Good morning. After a series of early-week distractions, currency market drivers are shifting back toward economic fundamentals today, with mixed US data keeping yields within tight ranges and the Japanese yen becoming a key focal point ahead of a potential snap election. Equity futures are setting up for a negative open after modest losses in yesterday’s session, Treasury yields are holding firm across the curve, and the dollar is trading almost imperceptibly lower against a basket of its major counterparts.

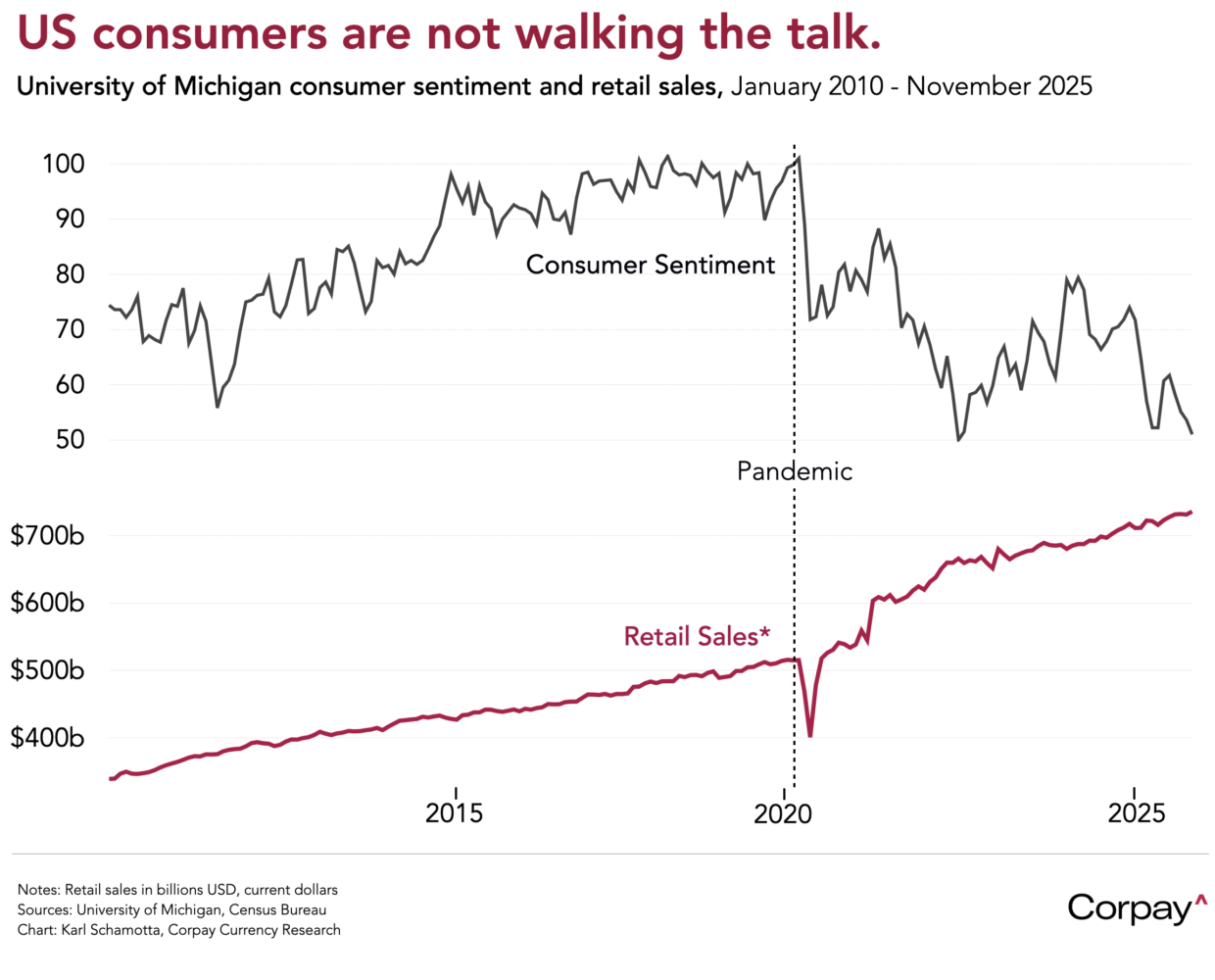

American consumers continued to engage in retail therapy in November. According to figures published by the Census Bureau this morning, total receipts at retail stores, online sellers and restaurants rose 0.6 percent on a month-over-month basis, beating forecasts set closer to the 0.5-percent mark, while so-called “control group” sales—with gasoline, cars, food services, and building materials excluded—rose 0.4 percent, matching expectations. This comes even as respondents express negative views when contacted by pollsters, sending measures of consumer sentiment down to historic lows, and potentially indicating that fundamentally-strong balance sheets among upper middle class and wealthy households are helping support growth across the economy.

Taken together, today’s on-target rise in producer prices and yesterday’s US consumer price update ultimately left monetary policy expectations unchanged, underlining our belief that labour market conditions have taken precedence over inflation dynamics in investor perceptions of the Federal Reserve’s reaction function. Although methodological quirks related to the Bureau of Labor Statistics handling of the late-autumn government shutdown led to a degree of wariness among economists, both the headline and core measures of inflation climbed by less than anticipated in December, and evidence of tariff-led cost increases in import-sensitive tangible goods categories remained marginal at best. Services prices continued to rise a little faster than would once have been comfortable, but not by enough to lift long-run inflation expectations or unsettle Treasury yields.

With a number of news sources reporting that prime minister Sanae Takaichi is poised to call a snap election and press for expansionary fiscal measures, the Japanese yen has hit a patch of turbulence. Against the dollar, the currency tumbled to an 18-month low last night, but then reversed higher when authorities publicly flagged “extremely regrettable” “one-way” moves in markets and reiterated that all options are on the table, putting traders on intervention watch. Takaichi’s push to translate her extraordinary personal approval ratings into a decisive governing mandate has led to a revival in bets on more government spending, restraints on monetary tightening, and higher inflation, lifting equity markets while sending the currency spiralling toward the 160 threshold that has historically triggered buying efforts from the Bank of Japan.

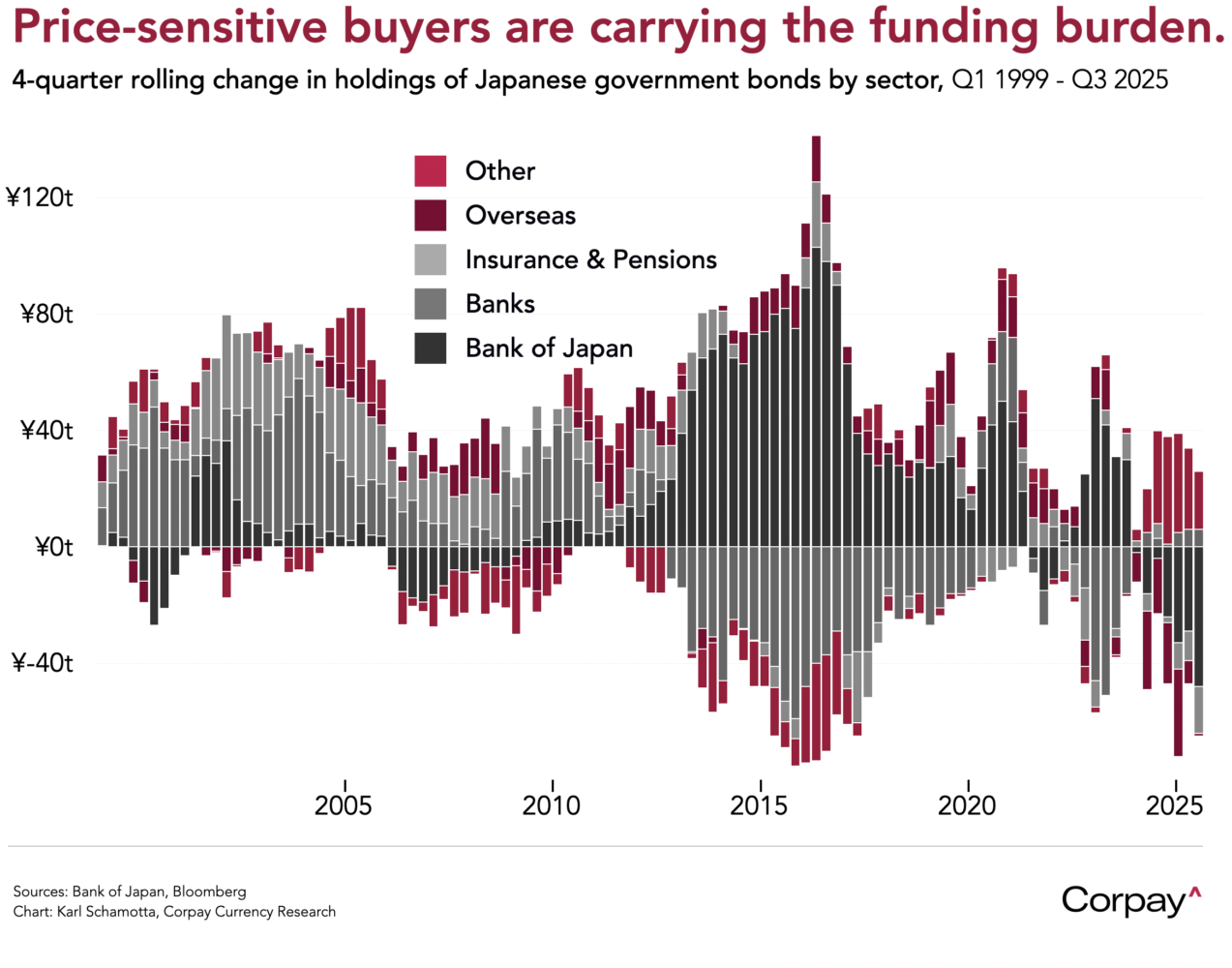

Developments in Japanese bond markets are arguably more consequential for the global economy. The Japanese government is by far the most indebted in the G7, and long-dated bond yields are climbing rapidly, prompting fears of a crisis in one of the world’s biggest bond markets and putting upward pressure on term premia in other countries. We don’t see recent moves as the beginning of a tantrum, but instead as a reflection of shifts in demand and supply within domestic fixed income markets as the Bank of Japan reduces its buying activity, inflation expectations ratchet higher, and returns improve on local corporate equities, reducing demand for safe-haven assets. In our view, price-sensitive investors are seeing a range of attractive opportunities opening up, pointing to a longer-term recovery in the Japanese economy, and eventually, in the yen itself.

Ahead today, the Supreme Court has another “opinion day” scheduled, meaning that a ruling on Donald Trump’s tariff regime could come as soon as 10:00 this morning. Prediction markets remain convinced the court will strike down the president’s use of the International Emergency Economic Powers Act to pass last year’s “reciprocal” and “fentanyl” levies—a development that could result in massive refunds for many businesses and add to the tailwinds behind the American corporate sector—but the administration is expected to pivot toward other legal avenues, meaning that the overall boost to growth could prove fairly minimal.

Given our belief that relatively low currency volatility levels are masking deep structural vulnerabilities—an over-concentration in growth drivers, fading US exceptionalism, rising fiscal and political risk, and an erosion of the post-war economic order—we have updated our views on the year ahead. In An Unstable Equilibrium, our team explores the global economic backdrop, market dynamics, and what we believe will matter most in 2026, focusing on where consensus expectations may be most vulnerable. To view, click here