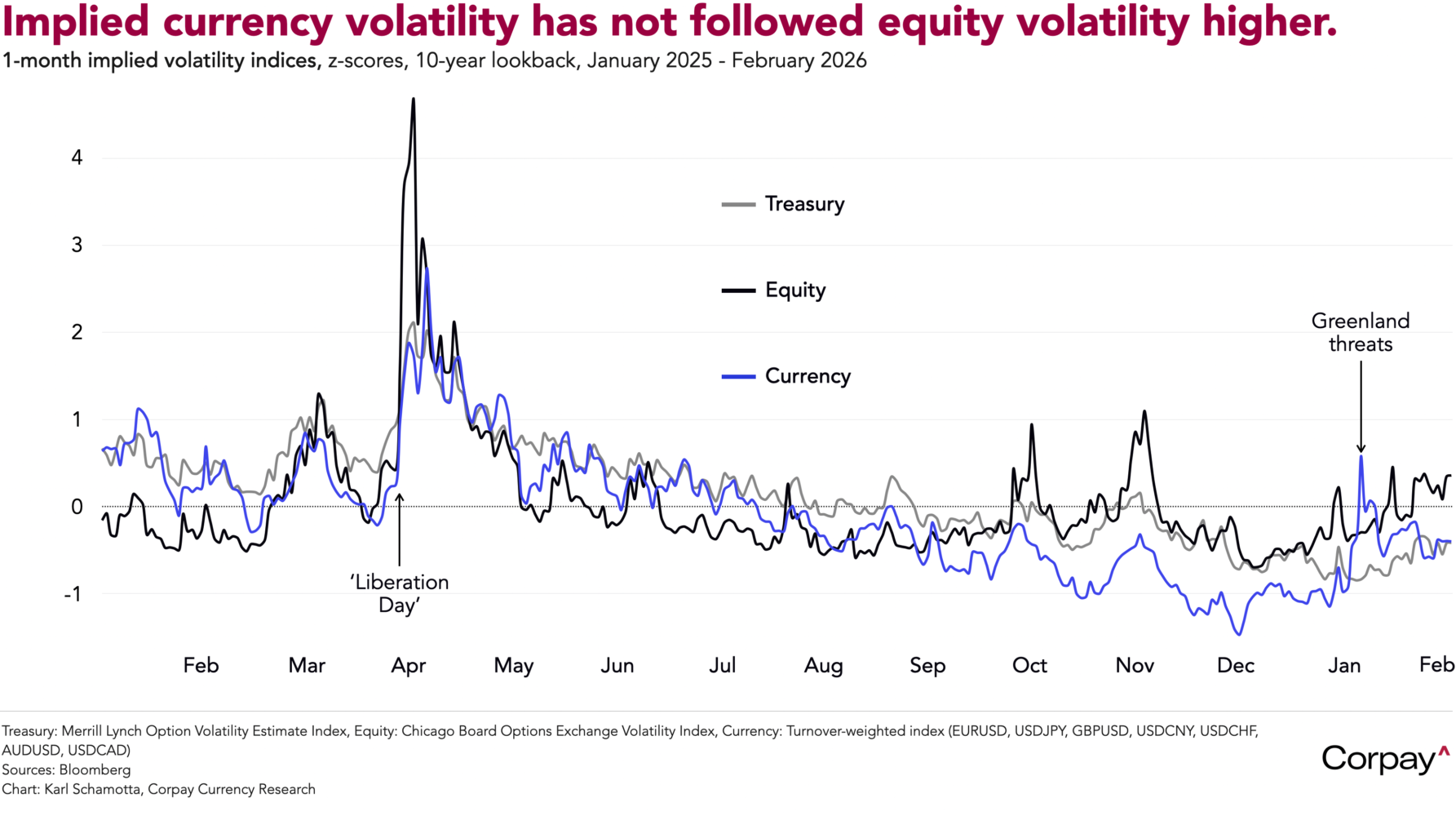

Good morning. The dollar is advancing against most of its major counterparts and measures of implied currency volatility are tracking near historic norms as foreign exchange traders downplay tariff risks and shrug off signs of a shift in investor sentiment around the US technology sector.

US Customs began collecting a 10-percent tariff on goods not covered by exemptions this morning—below the 15 percent threatened by President Trump in a weekend social media post. The White House reportedly remains committed to the higher levy, which would raise import costs on products from a number of key trading partners including Japan, the United Kingdom, and the European Union, but hasn’t articulated an execution timeline.

Separately, the Wall Street Journal said the administration is considering raising national security tariffs on at least six industries in the months ahead, adding batteries, electrical, and telecoms equipment to the list of investigations already underway against products like drones, robots, semiconductors, solar panels, and pharmaceuticals. The new tariffs, which would come under Section 232 of the Trade Expansion Act of 1962, require the administration to conduct extensive investigations before implementation, but could see average applied tariff rates ratcheting higher once again, particularly for the largest Asian exporters. This implies that US businesses are likely to busy themselves with another round of inventory front-running—and that trade data will continue to throw up false signals.

Equity futures are pointing to a slightly more constructive open after a selloff in software companies knocked major indices lower during yesterday’s session. The catalyst appears to have been provided by a paper from Citrini Research titled “The 2028 Global Intelligence Crisis”—which outlines a hypothetical scenario in which artificial intelligence advances wipe out existing business models and drive the unemployment rate above 10 percent—but clearly also reflects deeper concerns about structural overvaluation in the US technology sector.

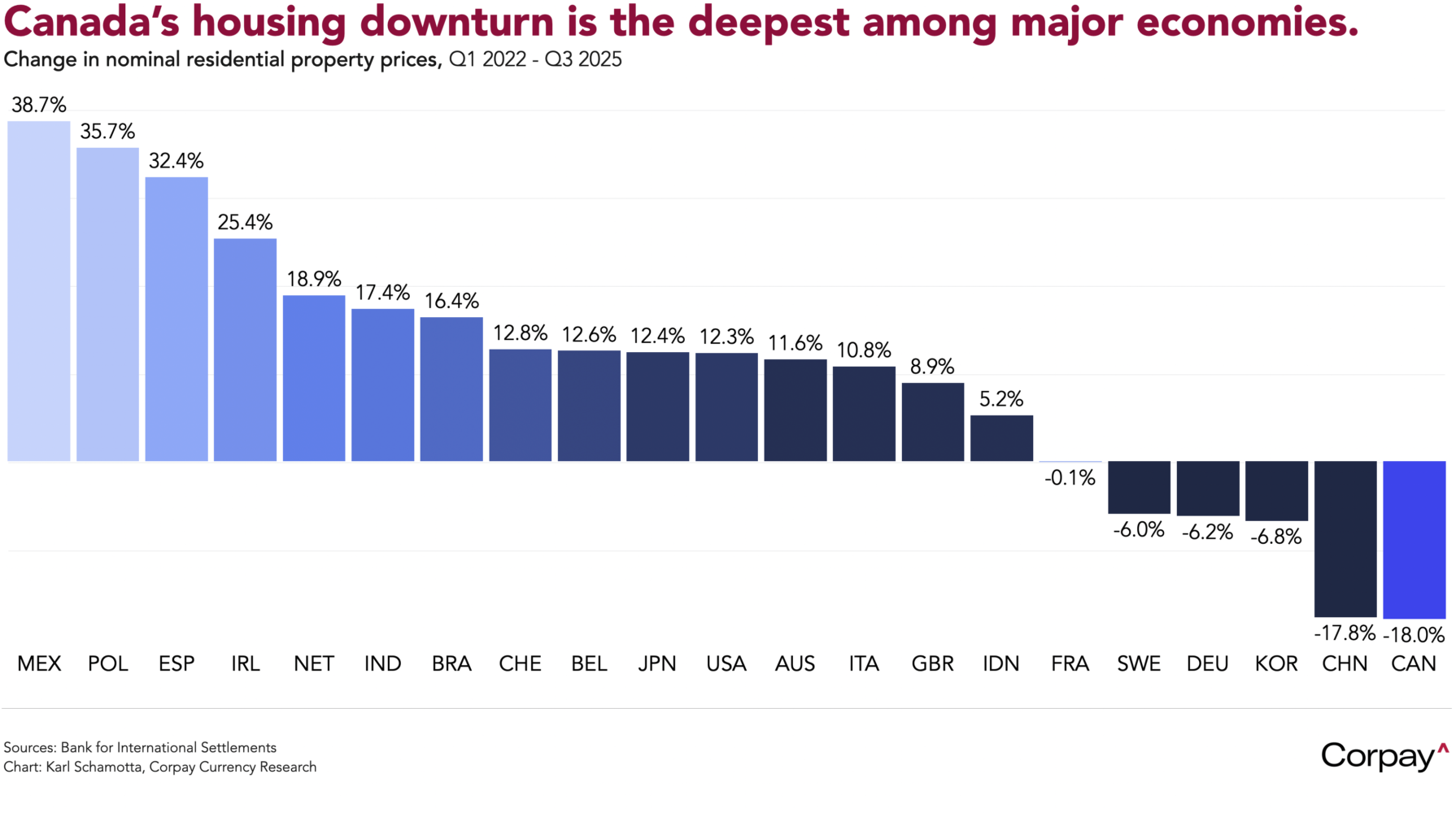

The Canadian dollar remains on the defensive despite avoiding steep tariff increases in the Trump administration’s latest round. That likely reflects lingering uncertainty around USMCA negotiations, with traders braced for disruptive headlines even if the agreement ultimately survives. It also speaks to domestic weakness: Canada is still in the grip of one of the deepest housing downturns in the advanced world. After spectacularly-outsized gains before and after the pandemic, home prices have fallen more sharply than in peer economies and are showing little sign of stabilising.

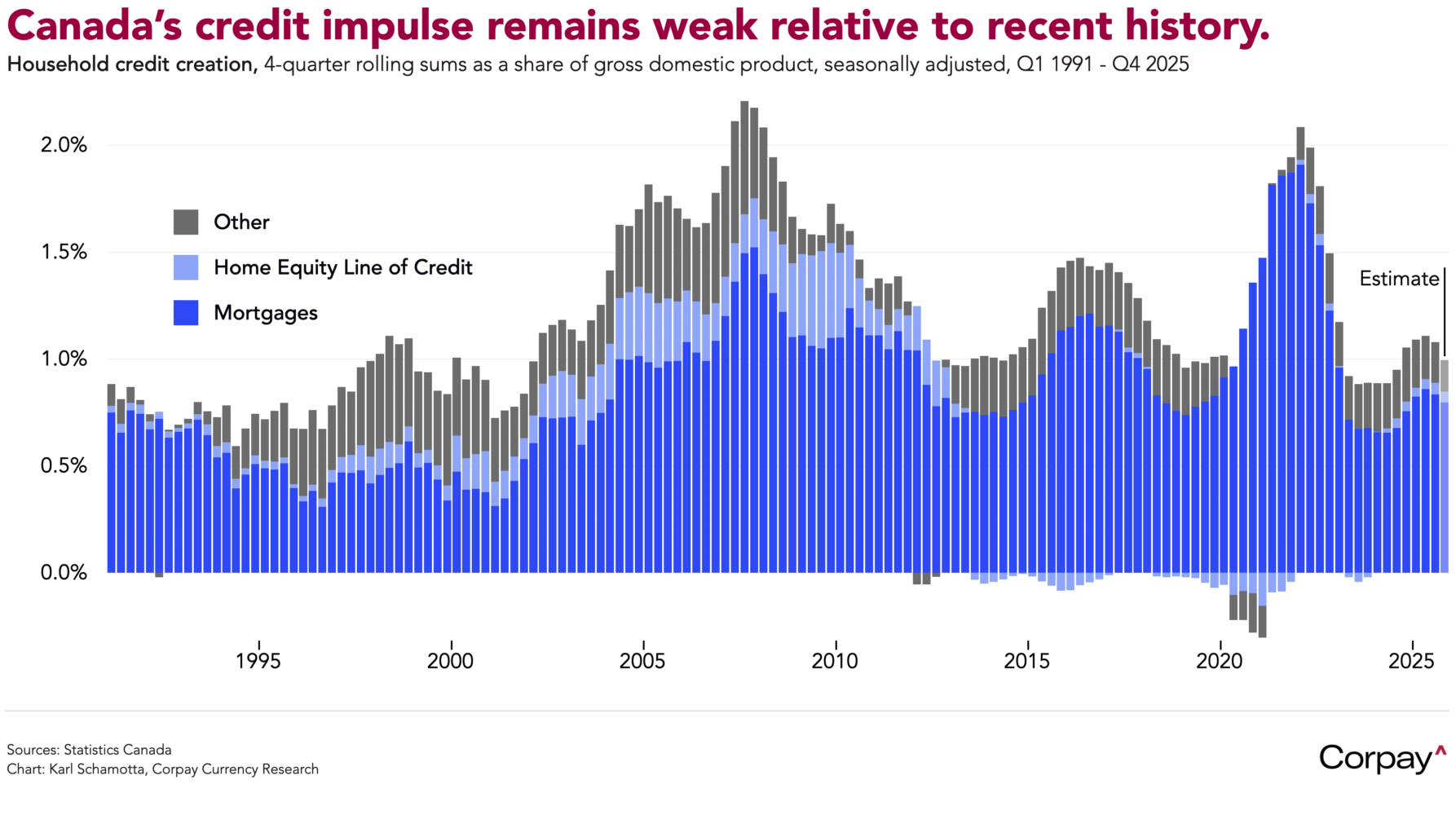

Credit flows to households have dropped sharply from their peak, echoing the pattern seen in the US after the 2008 housing crash. With speculative activity fading and overindebted homeowners growing less willing to extract equity, spending and investment are under pressure, weighing on growth relative to the still-resilient US economy. To us, this backdrop is likely to represent a continuing headwind for the Canadian dollar in the months ahead.

Outside North America, currencies remain broadly rangebound ahead of this morning’s consumer confidence measure from the Conference Board and tonight’s State of the Union address. The euro and pound are treading water against the dollar, the yen is edging lower as Prime Minister Sanae Takaichi pushes back against expectations for further rate hikes, and the Chinese yuan is firming as markets reopen following the Lunar New Year holiday. A slate of Federal Reserve speakers is due in the coming hours, but markets appear well conditioned for a mildly hawkish tone. Instead, geopolitical developments—particularly on the Iran front, and perhaps articulated during Trump’s speech—look more likely to provide the catalyst needed to push exchange rates out of their current holding patterns.