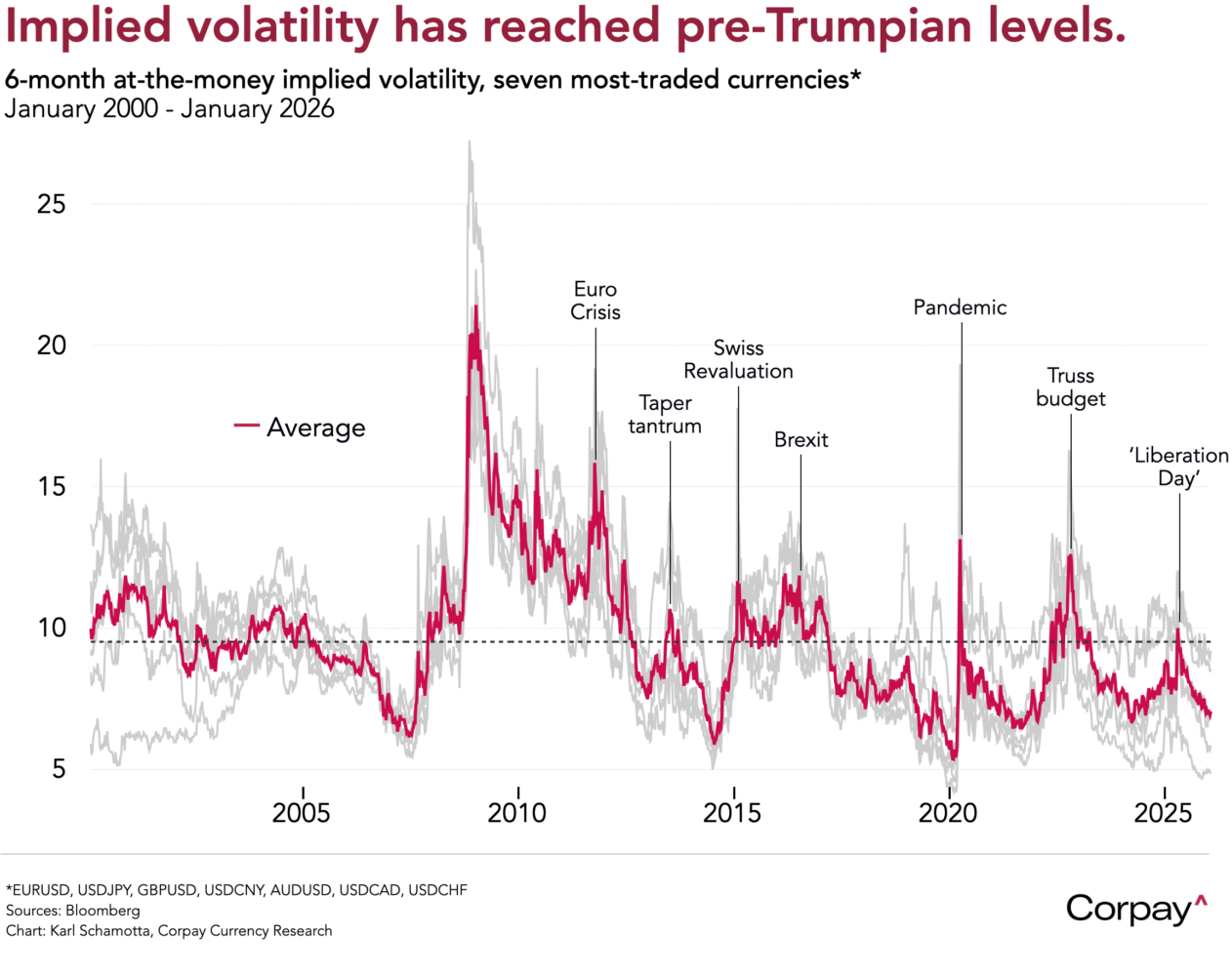

Good morning. Currency markets have slipped back into extremely tight ranges as geopolitical fears recede and incoming data point to “Goldilocks” conditions across much of the advanced world. Realised volatility across asset classes remains exceptionally low, and implied volatility measures show investors are unworried about shocks: the VIX has fallen well below traditional fear thresholds, the MOVE* Treasury index is at its lowest since 2021, and average six-month implied volatility in the major foreign exchange pairs has dropped to levels not seen since early 2024.

The British pound is struggling to make headway, even after new data showed the economy expanding by more than expected in November, prompting a slight paring in bets on more easing from the Bank of England this year. According to the Office for National Statistics, the UK economy grew 0.3 percent in November—above market forecasts for a 0.1-percent gain—as improving activity levels in the services and production sectors offset a decline in construction. Output slowed sharply in the second half of last year as a number of one-off factors hit, including a cyberattack on Jaguar, labour strikes, uncertainty related to Rachel Reeve’s Autumn Budget, and a rise in global uncertainty levels, and most observers expect to see a modest recovery play out in the coming months. Weakness in labour markets and inflation pressure is still in play however, meaning that monetary policymakers should have room to lower rates at least twice more this year, reducing the sterling’s interest rate premium.

The yen is little changed against the dollar as investors navigate political and monetary cross-currents. The currency has come under attack ahead of Prime Minister Sanae Takaichi’s expected snap election, with a strong showing for her Liberal Democratic Party seen opening the door to higher government spending. That move has been tempered by increasingly hawkish signals from the Bank of Japan: officials have stepped up intervention warnings, and Bloomberg last night reported that policymakers are growing more concerned that prolonged yen weakness could lift underlying inflation expectations. Swaps traders expect the next rate hike to come in June or July, further narrowing cross-Pacific rate differentials and helping offset selling pressure.

In my (admittedly lonely) view, positioning dynamics favour further incremental gains in the dollar over a one- to -three month horizon. Financial conditions remain incredibly loose, and incoming data remains broadly consistent with a US economy that is performing better than expected, reducing the sort of downside risks that might force policymakers to ease rates more aggressively in the first half of the year. Yesterday’s retail sales report underlined continued resilience in consumer spending, helping lift the Atlanta Fed’s GDPNow nowcasting model to a 5.3-percent handle for the fourth quarter, and the Fed’s early-January Beige Book survey—a summary of anecdotes collected from across the central bank’s twelve districts—saw businesses reporting a firming in growth prospects, even before the Big Beautiful Bill Act improves investment incentives and hits household pocketbooks.

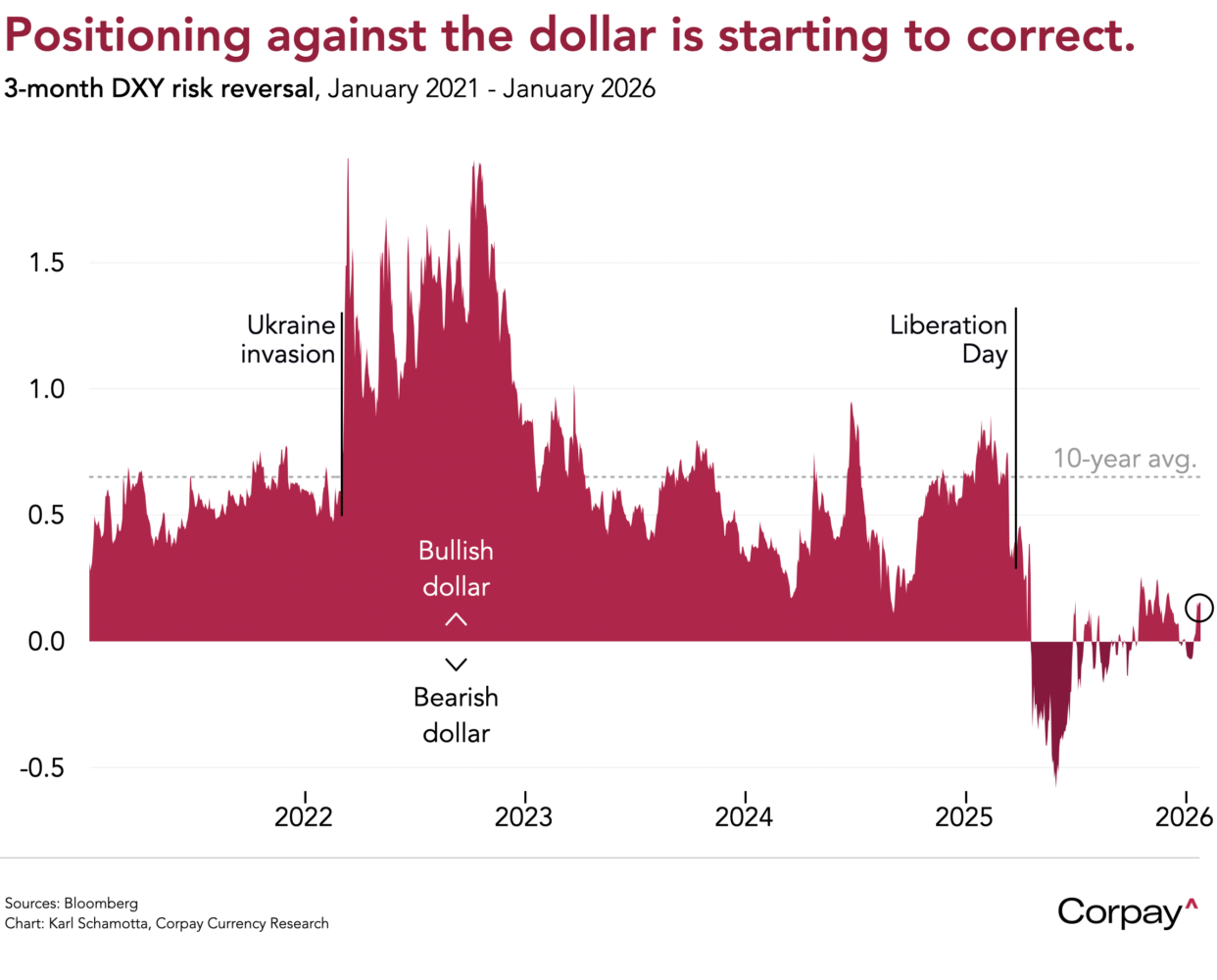

Options traders are growing more positive on the greenback, but risk reversals—which measure the price difference between bullish and bearish bets on the dollar index—are still priced well below historical norms, suggesting that there could be more room for travel in the short term.

To be clear, “US exceptionalism” is still likely to dim over the course of the year as domestic momentum slows, the fiscal impulse in other regions grows stronger, and asset managers reallocate capital to undervalued opportunities in other markets. For now, however, no major advanced economy is matching US growth, expectations for Federal Reserve rate cuts look stretched, and positioning remains heavily skewed against the dollar.