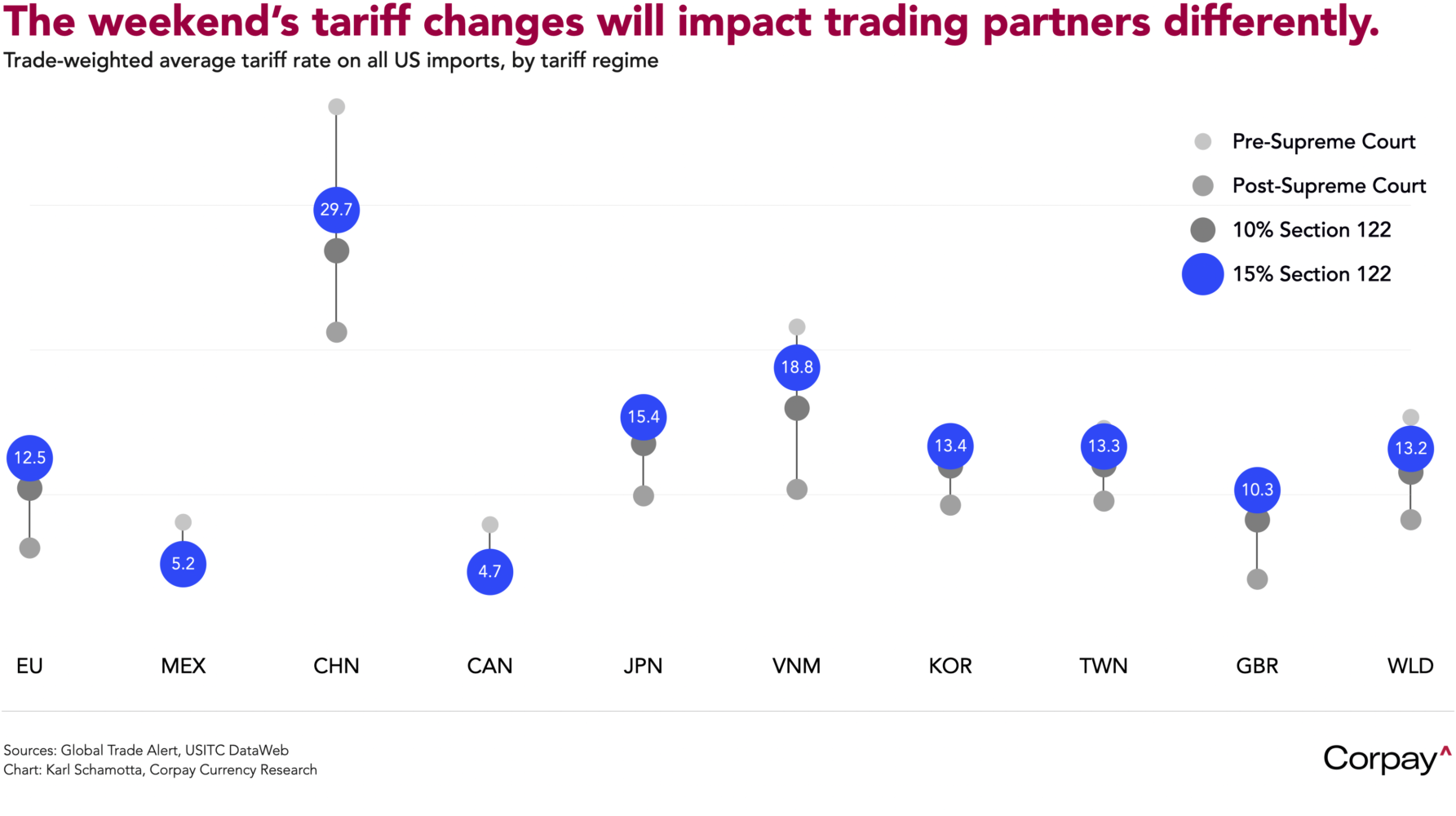

Equity markets are lower and the dollar is weaker against all of its major counterparts after the US cycled through four different tariff frameworks between Friday morning and Saturday afternoon, underscoring the policy uncertainty facing the world’s largest economy. After the Supreme Court struck down President Trump’s use of the International Emergency Economic Powers Act, he moved to replace the measures with a flat-rate 10 percent levy on all US imports under Section 122 of the Trade Act of 1974, which he then raised to 15 percent on Saturday. The new tariff, which is set to take effect tomorrow and will lapse within 150 days unless renewed by Congress, includes a wide range of exemptions that will lower overall rates for some countries—like Canada, Mexico, and China—while raising them for others.

A number of conflicting cross-currents are hitting financial markets. The euro, sterling and Canadian dollar remain tightly rangebound, while the yen and Swiss franc are outperforming on a modest pickup in safe-haven demand. The Mexican peso is down about 0.5 percent after authorities killed the leader of a major cartel, triggering reprisals in Jalisco. Commodity prices, led by oil and gold, are firming as traders brace for a possible attack on Iran in the coming days.

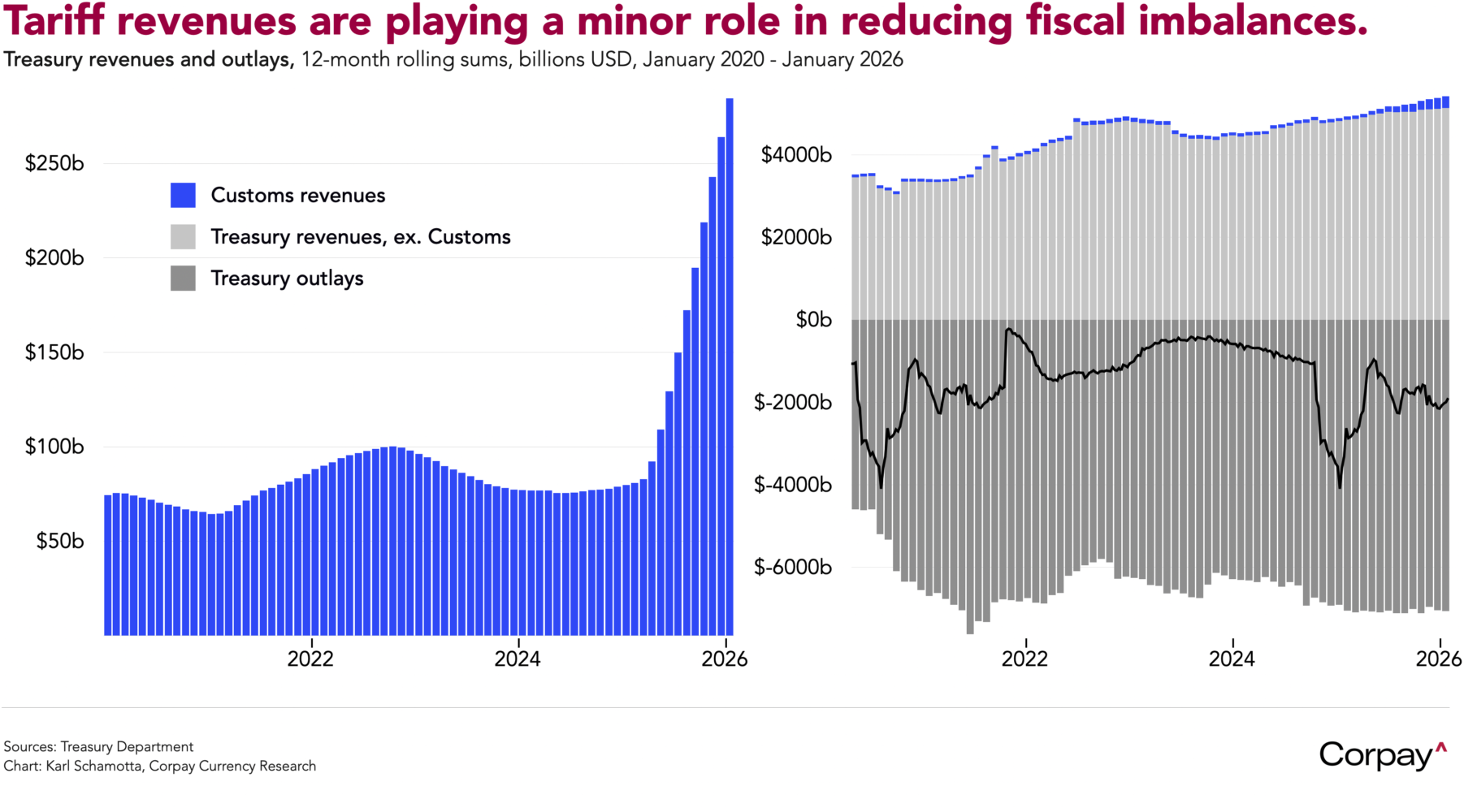

Refunds are likely to widen US budget deficits and increase Treasury funding needs, but the effect should be gradual and modest. Firms pursuing claims through the lower courts could wait months or years for payment, and at roughly $140-170 billion, the amounts at stake are small relative to the government’s $7 trillion in annual outlays. Yields on 10-year Treasuries, which move inversely to prices, are holding near 4.07 percent, essentially unchanged from Friday’s opening levels.

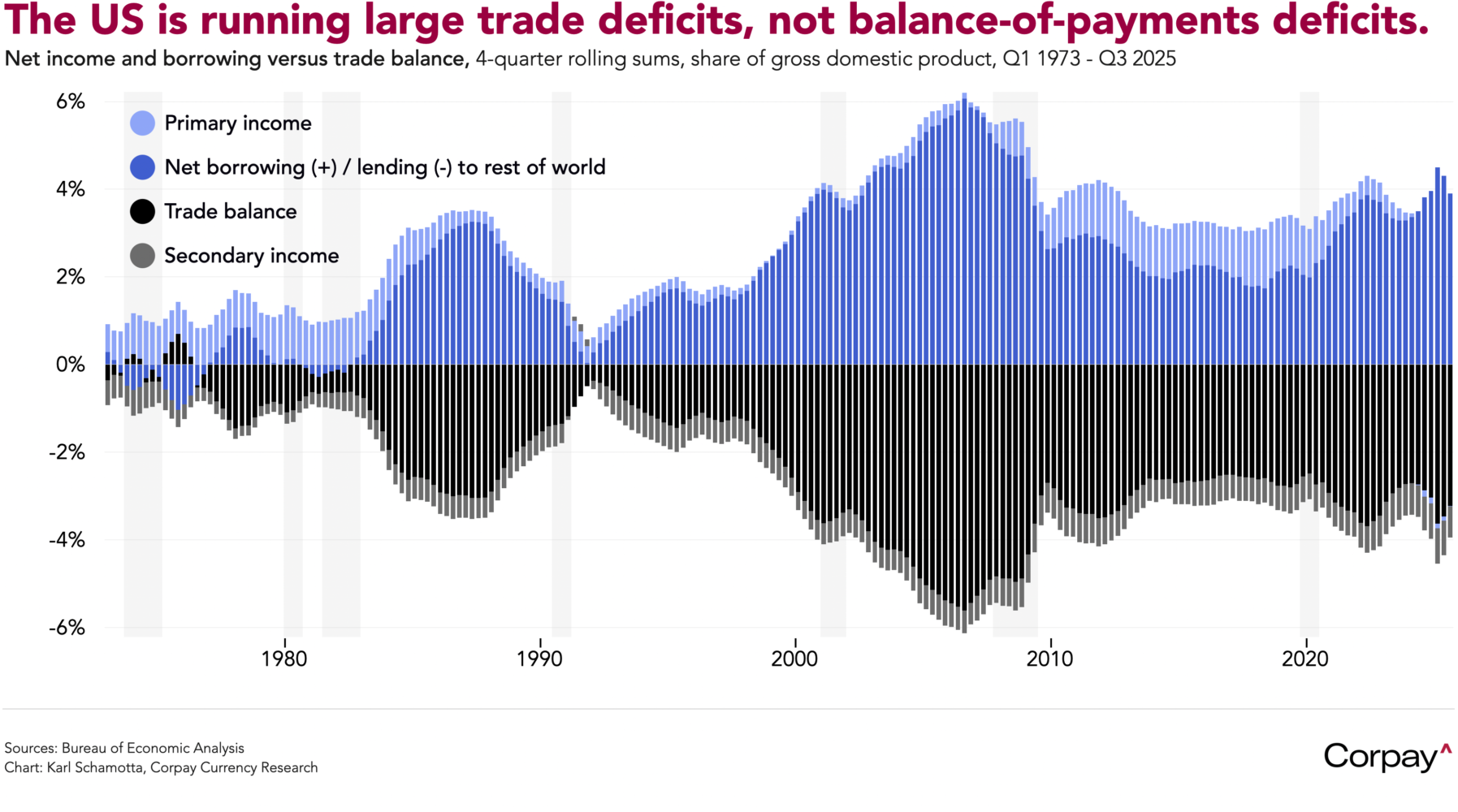

A fresh round of legal challenges is likely in the weeks ahead. Section 122, drafted after the dollar’s link to gold came under pressure in the late 1960s, grants the president limited authority to impose temporary tariffs to address large balance-of-payments deficits, prevent a sharp currency depreciation, or support international adjustment efforts. But a balance-of-payments deficit is not the same as a trade deficit. The US runs a large goods and services shortfall, yet continues to attract substantial foreign capital, and there is little evidence that markets are constraining its ability to finance its excess consumption. The administration itself made this distinction in previous legal filings, saying that Section 122 doesn’t have “any obvious application here, where the concerns the President identified in declaring an emergency arise from trade deficits, which are conceptually distinct from balance-of-payments deficits,” and has implemented a range of policies that appear designed to reduce US savings rates while encouraging inward capital flows**.

The dollar could ultimately benefit from the weekend’s events. If the administration doesn’t find other ways to sidestep Congress, the Supreme Court’s judgment, the legal quagmire ahead, and signs of growing political opposition to the administration’s tariff agenda are evidence that the US republican system of government is working as intended, placing checks and balances on the president’s unilateral use of executive power, and reducing the likelihood of extreme policy pivots in the days and months ahead. The risk discount that has been embedded in US assets since last year’s ‘Liberation Day’ tariff announcement might shrink over time, allowing favourable fundamentals to play a bigger role in driving currency valuations.

A significantly-quieter economic calendar beckons this week. Tomorrow’s Conference Board consumer confidence report, Thursday’s jobless claims and Friday’s producer price data should offer insight into US conditions, but are unlikely to shift expectations materially. President Trump’s State of the Union may include references to tariff “rebate cheques”, though markets will weigh any stimulus against the fiscal cost. In Canada, Friday’s gross domestic product numbers are expected to show modest growth in December alongside a slight contraction over the final quarter of 2025, further undermining the case for rate hikes this year.

In theory*, the “trade balance” is a narrow concept, capturing the degree to which a country’s imports of goods and services exceed its exports. The “balance of payments” is broader, reflecting the inflow of foreign currency relative to outflows across all external transactions including trade, investment income, reserves, asset transfers, and investment transactions. In accounting terms, the balance of payments must always sum to zero, with spending and income imbalances financed through the selling of claims on future income or assets to the rest of the world, but can exhibit signs of stress when foreign investors become unwilling to buy those claims. Typically, this shows up in higher interest rates, falling exchange rates, and—in emerging markets especially—a drop in currency reserves.

**Theory may not matter in practice. Courts will struggle to parse these distinctions, and the administration is likely to move ahead with new tariffs under separate legal avenues long before any judgment is passed.

***Lowering taxes, pushing for lower interest rates, and actively encouraging foreign investment are policies that tend to increase trade and balance of payment imbalances, not decrease them.