The US job creation engine decelerated sharply last month, partially reversing market bets on a more hawkish policy stance from the Federal Reserve this year. According to data just released by the Bureau of Labor Statistics, 92,000 jobs were lost in February—representing a major downside surprise relative to the 55,000-consensus forecast—while the previous two months were revised down by a total 69,000 positions, bringing the three-month average pace of job creation to 6,000, well below the 73,000 recorded ahead of the update. The unemployment rate ticked up to 4.4 percent from 4.3 percent in January, missing market expectations for a flat print. Average hourly earnings climbed 0.4 percent month-over-month, maintaining the pace set in the prior month, rising 3.8 percent year-over-year.

Colder-than-typical weather—paired with strike activity in the healthcare sector—appears to have played a role, but weakness is evident throughout the report, giving greater credence to the concerns aired by Governor Christopher Waller in recent speeches, and suggesting that other officials may join him in worrying about a non-linear deterioration in US labour markets.

American consumers spent less in January, but the decline was slightly smaller than markets had anticipated, pointing to a degree of resilience in the household sector. According to figures published by the Census Bureau this morning, total receipts at retail stores, online sellers and restaurants fell -0.2 percent on a month-over-month basis, slightly overshooting market forecasts for an -0.3-percent contraction. So-called “control group” retail sales—with gasoline, cars, food services, and building materials excluded—rose 0.3 percent, matching consensus estimates.

Treasury yields are down sharply across the front of the curve as traders bet the Federal Reserve could resume rate cuts sooner than previously anticipated, equity futures are edging lower, and the dollar is slipping against its major rivals, even as ongoing safe-haven flows provide a bid.

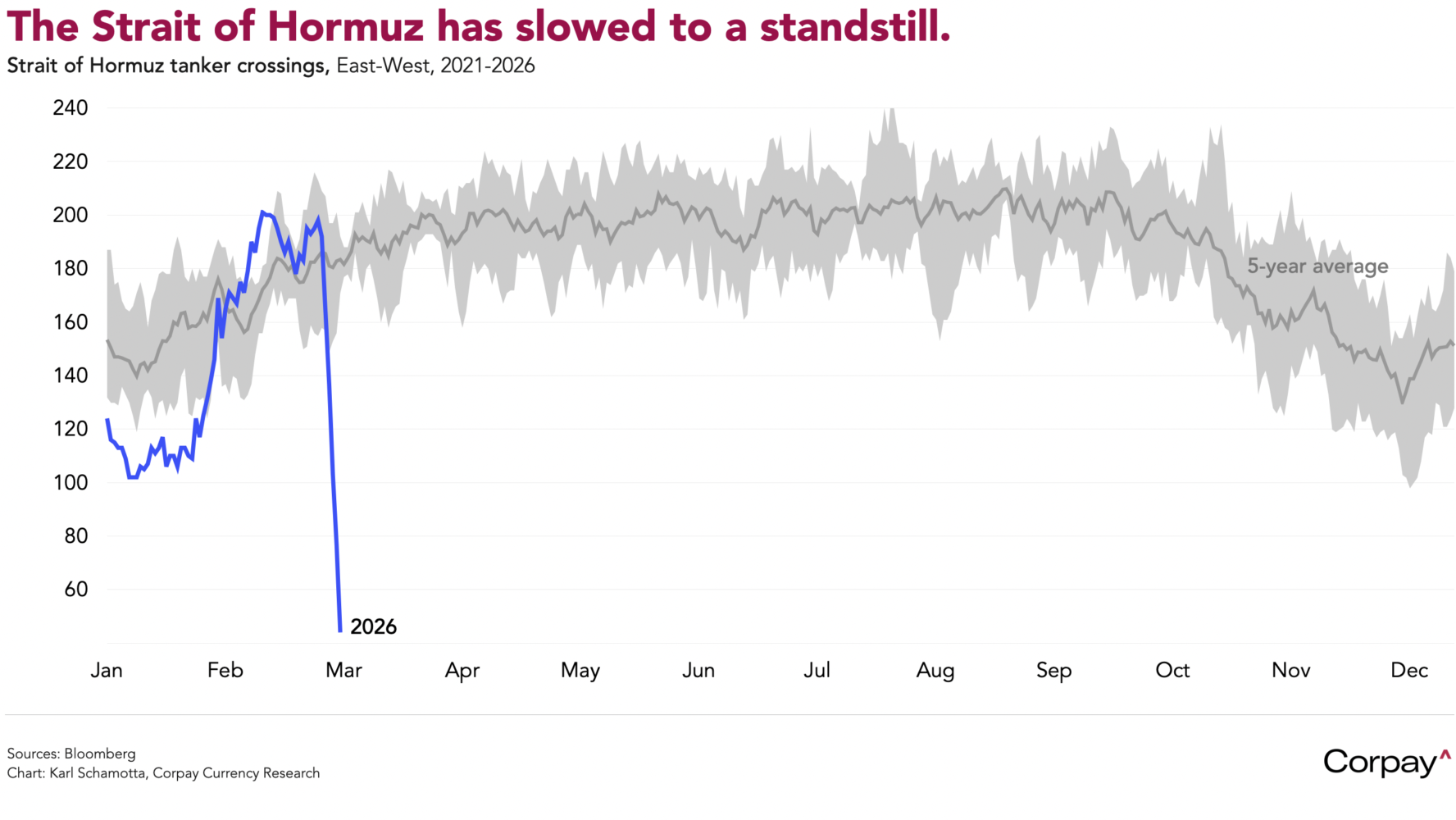

Crude benchmarks are marching higher as reports of a new attack on a tanker in the Persian Gulf cross the wires, and after Qatari energy minister Saad al-Kaabi told the Financial Times that the war in the Middle East could force the region’s energy exporters to stop production in the coming weeks, driving global prices above $150 a barrel. Brent is exchanging hands for nearly $89, while West Texas Intermediate is going for $85, up almost 28 percent on the month after a US-Israeli attack on Tehran followed by Iranian retaliatory strikes brought shipping through the Strait of Hormuz to a virtual standstill. The euro, pound and yen are struggling to make headway amid an ongoing depreciation in energy-importer currencies, while the Canadian dollar and Norwegian krone—the clearest oil proxies among the advanced-economy units—advance against the greenback.

Markets will, more likely than not, get sideswiped by geopolitical headlines in the interim, but next week’s US economic calendar is heavily inflation-oriented, and could refocus investor attention on the extent to which price pressures are intensifying and complicating the Federal Reserve’s policy trajectory. The February consumer price index report will land on Wednesday, followed by the central bank’s preferred inflation measure—January’s core personal consumption expenditures index—on Friday, giving markets an opportunity to recalibrate expectations for rate cuts this year. As we go to print, traders in futures markets are positioned for 45 basis points in easing by December, down from 60 basis points ahead of the outbreak of war in the Middle East.

Bottom line: The Fed’s policy trajectory just got a lot more complicated, and volatility is likely to remain elevated in the days ahead as investors brace for the implications that a stagflationary shock might have on the US and global economies.