• Negative vibes. Another jump in energy prices & upward repricing in interest rates dampened risk sentiment. USD firmer. AUD & NZD underperform.

• Macro news. Asia exposed to higher energy costs. Growth in Australia set to slow. US Fed looks to be in no hurry to cut again. AU jobs report out today.

Global Trends

The positive sentiment that ran through markets over recent days gave way overnight, with the harsh reality of the situation in the Middle East and a few macro factors dampening the mood once again. European and US equities declined with the S&P500 shedding ~1.4%, while bond yields rose (US rates increased ~7-10bps across the curve), and the USD strengthened. EUR (the major USD alternative) dipped towards its multi-month lows (now ~$1.1452), GBP weakened (now ~$1.3257), and USD/JPY edged up to the top of the range it has occupied since mid-2024 (now ~159.86). Cyclical growth linked currencies like the NZD (now ~$0.5788) and AUD (now ~$0.7023) underperformed.

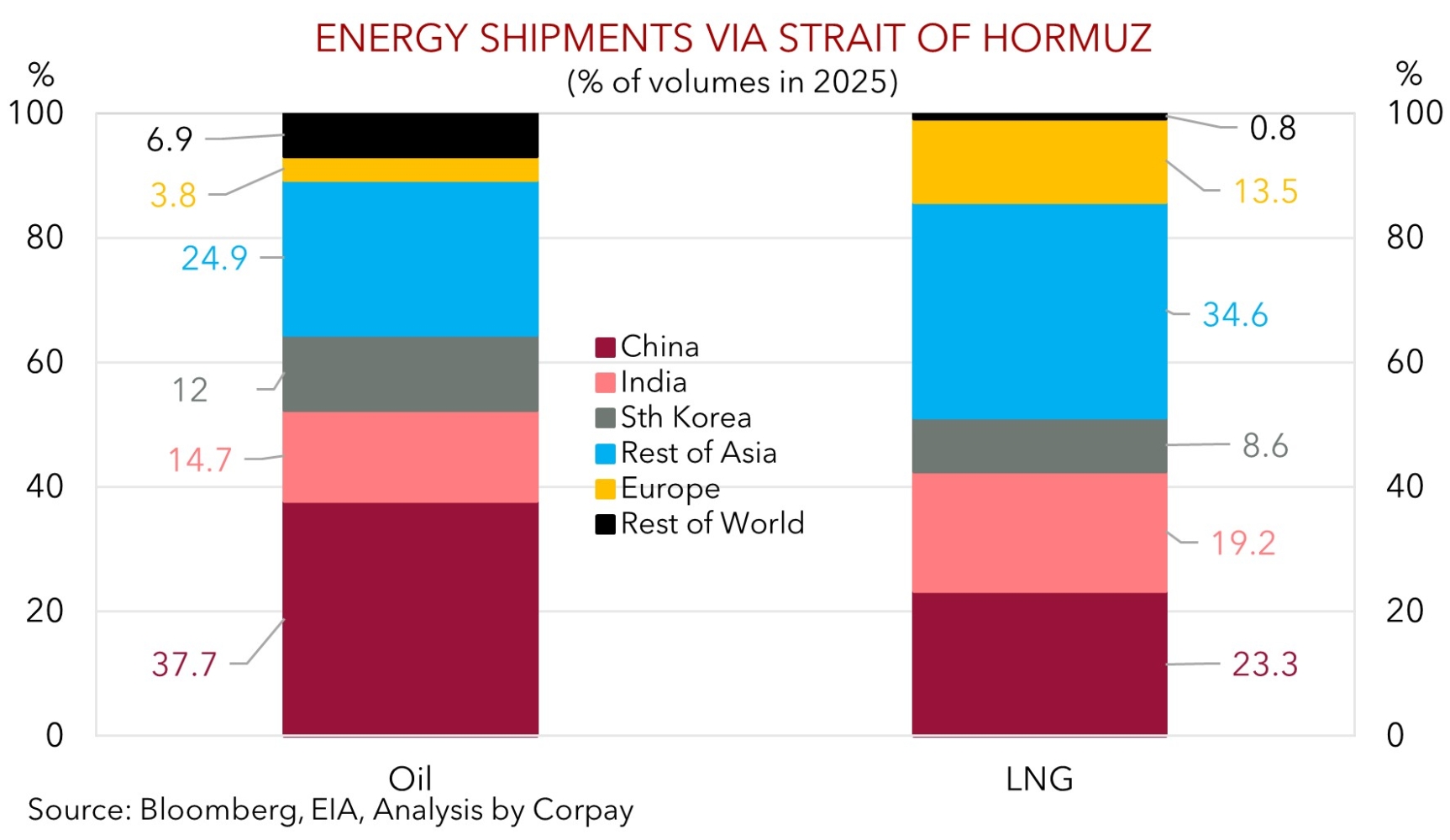

Oil prices jumped up again with Brent Crude near ~US$111/brl, ~7% above where it closed last week and ~90% higher than where it was tracking in mid-December. European natural gas prices also increased. The conflict in the Middle East shows no real signs of improvement and traders continue to factor in a hefty supply risk premium. Israel and Iran traded strikes on key energy facilities across the region with Qatar’s Ras Laffan Industrial City (a complex where the world’s largest LNG export plant is housed) suffered “extensive damage”. As outlined before, the surge in energy prices will push up inflation around the world, but it can also see growth slowdown sharply, especially after second round ‘butterfly’ effects on other industries are factored in. As our chart shows, given the bulk of oil and LNG shipped via the Strait of Hormuz (which is effectively shut) is sent to Asia it is the region in the direct line of fire from an economic standpoint.

Macro wise, US producer price inflation in February (which doesn’t capture the energy price spike) was hotter than predicted, indicating there are already concerning price pressures in the system. As expected, the Bank of Canada and US Fed kept interest rates on hold. The BoC indicated it would “look through” the Middle East war’s short-term inflation impacts, while the US Fed emphasized the “uncertainty” caused by the events. The Fed’s updated forecasts show the median expectation of the committee is for 1 rate cut in 2026 and another in 2027. Barring a sharp rise in unemployment, Fed policymakers look to be in no hurry to lower rates again given the push-pull forces at work, in our view. Indeed, when asked, Fed Chair Powell remarked that although the “vast majority” don’t see a hike as their base case for the next move the “possibility” it could be “did come up” during discussions. Markets are now only pricing in the next US Fed rate cut to happen

The BoJ (no set time), Bank of England (11pm AEDT), and ECB (12:15am AEDT) meet today. No changes in policy are anticipated. As outlined previously, the situation in the Middle East remains fluid, with the bursts of market volatility, negative global economic implications, and elevated oil prices (because of the US’ ‘net energy exporter’ status) a supportive backdrop for the USD.

Trans-Tasman Zone

The volatility stemming from the unfolding Middle East situation and jump up in energy prices, coupled with the upward repricing in US interest rate expectations, has supported the USD and exerted downward pressure on cyclical assets like the NZD and AUD. The NZD (now ~$0.5788) has also been weighed down a little this morning by softer than anticipated Q4 NZ GDP with growth slowing more than expected and the economy expanding by just 0.2%qoq.

The AUD (now ~$0.7023) has declined to be back trading below its 1-month average, with the AUD also losing ground on the major cross-rates. The AUD shed ~0.4-0.9% against the EUR, JPY, GBP, CAD, and CNH over the past 24hrs, while AUD/NZD has tread water near the upper end of its ~13-year range (now ~1.2116).

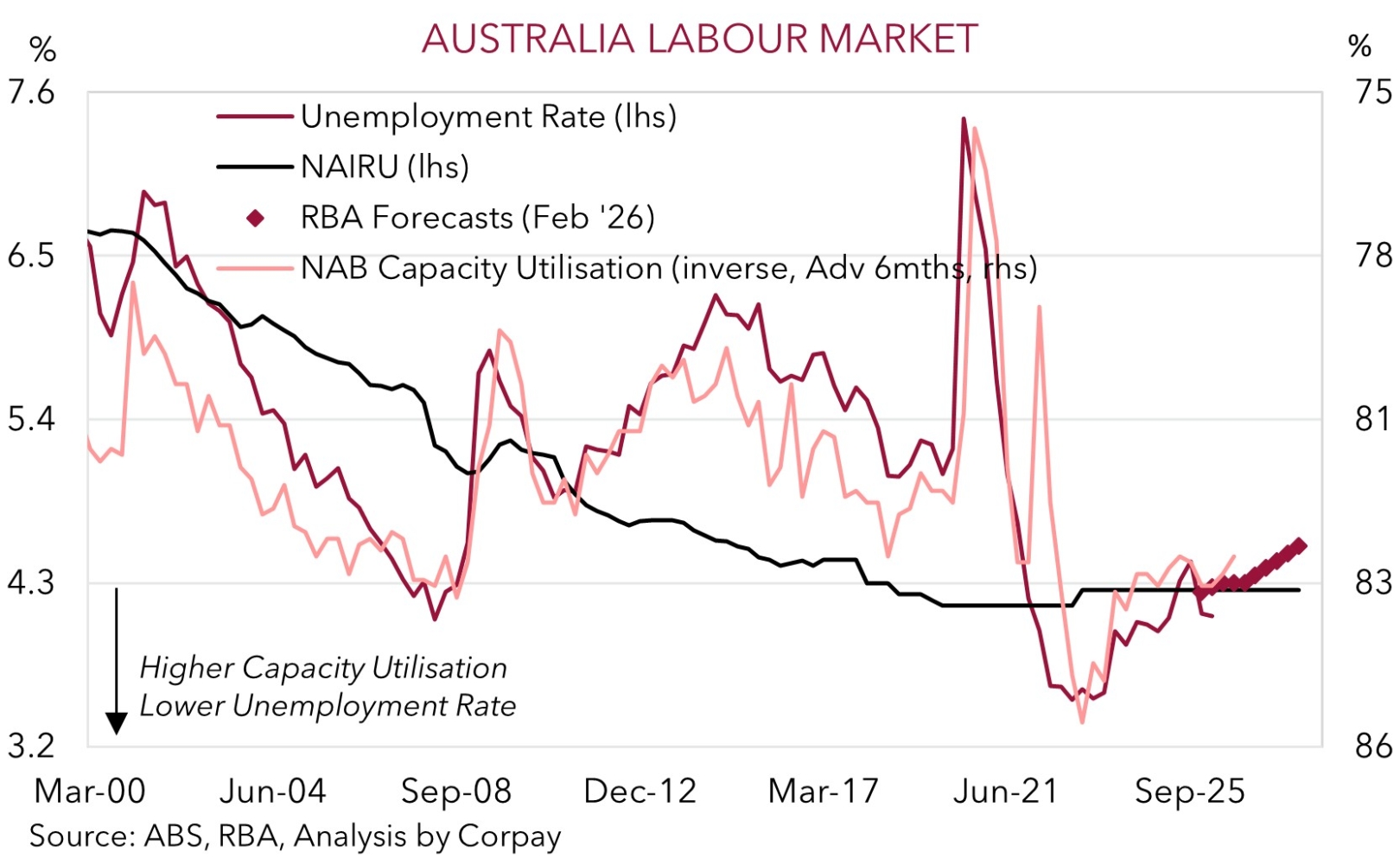

Today in Australia the volatile monthly jobs report is due (11:30am AEDT). The labour market is a lagging indicator (as a rule of thumb the unemployment rate today reflects the state of the economy ~6-months ago). As such, we think the February employment figures should show conditions remain solid, though based on the trends in forward indicators like capacity utilization there is a chance the unemployment rate ticks up from 4.1%. That said, barring a large positive surprise, we believe global forces will have a more lasting impact on the AUD than domestic data in the near-term.

On balance, we feel that given how much RBA tightening is still factored into the Australian interest rate curve (markets are pricing in another ~48bps of hikes by year-end), the situation in the Middle East (which is set to drag on Asian/global growth), and with the negative domestic economic consequences of higher mortgage rates and fuel costs set to show up over coming months, downside risks for the AUD are lurking. On our figuring, the back-to-back RBA rate rises (with another likely to be delivered in May) and substantial jump in fuel costs mean the outlook for household consumption has worsened. Household spending is the largest part of the Australian economy (~52% of GDP). A slowdown in activity over future months should be expected, and a lift in unemployment could follow down the track given the lags. Added to that, the AUD is ~2% higher than our ‘fair value’ estimate, and above where various yield/interest rate differentials suggest it should be. Bottom line, we believe too many positives are baked into the AUD. While the higher level of interest rates and wider yield spreads point to a higher average range for the AUD than what we saw the past few years, it doesn’t necessarily mean there will be much more AUD appreciation because of the worsening global/domestic growth trajectory.