in the past few days, the situation in the Middle East remains fluid and oil remains a key driver of broad market volatility. We think it is premature to assume things are coming to an end. There could be more twists and turns, with headline driven volatility set to continue for a while. In addition to Middle East developments, focus tonight will be on the latest US CPI data (11:30pm AEDT). Signs of stickiness in US core inflation, which will be compounded over the next few months by the jump up in oil prices, might act to once again dampen the market mood. This in turn could give the USD renewed support, particularly as the US’ shift to becoming a ‘net energy exporter’ means the higher level of oil prices (and a higher US terms of trade) may keep the USD in a relatively higher range than it was when oil was tracking down around US$60/brl at the end of last year.

Trans-Tasman Zone

The oil pullback led improvement in risk sentiment, combined with an upward repricing in Australian interest rate expectations and relative outperformance on the cross-rates has helped the AUD snap back over the past few sessions (see above). At ~$0.7120 AUD/USD is near the top of the range it has occupied since early-2023, with its overnight intra-session peak also the highest it has traded since mid-2022. The ~2.3% rebound in the AUD from Monday’s low once again highlights how volatile the currency can be. Participants may have forgotten, but since the late-80’s the AUD has, on average, traded in a ~1% daily range. On the cross-rates the AUD has risen by ~0.5-0.9% versus the EUR, JPY, GBP, NZD, CAD, and CNH the past 24hrs. AUD/EUR (now ~0.6132) is near its highest point since December 2024, AUD/GBP (now ~0.5306) is around the top of its ~26-month range, AUD/NZD (now ~1.2008) is at a ~13-year peak, AUD/CNH (now ~4.8976) is tracking close to the upper bound of its ~4-year range, and AUD/JPY (now ~112.52) is at a multi-decade high.

Locally, RBA deputy Governor Hauser spoke yesterday, and he sounded ‘hawkish’ about recent developments. Specifically, he noted inflation was “directionally higher” than the RBA’s February forecast, in part due to the jump in oil which is well above the technical assumption used in the RBA’s modelling, and upward revisions suggest growth was stronger. He also indicated he thinks “there will be a very genuine debate” about another rate hike at next Tuesday’s meeting. Recall, Governor Bullock has already said that the meeting is “live”, but these latest comments have added fuel to the fire, particularly as uncomfortable inflation trends have been made worse by the spike in energy prices. Markets are now pricing in a ~57% chance of a 25bp rate rise on Tuesday (up from ~25% chance earlier in the week), with a bit more than two hikes now discounted from September.

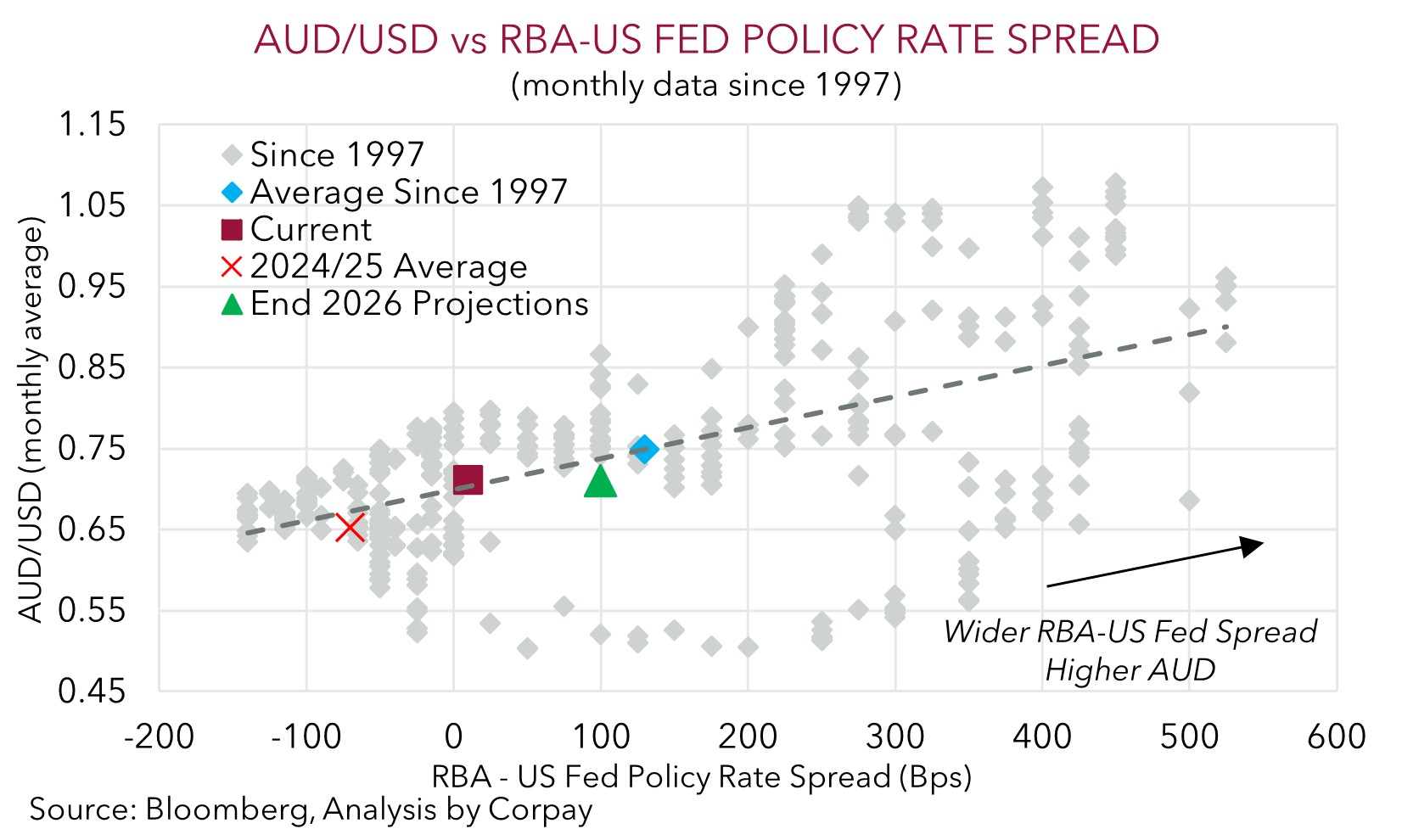

It remains a matter of when, not if, the RBA raises interest rates again. The decision to not raise rates as far as other central banks in order to preserve as many of the COVID-era job gains as possible clearly failed to break inflation, and last year’s rate cuts came through too quickly. A move next week is possible, though we think the RBA Board (which has tended to be more conservative this cycle and backward data looking) may want to wait on the next full quarterly CPI (due late-April) before acting again in early-May. Nevertheless, in terms of the AUD, given what is now factored into the interest rate curve, the ongoing issues in the Middle East, and with the negative domestic economic consequences of higher mortgage rates set to manifest down the track, we believe further sustained upside may be limited. Indeed, the AUD is tracking above our ‘fair value’ estimates and is broadly inline with where the RBA-US Fed policy outlook suggests it should be (see chart below).