Markets are soaring after US President Donald Trump announced an end to the war in Iran, saying that he and parliamentary Speaker Mohammad Bagher Qalibaf had “really hit it off” during a FaceTime call brokered by Jared Kushner. “Tremendous guy. Deeply misunderstood. Loves oceanfront real estate,” Trump posted at 4:17 AM.

Under the proposed settlement, Iran has agreed to give up nuclear enrichment activities in favour of simply getting rich. Tehran will recycle its oil revenues into a new dollar-pegged stablecoin called the PetroDollar™, which will be backed by partial ownership stakes in certain Trump-branded properties, including an unused room the term sheet describes as the “Library” at Mar-a-Lago. The Strait of Hormuz will be reopened to shipping in both directions, and the Republican Guard will expand its mandate from paramilitary operations to port logistics and cruise ship management, in what the White House is calling its “swords to timeshares” programme. Marco Rubio has agreed to chair the country’s interim governing council until a new Supreme Leader has been selected. Scott Bessent will act as interim central bank governor—and is already outlining plans to use the rial as a vehicle for intervening in the Japanese yen. Steve Witkoff, the president’s special envoy, is planning a joint Russo-American luxury tourism venture along Iran’s Caspian Sea coastline.

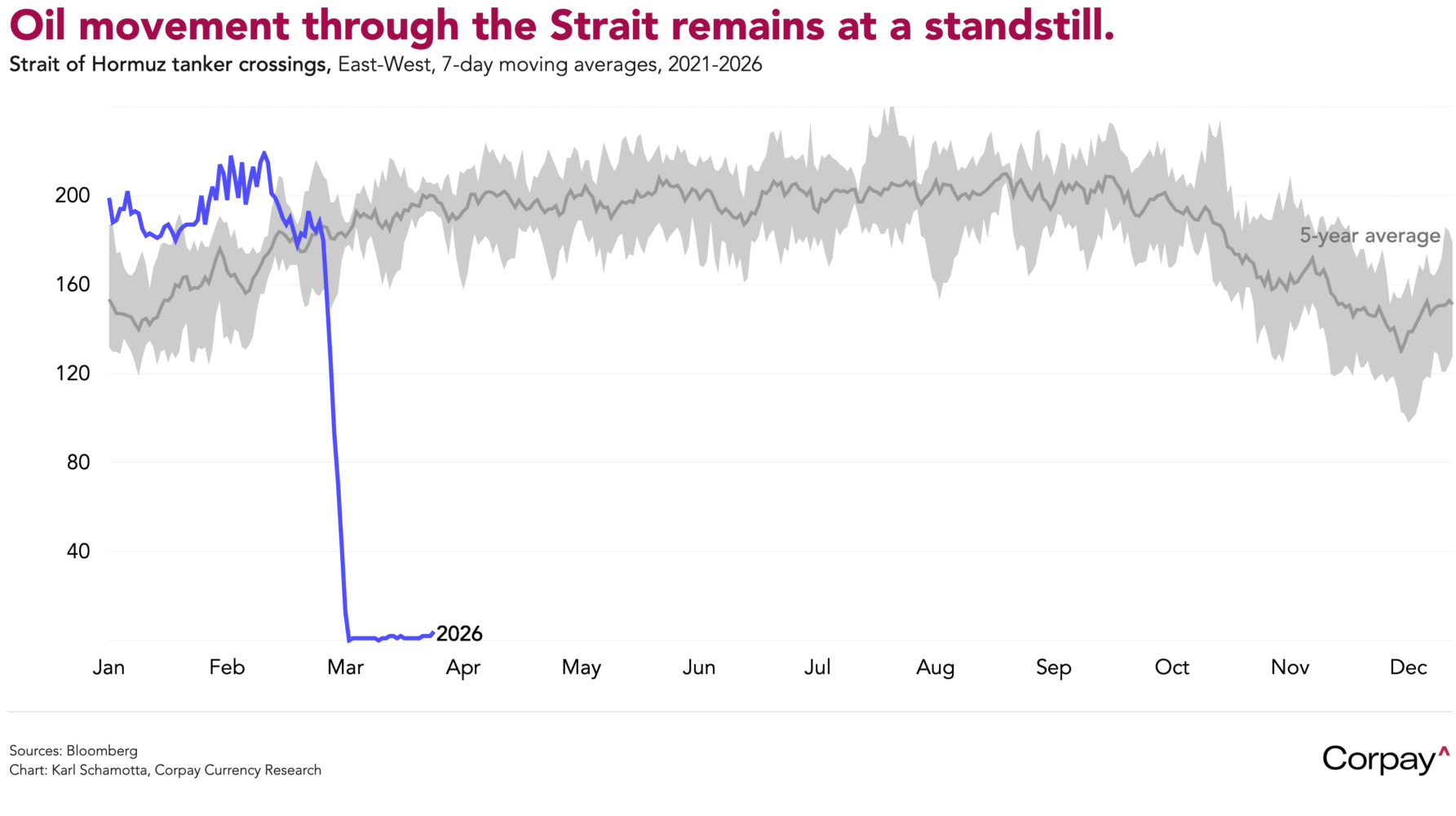

April Fools!

Here in reality, markets are rallying on growing conviction that President Trump is preparing to declare victory in the war with Iran. During yesterday’s session, Iranian president Masoud Pezeshkian signalled his country’s willingness to end hostilities provided the US accepts a five-point peace framework. After the close, Trump told reporters the US would be out of the war zone within two to three weeks, and his press secretary subsequently said he would deliver “an important update” tonight at 9 pm. By all indications, the president seems ready to withdraw without achieving meaningful regime change or Tehran accepting his fifteen-point plan—which includes opening the Strait of Hormuz—under the assumption that Iran will stop its attacks on shipping once the US-Israeli military onslaught ends.

Oil prices are retreating and currencies are edging toward pre-war levels, with the dollar down almost 1 percent against a basket of its most-traded rivals this week. The energy import-sensitive euro, pound, and Swiss franc are climbing, while the yen and renminbi hold steady. The Canadian dollar remains fragile after yesterday’s January gross domestic product report showed the economy starting the year on a weak footing. Treasury yields are coming down, equity futures are setting up for another day of gains, and implied volatility is falling across asset classes as traders begin stripping out tail-risk hedges.

The ebullience may not last. If past history is any guide, this evening’s presidential address will feature a declaration of victory in the US-Israeli campaign against Iran’s missile programme, barbs aimed at allies who have refused to get involved, and vague assurances that the war will soon be over. None of this, in itself, will alleviate the supply shock unfolding across global energy markets while the Strait of Hormuz remains closed.

There are reasons for optimism beyond the war, however. As the one-year anniversary of Trump’s “Liberation Day” tariff blitz approaches, it is clear that a substantial escalation in protectionist policy has had a surprisingly modest effect on underlying fundamentals. Tangible goods costs have risen and growth rates have softened, but the US is importing more than ever, deficits remain at record levels, and world trade volumes are in rude health, having jumped 7.2 percent in 2025 from a year prior. It is prudent to keep tail-risk hedges in place as the established order frays, but it is equally important to remember that the underlying calculus driving globalisation for centuries—comparative advantage and technology differentials between nations—remains firmly intact. For businesses, the implications are straightforward: it’s smart to protect against disruption in the near term, but foolish* to bet against continued growth in global trade over the long term.

*As Nabokov put it, “He was a pessimist, and, like all pessimists, a ridiculously unobservant man”