• Oil jolt. Another jump in oil prices weighed on sentiment. Equities lower, USD firmer. NZD weaker. AUD underperforms after its strong run.

• Twists & turns. Markets pricing a supply risk premium in oil. More volatility likely. RBA next week with chances of a rate hike now sitting at ~70%.

Global Trends

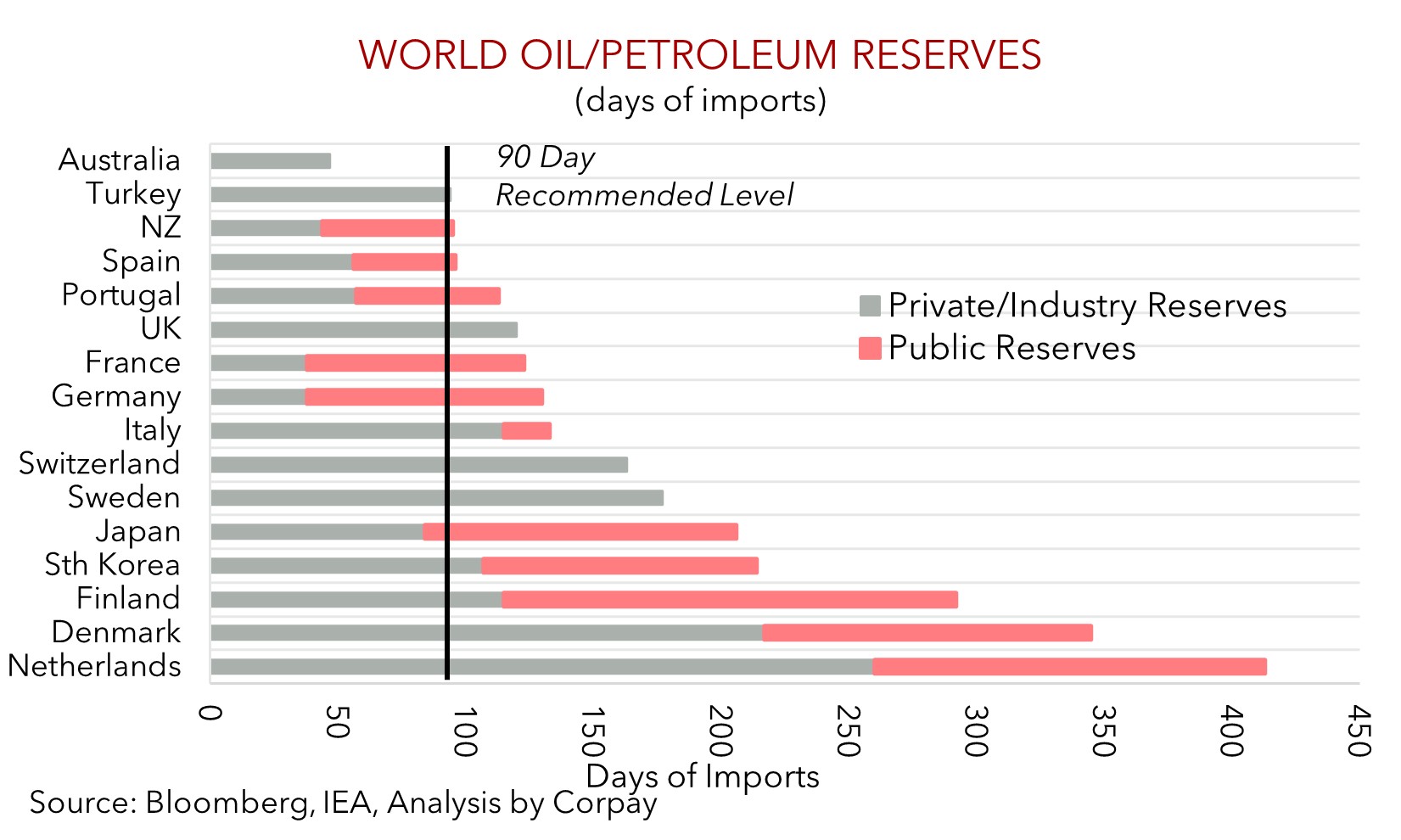

Middle East developments continue to be in the driver’s seat. Sentiment remained negative overnight with the jump in oil prices dampening the market mood. Brent crude oil is back above ~US$101/brl, a ~8.5% lift from where it was tracking yesterday, and ~74% above levels it was at in mid-December. As our chart shows, markets continue to factor in a hefty supply risk premium with the current price of oil well above where fundamentals suggest it should be. Prospects for a rapid restoration of oil flows through the Strait of Hormuz have faded. President Trump said preventing Iran from acquiring nuclear weapons was a higher priority than oil prices. At the same time, Iran’s new leader vowed to keep the Strait shut (several vessels were reportedly attacked over the past 24hrs), and US naval escorts look like they might not be in place for weeks. Indeed, even the announced record release of global oil reserves (~400mn barrels, which includes ~172mn from the US’ strategic stockpile) failed to appease wary markets. This is somewhat understandable as the headline grabbing figures may not hit the ground for a while. The US Energy Secretary said the release of its reserves will take “about 120 days to fully deliver”.

Across other markets, European and US equities fell with the S&P500 shedding ~1.5%. The inflationary implications of a sustained elevated oil price are also underpinning a move up in bond yields. US bond yields rose ~3-9bps across the curve with the 2yr rate (now ~3.74%) at its highest since last August. Notably, markets are now only fully discounting another US Fed rate cut by September 2027. At the start of this month there was a US Fed rate reduction factored in by July 2026. In FX, the USD strengthened with EUR around the bottom of its multi-month range (now ~$1.1512) and USD/JPY (now ~159.34) approaching its cyclical peak. Growth linked currencies like the NZD (now ~$0.5853) and AUD (now ~$0.7078) underperformed overnight.

As outlined over the past week, the situation in the Middle East is fluid. Based on the rhetoric of the two sides it is premature to assume things are nearing an end. There may be more twists and turns with market volatility set to continue for a while. All up, we continue to believe safe-haven demand, combined with higher oil prices, can be USD supportive. These dynamics should keep the USD in a higher range than it was in when oil was near US$60/brl at the end of 2025. As mentioned before, the US’ shift to a ‘net energy exporter’ a few years ago has resulted in the USD becoming positively correlated to oil prices.

Trans-Tasman Zone

The bout of risk aversion stemming from the latest jump in oil prices has supported the USD (see above). This, and the negative sentiment has exerted downward pressure on the NZD (now ~$0.5853) and seen the AUD underperform after its recent strong run (now ~$0.7078). On the cross-rates the backdrop has seen the AUD weaken by ~0.6-1% versus the EUR, JPY, GBP, CAD, and CNH, while AUD/NZD consolidated around the top of its ~13-year range. That said, if you take a step back, crosses like AUD/EUR (now ~0.6148), AUD/JPY (now ~112.78), AUD/GBP (now ~0.5306) and AUD/CNH (now ~4.87) are still hovering near the upper end of their respective ranges.

Looking ahead, in Australia focus next week will be on the RBA meeting (Tuesday). Following a run of solid data, ‘hawkish’ commentary from RBA officials, and the upside risks to inflation generated by the oil price spike, chances of another rate hike being announced are sitting at ~70%. It remains a matter of when, not if, the RBA acts again, with more than a fully rate rise baked in by May and ~71bps worth of tightening discounted by year-end. AUD volatility around the RBA meeting looks likely given the elevated level of expectations.

In markets, outcomes versus expectations are what matter. With this in mind, we think another RBA rate rise next week might not be the catalyst for that much more AUD strength. There is a lot of tightening now priced into the Australian interest rate curve, the issues in the Middle East look set to continue for some time, and the negative domestic economic consequences of higher mortgage rates and fuel costs, which are set to manifest over coming months, don’t appear to be factored in. For the Australian economy higher energy prices support the terms of trade and national incomes because of LNG exports. But for Australians already feeling the cost-of-living squeeze it is more of a negative shock. As the slowdown in activity (which is needed to lower inflation) takes hold down the track, the AUD could start to give back ground, in our opinion. Moreover, the AUD already looks ‘stretched’ with it ~2% above our ‘fair value’ estimates and above where interest rate differentials suggest it should be. The higher level of interest rates and wider yield spreads point to a higher average range for the AUD than what we saw the past few years, but not necessarily further AUD upside.