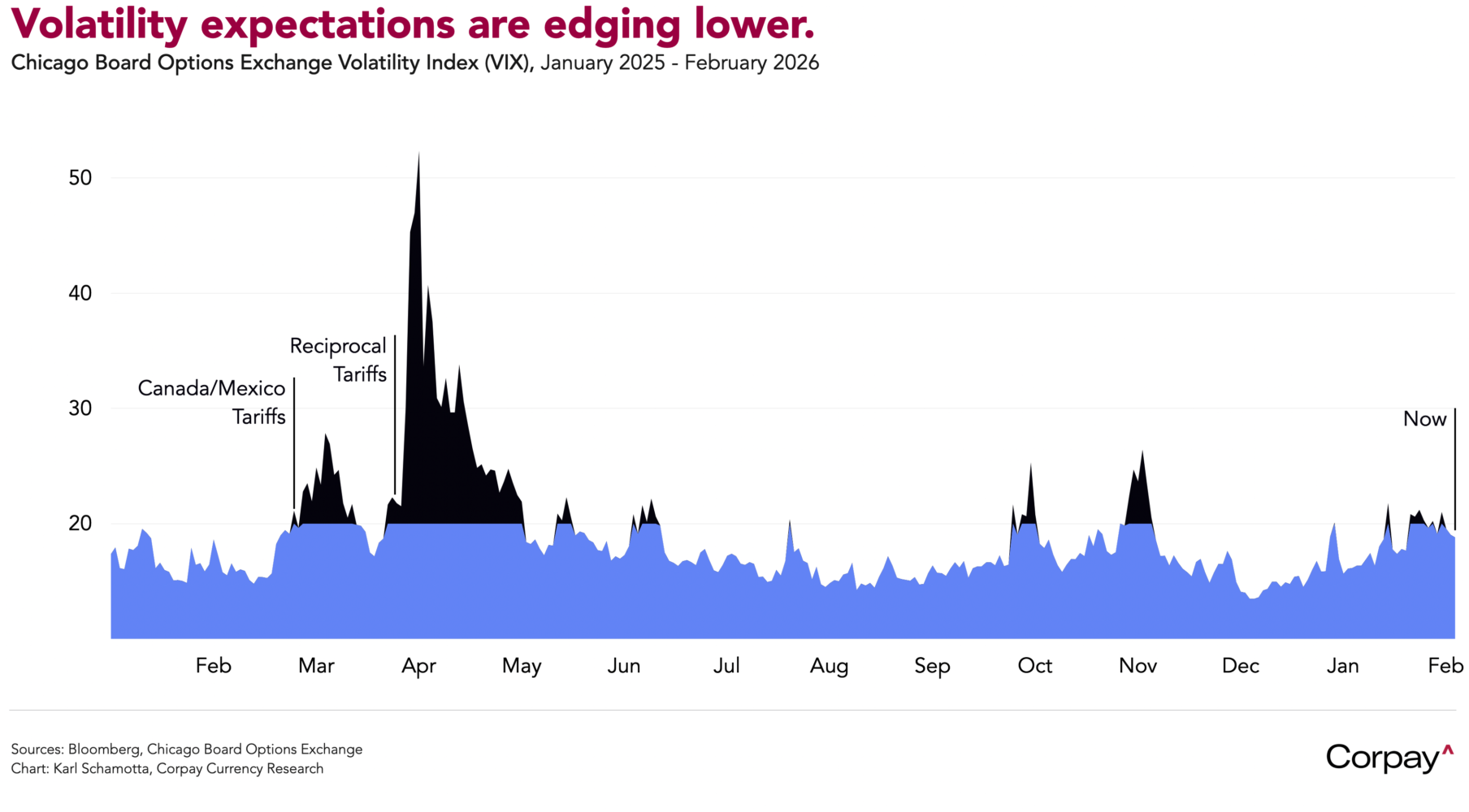

Financial markets are becalmed after US president Donald Trump stuck to the script in his State of the Union address last night, avoiding any major policy announcements and striking a more measured tone on Iran than some investors had feared. The dollar is almost unchanged relative to the afternoon fix, benchmark Treasury yields are edging higher, and equity markets look set to extend yesterday’s recovery into a second session. Measures of implied volatility are tracking lower, with the VIX index—Wall Street’s “fear gauge”—falling back below the 20 threshold that typically signals a sense of alarm among market participants.

The president gave no indication he was prepared to moderate his stance on trade. Trump described last week’s Supreme Court decision to strike down his tariff regime as “disappointing” and vowed to erect a new, more “complex” framework without recourse to Congress. He has since imposed a blanket 10 percent tariff by executive order and threatened to raise it to 15 percent. “Countries that were ripping us off for decades are now paying us hundreds of billions of dollars,” he said. “I believe the tariffs paid for by foreign countries will, like in the past, substantially replace the modern-day system of income tax”.

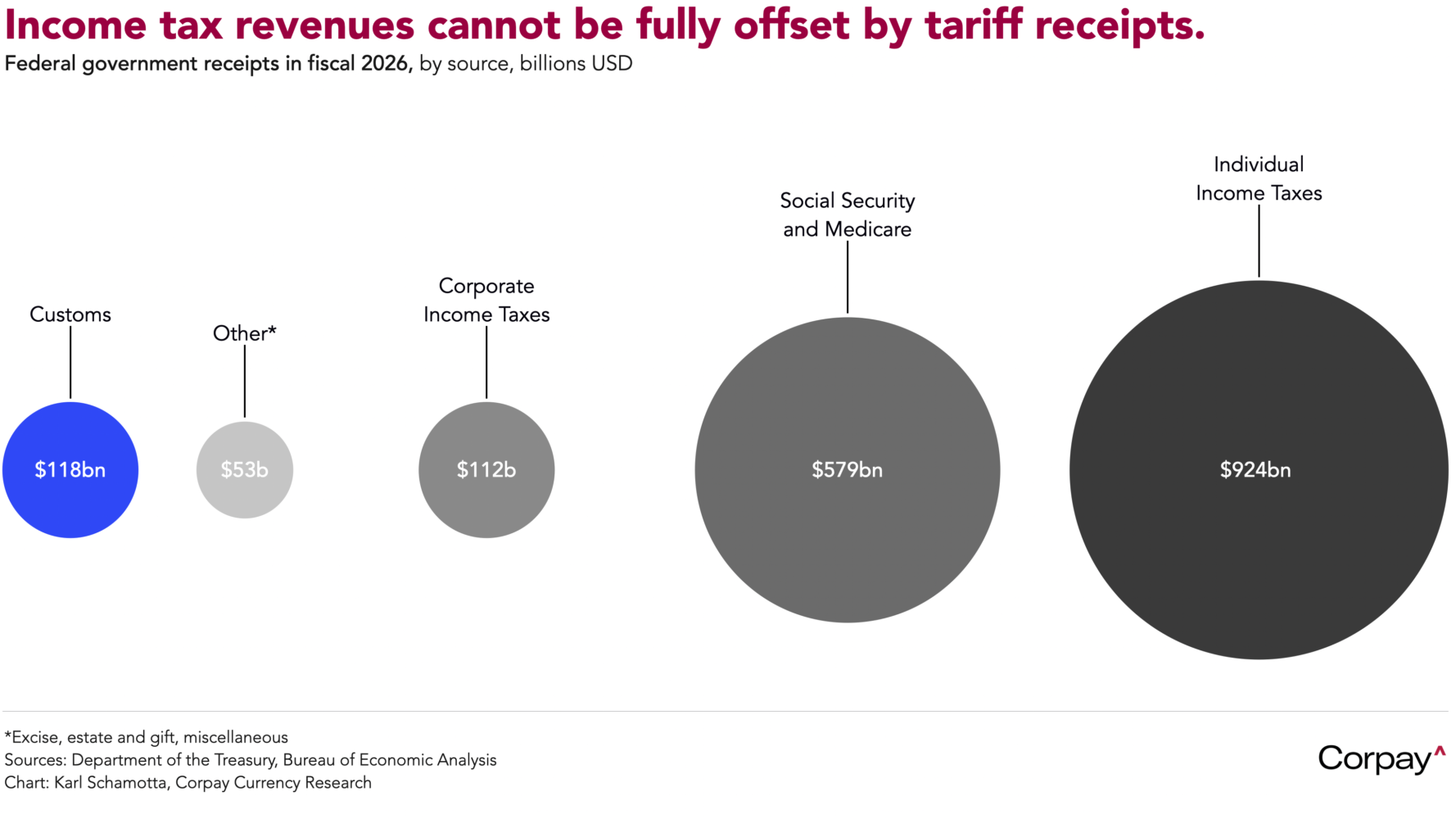

These claims are not supported by the arithmetic. Studies spanning the political spectrum have found that US businesses bear roughly 95 percent of tariff costs, while total goods imports of some $3.4tn are dwarfed by the approximately $15tn in household income on which the federal tax system depends*, making a wholesale substitution of one for the other a fiscal impossibility. Prior to last week’s rollback, tariffs made up 6.6 percent of overall revenues in fiscal 2026, while income taxes accounted for 52 percent and Social Security and Medicare taxes added another 32 percent.

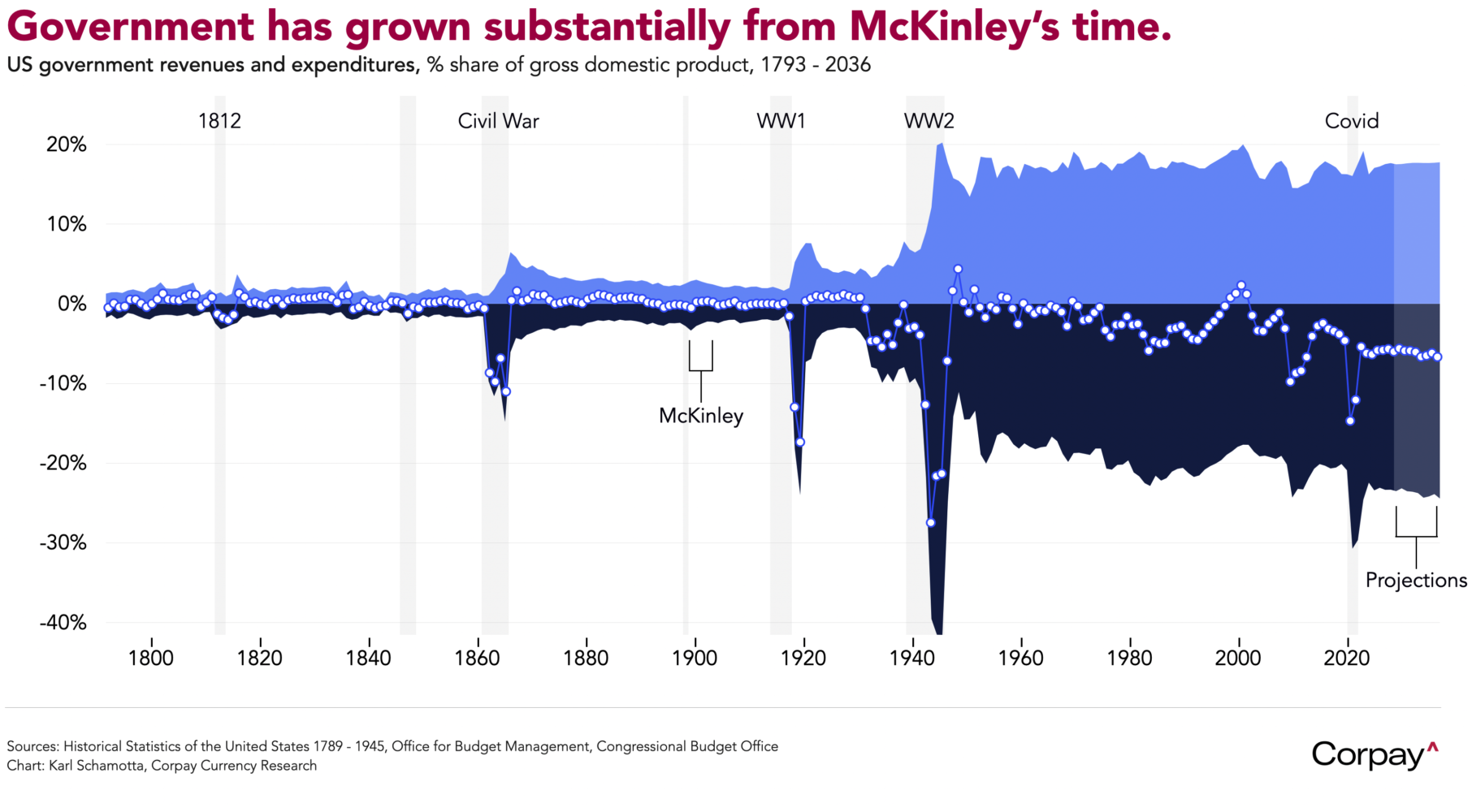

The role of government in the American economy has expanded vastly since the days of president McKinley, to which Trump often harks, and its obligations have grown faster still. Under successive Democratic and Republican leaders, spending on defence, Medicare and Medicaid and other programmes has marched steadily higher, while revenues have lagged, forcing the Treasury to borrow more and raising interest costs over time. Tariffs have, unfortunately, not changed that calculus.

The Japanese yen is down sharply after Sanae Takaichi’s government nominated a pair of dovish academics to the Bank of Japan board, lowering monetary tightening expectations and driving long-term yields higher. The two long-time “reflationists”—Aoyama Gakuin University professor Ayano Sato and Chuo University professor Toichiro Asada—are expected to play a modest role in slowing the central bank’s hiking cycle, given that they will swap seats with two existing doves. But the news comes after the prime minister reported asked governor Ueda to move “cautiously” in normalising monetary policy, and on the heels of a Nikkei article suggesting that US treasury secretary Scott Bessent acted unilaterally in instigating last month’s “rate checks”—implying a lack of concern among Japanese policymakers over the yen’s decline.

Today’s agenda is bereft of important data releases, but Nvidia’s earnings report after the bell looms as a potential volatility catalyst. Most observers expect another quarter of strong results, yet the world’s most valuable company has struggled to reach new highs in recent months as investors have grown less willing to underwrite spectacular levels of capital expenditure among the artificial intelligence hyperscalers, and have begun rotating into sectors with more defensive characteristics. Any evidence of a deceleration in the technology supercycle could deliver a serious blow to global risk appetite, hitting currencies such as the Australian, New Zealand, and Canadian dollars, but could also redound on the United States itself, which has attracted the bulk of global capital flows in recent years.

*Tariff rates high enough to close the gap would dramatically reduce the very trade they aim to tax, shrinking the revenue base in a self-defeating spiral.