Financial markets are staging yet another relief rally after the Wall Street Journal reported that Donald Trump is considering declaring victory in the Iran conflict without establishing control over the Strait of Hormuz. According to an article published last night, the president now believes the US should limit itself to incapacitating Iran’s navy and missile forces, unilaterally ending large-scale attacks before achieving the regime change goals set out at the war’s onset. Relative to the alternatives, this is a market-friendly outcome: it would give Tehran an opening to pull back on its strikes on regional infrastructure and allow shipping to resume. It would also, however, leave the Republican Guards holding a recently-demonstrated weapon at the throat of the global economy.

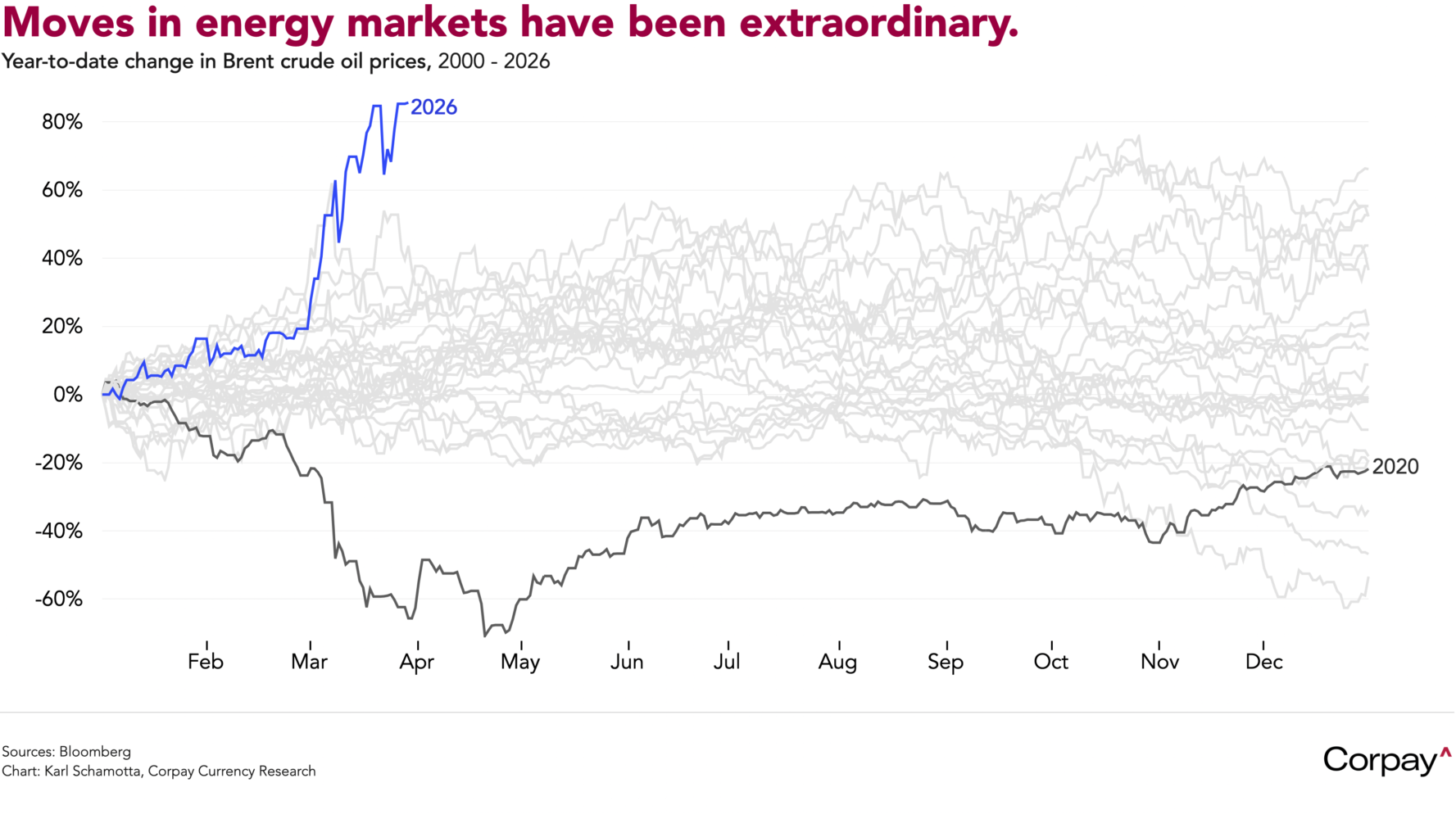

Energy prices are retreating from yesterday’s highs, but remain far above pre-war levels. With attacks continuing across the Middle East, more US troops arriving, and Yemen’s Houthis joining the war, traders are inclined to wait for solid confirmation of a change in strategy before abandoning the scramble for deliverable supplies. After a series of unusually-violent moves, the global crude oil benchmark*—Brent—is holding near $115, barrels of West Texas Intermediate are trading hands for more than $103, and European natural gas costs are still up more than 80 percent this year.

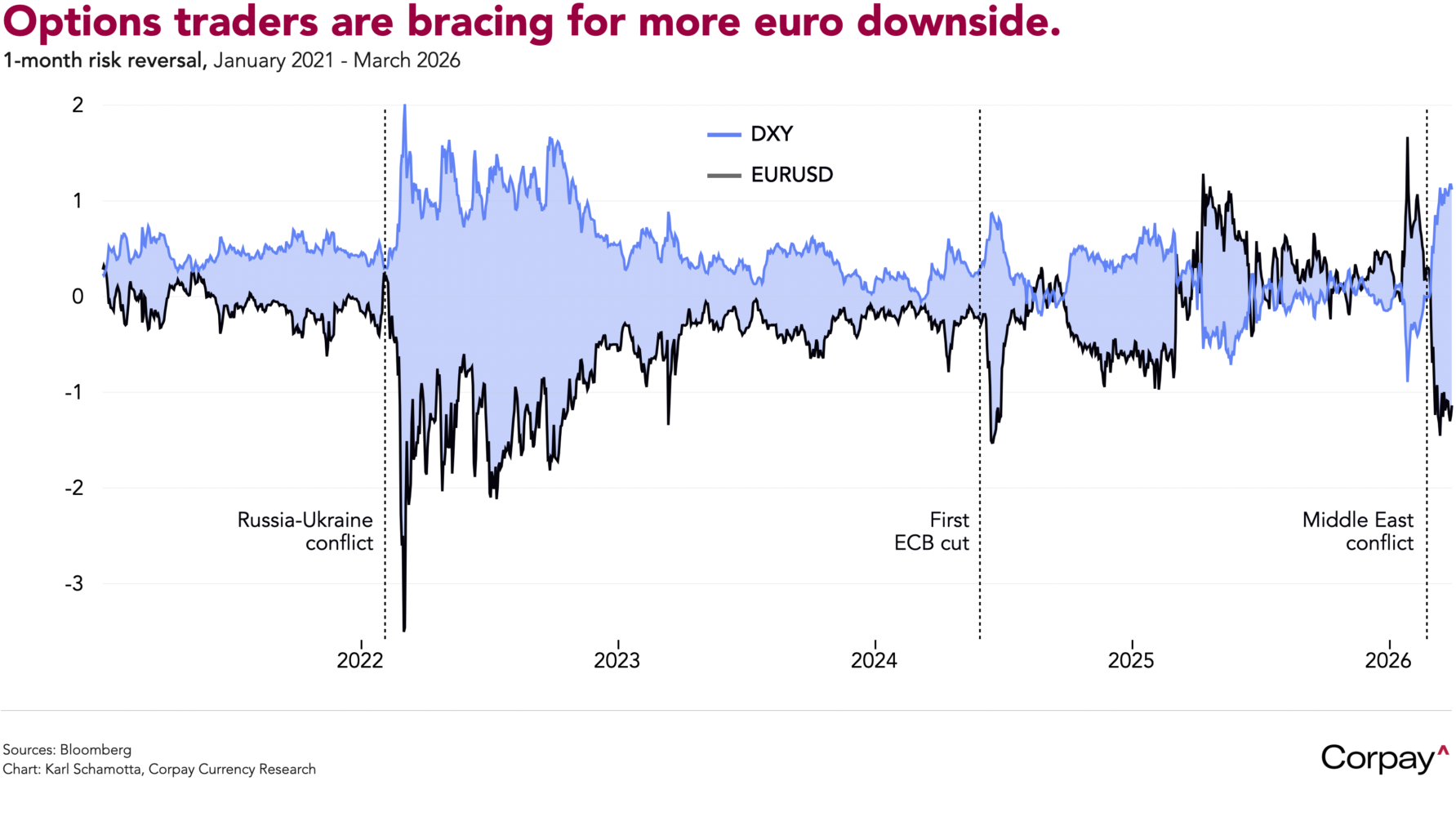

Evidence of an incoming inflation shock is beginning to surface. Data released this morning showed euro area headline prices jumping 2.5 percent in the year to March, accelerating sharply from 1.9 percent the prior month as a 4.9 percent year-on-year surge in energy costs lifted inflation to its highest since January 2025. The European Central Bank is expected to respond with two or three rate increases this year as policymakers seek to forestall wage and price spillovers, and currency traders are betting the economy will suffer, growing more slowly than it would otherwise. The euro has slipped below the psychologically important 1.15 threshold against the dollar, and options markets are positioned for further bouts of weakness.

In the United States, where the central bank has a more complex dual mandate, Federal Reserve officials seem content to leave policy settings where they are. In separate appearances yesterday, Chair Jerome Powell and New York Fed President John Williams both signalled patience. Powell said policy was “in a good place” to wait and see how the economy absorbs the Iran-related supply shock, cautioning that pre-emptive rate increases could backfire: “By the time the effects of a tightening in monetary policy take effect,” he said “the oil price shock is probably long gone, and you’re weighing on the economy at a time when it’s not appropriate”. Inflation expectations, he added, look well anchored beyond the short term. Williams, who serves as vice chair of the Federal Open Market Committee and is widely regarded as a bellwether for the group, acknowledged that the war could simultaneously raise inflation and dampen activity—and that this is already playing out—but nonetheless judged that current rate settings are appropriate for reaching the central bank’s employment and price stability goals. Pricing on the Fed’s policy trajectory has flipped once again, with investors now seeing a rate cut as more likely than a hike by year end.

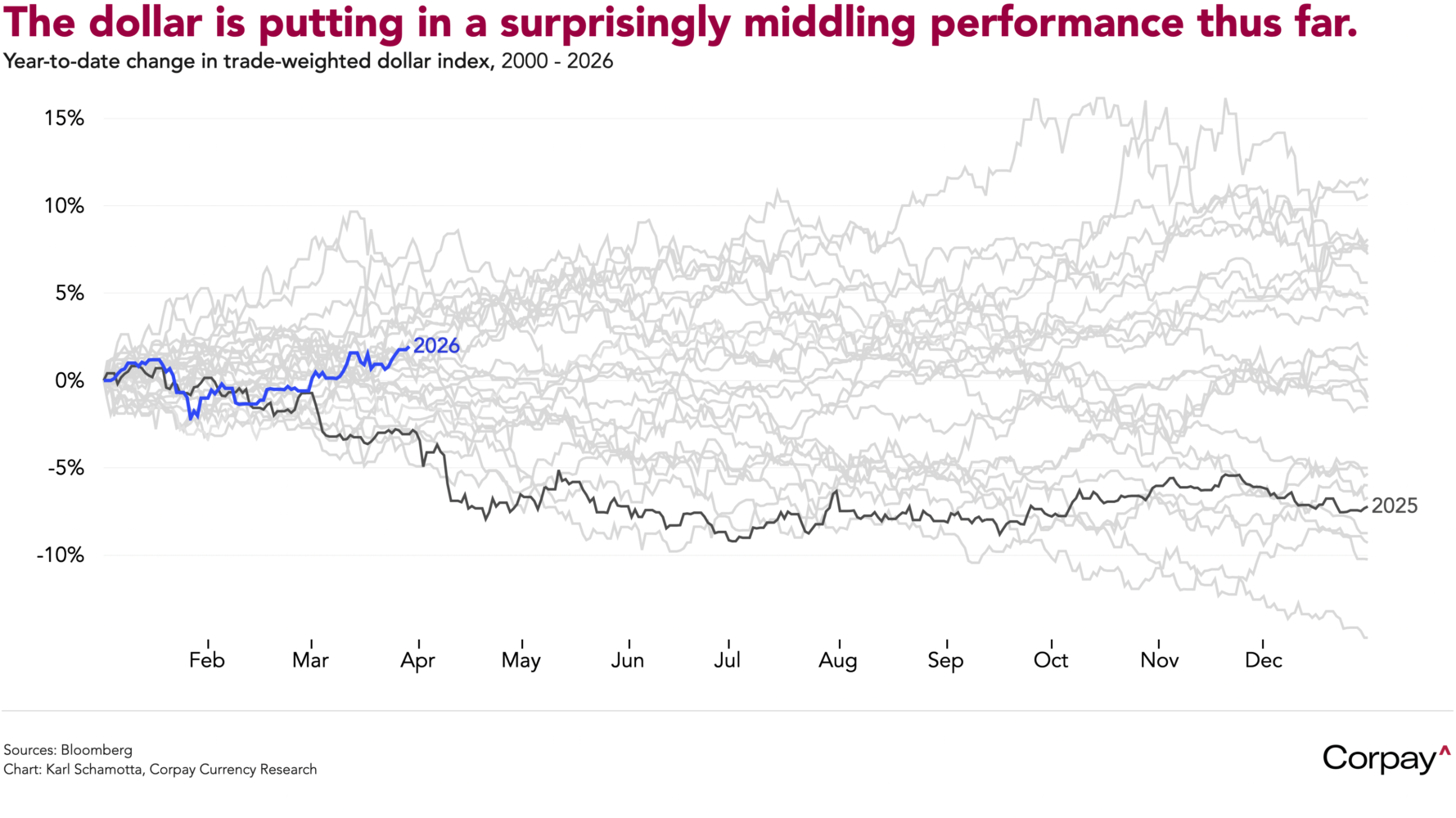

The trade-weighted dollar looks set to close the month with its strongest performance since 2024, but its year-to-date gains appear more pedestrian, particularly when measured against past conflicts. This likely reflects a combination of factors: narrowing cross-currency interest rate differentials among advanced economies, an ongoing rotation out of portfolios that had grown too technology-heavy in recent years, growing fiscal concerns, and a reluctance among international investors to deploy more capital into an increasingly unstable American economy. Taken together, they suggest the currency could face stronger headwinds once the new quarter gets under way.

*Note that you might see similar charts across financial commentary this morning. That’s because Bloomberg put a version of it on the terminal homepage yesterday. No one ever accused foreign exchange strategists or economists of being independent thinkers : )