• Macro worries. Growth/inflation concerns due to the jump in oil were compounded by a weak US jobs report. AUD remains on the backfoot.

• Oil risks. Production cuts across Middle East creating supply risks. Oil at multi-year high. USD has become positively correlated to oil the past few years.

Global Trends

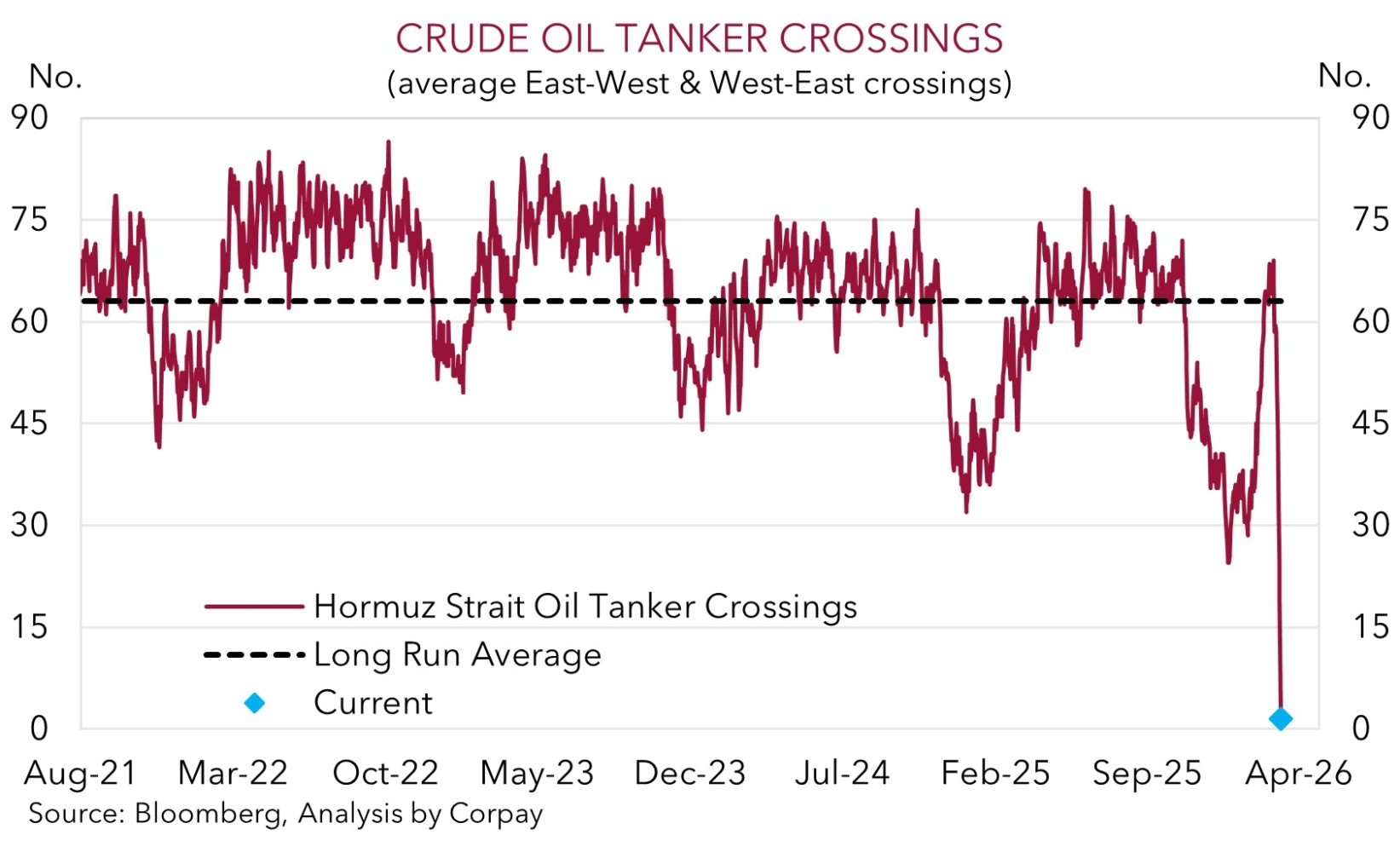

It was a negative end to a rather torrid week for markets on Friday. Developments in the Middle East and oil prices remain front of mind, while a weaker than anticipated US jobs report and tepid retail sales compounded investor nervousness. Oil prices jumped again with Brent Crude tracking near ~US$94/brl. This is a high since Q3 2023 and ~58% above the mid-December low. As mentioned before, higher oil prices are generating fears of a simultaneous growth slowdown (higher fuel prices act like a tax) and inflation jolt. Worries about ‘stagflation’ aren’t typically a great environment for risk assets. As our chart below shows, on our figuring, traders are (finally) factoring in a supply premium in oil. Key Middle East oil producers such as the UAE, Kuwait and Iraq are slowing production. This is because storage capacity is running out due to the Strait of Hormuz, the vital shipping lane in the region, effectively being shut. As the second chart illustrates, container crossings have dropped to near zero. Given the regional situation shows no real signs of improvement, oil prices may move even higher in the near-term.

Data wise, topline US retail sales declined 0.2% in January, in part due to severe winter weather which disrupted spending in areas like restaurants and vehicles. With respect to the US jobs market non-farm payrolls fell 92,000 in February and the unemployment rate nudged up to 4.4%. Some temporary factors like a healthcare workers strike and the winter weather may have weighed on jobs growth in some sectors in February, however the underlying trend has been subpar for a while indicating there are bigger forces at play.

In terms of markets, US/European equities declined on Friday with the S&P500 shedding ~1.3% (or ~2% over the week, its largest weekly fall since October). Bond yields consolidated as push-pull growth/inflation forces washed through (the US 10yr rate is tracking near ~4.14%, the middle of its year-to-date range). Markets are only fully discounting another US Fed rate cut by September despite the negative labour market surprise. In FX, the USD index drifted lower, though this reflects strength in a few currencies like CAD and CHF. EUR (the major USD alternative) has dipped towards the bottom of its multi-month range (now ~$1.1548) and USD/JPY (the second most traded pair) has edged up (now ~158.10). Cyclical currencies such as NZD (now ~$0.5866) and AUD (now ~$0.6984) underperformed.

This week, in addition to Middle East developments, attention will also be paid to the latest US CPI print (Weds night AEDT). Signs of stickiness in core inflation might act to further dampen the market mood. On net, as outlined previously, given the US’ shift to becoming a ‘net energy exporter’, higher oil prices are positive for the US’ terms of trade and are USD supportive (the USD now has a positive correlation to oil prices). In our opinion, this, coupled with safe-haven demand because of geopolitical worries, can see the USD extend its rebound over the near-term.

Trans-Tasman Zone

The direct and indirect consequences of the conflict in the Middle East, combined with the upside global inflation/downside global growth risks generated by the sharp jump up in oil prices has further dampened sentiment and weighed on cyclical currencies like the NZD (now ~$0.5866) and AUD (now ~$0.6984). The AUD also lost ground against a few other major currencies like GBP (-0.3%), CAD (-0.9%), and CNH (-0.5%), while it has ticked up versus the EUR (now ~0.6048) and NZD (now ~1.1905) in part due to concerns about momentum in the production heavy Eurozone economy stemming from the energy price rise and NZ’s status as a ‘net energy importer’.

This week in Australia it is a quiet data calendar with only consumer confidence and business conditions due (both Tues). The next major event in Australia is the 17 March RBA meeting. It is a similar story in NZ with Q4 GDP (19 March) the next top tier release. While the upcoming March meeting is deemed to be “live” for a policy change by RBA officials (markets are pricing in a ~25% chance of another rate hike) we think the more likely outcome is for the RBA to hold steady until the 5 May meeting as it gathers information on labour market/inflation trends and sees how the Middle East conflict is playing out.

As discussed above and over the past week or so, the situation in Middle East is constantly evolving and more bouts of market/AUD volatility should be anticipated over the period ahead. While the outlook for further RBA rate rises and a shift up in the level of Australian interest rates should act as an AUD downside support, the negative external risk environment is more than an offsetting factor. Added to that, with the AUD still tracking above our model estimates (we see ‘fair value’ closer to ~$0.6930), the negative growth/inflation implications for parts of Asia (and the global economy) created by higher energy prices, and potential for the USD to extend its recovery (due to safe-haven demand and positive correlation to oil prices), we continue to believe there are more downside risks for the AUD over the short-term.