There was lots of drama over the weekend. Sinners. One Battle After Another. A Shakespearean tragedy. The Secret Agent. Mr Nobody Against Putin. And that was just the Middle East — the Oscars were on too.

Markets are reversing direction and turning cautiously optimistic after several oil tankers navigated the Strait of Hormuz over the weekend, easing fears of a prolonged disruption to crude flows in the wake of US strikes on Kharg Island. Ships registered to India and Pakistan were granted safe passage, joining Chinese and Iranian vessels already making the transit. Global crude benchmarks are surrendering some of their weekend gains, with West Texas Intermediate trading just below $95 a barrel and Brent at $102. Equity futures point to a modest gain at the open, and the dollar is giving back its recent advance against a basket of major counterparts.

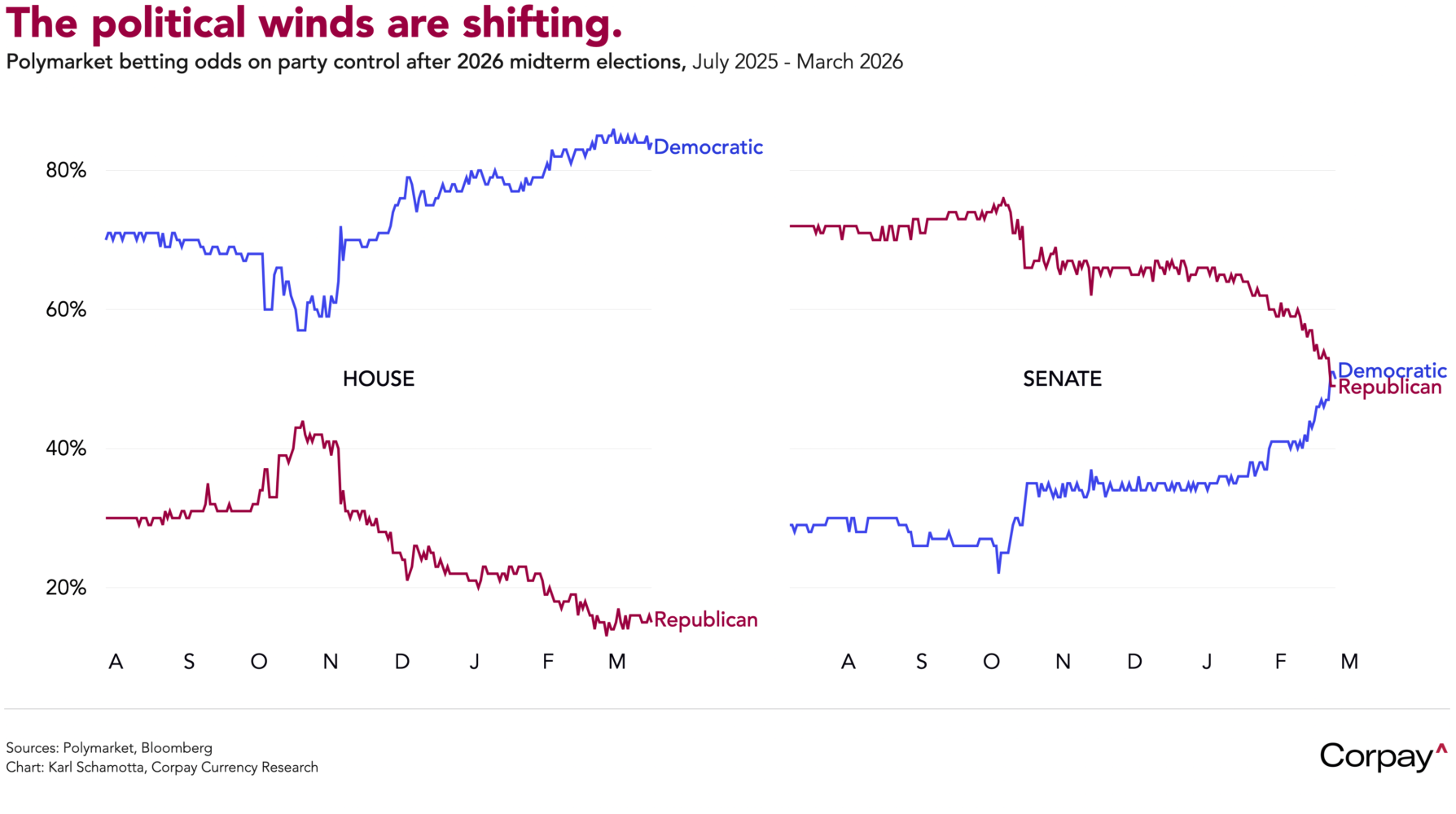

Investors are growing increasingly confident that the Trump administration is looking for an exit—and a way to declare victory. Allies and domestic politics have turned decisively against the conflict. Despite weekend threats, Japan, Germany, and most Nato allies have refused to join a naval flotilla to reopen the Strait, favouring diplomatic channels instead. At home, the war has failed to produce the rally-round-the-flag effect seen in previous conflicts and is deeply unpopular, widely viewed as worsening the affordability crisis facing American households. Prediction markets now point to Democrats taking both the House and the Senate in November, raising the prospect of impeachment proceedings and compounding the political pressure on the president to dial the conflict down.

An optical breakthrough could come at any time, meaning that changes in the dollar’s risk premium and safe-haven bid will remain the dominant forces in foreign exchange this week, but six major central banks will deliver decisions in what amounts to the first monetary policy response to the energy price shock unleashed by the war:

Later today, the Reserve Bank of Australia is likely to hike rates, fully reversing last year’s short and shallow easing cycle. With a domestic inflation problem predating the oil shock, a tight labour market, and private demand growth that keeps surprising to the upside, the RBA is the only major central bank actively tightening, which should attract yield-seeking flows to the Australian dollar, though the currency’s high beta to global growth sentiment and its exposure to Asian energy importers create a natural drag.

Canadian inflation pressures eased more than expected in February, giving the Bank of Canada room to remain on the sidelines at Wednesday’s decision. Statistics Canada data showed the headline consumer price index rising 1.8 percent year on year, down sharply from 2.3 percent in January as tax-related base effects improved, while the month-on-month increase of 0.5 percent undershot forecasts of 0.7 percent. Core inflation — measured as the average of the Bank of Canada’s preferred trim and median gauges — fell to 2.3 percent from 2.5 percent. The figures follow Friday’s deeply negative employment report, which showed the economy shedding 84,000 jobs in February after a 25,000 loss the month before, underscoring the degree of slack still present in the Canadian economy.

Tiff Macklem & Co. are overwhelmingly likely to stay on hold as they face a textbook case of opposing economic shocks: rising energy prices that flatter Canada’s terms of trade while slumping home values and trade uncertainty weigh on domestic demand. Policymakers will undoubtedly acknowledge the possibility that growth rebounds and price pressures intensify once again, but we think their language will remain focused on downside risks, and we suspect that current swap market pricing—for one hike by year-end—could prove vulnerable to downward revision. Although the Canadian dollar is dusting off its petro-currency credentials as crude prices rise, safe-haven demand for the greenback, persistent tariff uncertainty, deep economic slack, and a reticent Bank of Canada should keep gains capped for now.

The Federal Open Market Committee is universally expected to leave policy settings unchanged later on Wednesday, but the Summary of Economic Projections could generate some market turbulence. Two of twelve voting members dissented in favour of a cut in January, but growth numbers have been revised down and the labour market has since softened further, while the war has introduced significant upside price risks, putting the central bank between a rock and a hard place. The update—colloquially known as the “dot plot”—may exhibit stagflationary characteristics, with the median policymaker expecting weaker growth, more unemployment, and higher inflation this year, even as the number of rate cuts remains unchanged at just one.

The Bank of England is expected to hold rates steady on Thursday, capping a sharp repricing since the outbreak of hostilities. Just two weeks ago, swap markets were assigning an 80 percent probability to a March cut and pricing in 50 basis points of easing this year. They now imply 15 basis points of tightening. Britain is acutely exposed: it imports roughly 40 percent of its oil and almost 60 percent of its natural gas, and inflation could rise markedly in the coming months if prices remain elevated. With no new forecasts due at this meeting, Monetary Policy Committee members may instead strip hints of an easing bias from the official statement. The 2022 playbook does not map directly, however: corporate pricing power has diminished, the labour market is considerably weaker, and the risk of second-round wage effects is much lower. The bar for actual rate increases remains high, and—failing a broader reversal in the dollar—the pound looks vulnerable to further selling.

The euro could move later the same morning, even as the European Central Bank leaves rates unchanged. Updated staff forecasts are likely to show a higher near-term inflation profile alongside modestly slower growth, and a scenario analysis could help clarify how the Bank might assess risks under alternative energy price paths. Swap markets are pricing 40 basis points of tightening by year-end—equivalent to roughly one and a half rate increases—but that looks aggressive. Energy prices remain well below 2022 levels, inflation expectations are anchored, and domestic demand is still soft. The balance of risks points to a governing council more concerned about slowing growth than by the inflation impulse—and if that reading is correct, the euro faces renewed selling pressure.

Lastly, the Bank of Japan is all but certain to hold rates steady after raising them to a three-decade high in December. Governor Ueda’s commentary may prove more consequential than the decision itself, offering signals on how policymakers see price and wage dynamics shifting as imported energy costs climb and spring wage negotiations begin. Although markets have pencilled in July for the next increase, hawkish language on inflation risks could pull that timeline forward — and any resulting rise in domestic yields would help ease pressure on the yen.

Bottom line: This week may not bring a resolution to the major uncertainties facing markets, but it will reveal how the world’s most powerful central banks are framing the trade-offs. Currency trends could look very different by the time Friday rolls around.