Markets are giving back some of yesterday’s gains as doubts mount over Tuesday’s US-Iran ceasefire agreement, with Israel pressing its assault on targets in Lebanon, Tehran showing no sign of easing its grip on the Strait of Hormuz, and all sides remaining far apart on basic terms. Both the Brent and West Texas Intermediate global crude oil benchmarks are knocking on the $100 threshold once again, front-end Treasury yields are pushing higher, equity futures are pointing to losses, and the dollar is back to outperforming its higher-beta and carry-driven counterparts.

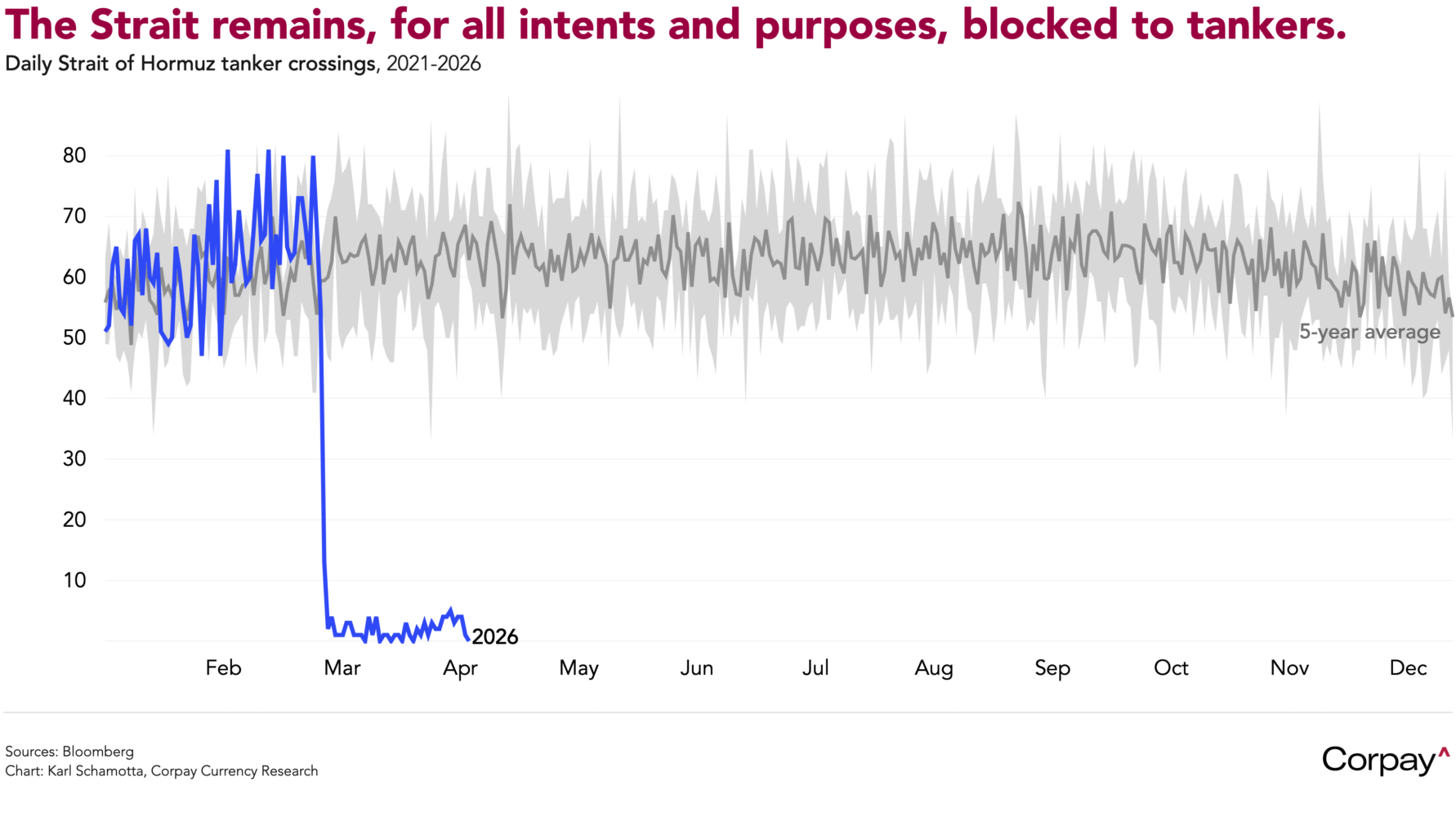

There’s little evidence to suggest that the agreement is translating into an improvement in global energy supply dynamics. Although the tempo has decreased, drone and missile strikes are continuing across the Middle East, Israel is stepping up its attacks on Iranian proxies, and units of the Republican Guards are demanding a toll* from ships seeking to navigate the Strait. Iranian state media are saying that the strait is “fully closed,” and the data bear that out—to our knowledge, no oil or gas tankers have crossed since Tuesday evening***, leaving energy facilities idled throughout the Gulf, and downstream users running low across the planet.

The Federal Reserve’s preferred inflation measure held steady before the war, leaving policy expectations largely unchanged. Data released by the Bureau of Economic Analysis this morning showed the core personal consumption expenditures index rising 0.4 percent in February from the prior month, exactly matching market estimates. On a year-over-year basis, core price growth decelerated to 3.0 percent, slightly below forecast. Personal income fell -0.1 percent month-over-month, and inflation-adjusted household spending climbed 0.1 percent, with both missing forecasts that had been set at 0.3 percent and 0.2 percent, respectively.

Tomorrow’s consumer price index is expected to deliver a bigger shock, with headline inflation jumping by the most since mid-2022 as higher gasoline costs feed through the consumption basket. Second-round effects are likely to be lagged, however, with price pressures taking several months to reach categories such as airfares and food.

Fed officials are keeping their options open. Minutes taken during the central bank’s March meeting, released yesterday, showed most policymakers worried that a “protracted conflict in the Middle East could lead to a further softening in labour market conditions, which could warrant additional rate cuts, as substantially higher oil prices could reduce households’ purchasing power, tighten financial conditions, and reduce growth abroad”. However, “Many participants pointed to the risk of inflation remaining elevated for longer than expected amid a persistent increase in oil prices, which could call for rate increases to help bring inflation down to the committee’s 2 percent objective,” and some felt it would be prudent to incorporate a “two-sided description” of future interest rate decisions.

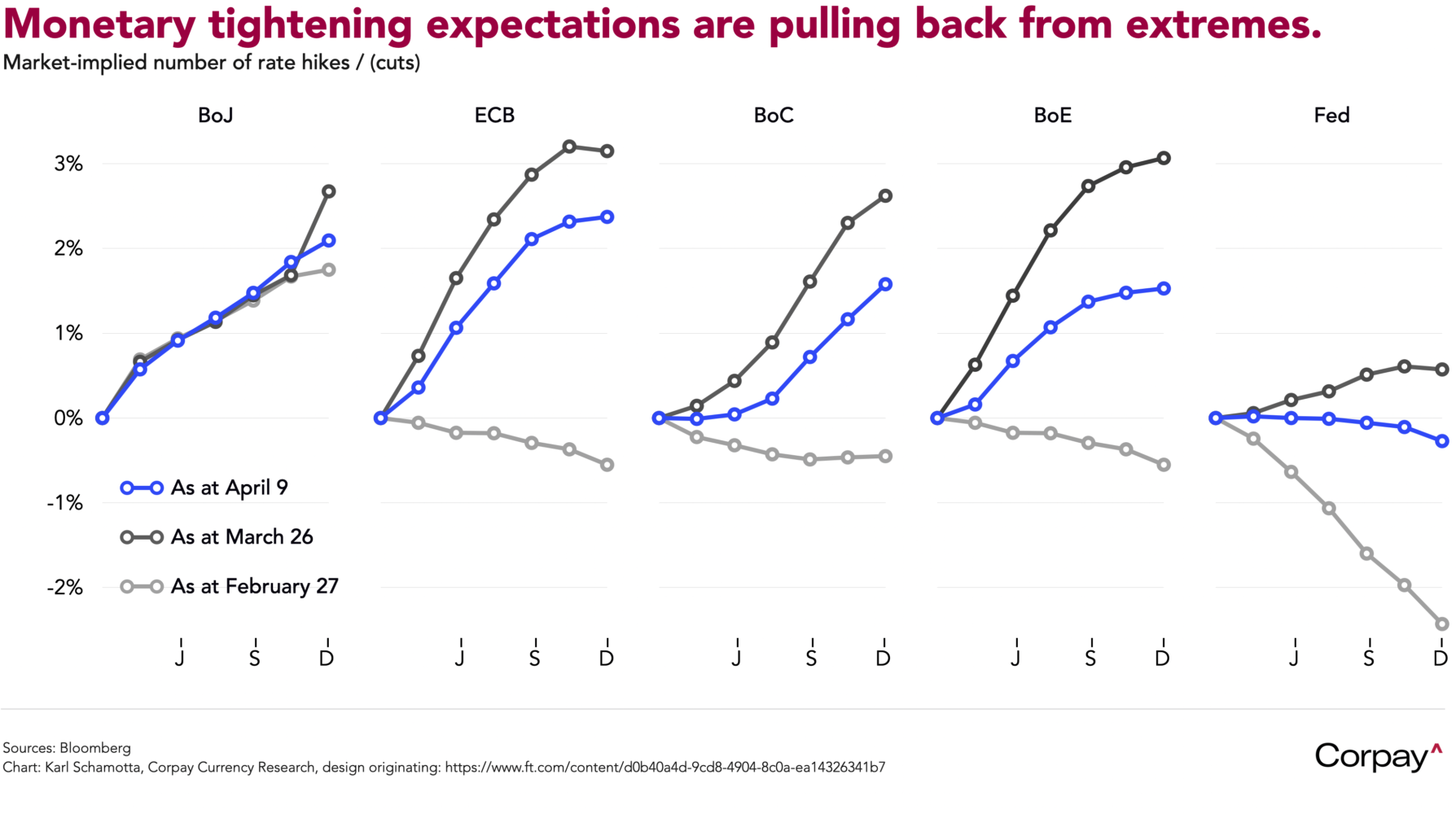

After overshooting, policy expectations are pulling back across advanced-economy bond markets. Swap traders are now assigning one-in-three odds to a Fed rate cut by year-end, while pricing at least one increase from the Bank of England and Bank of Canada, and two each from the European Central Bank and Bank of Japan.

Bottom line: Tuesday’s ceasefire provided a useful market signal by underscoring the Trump administration’s desire to find an exit ramp, but so far it appears worth little more than the paper it was written on****, doing almost nothing to alleviate stress in the global energy complex. We think our year-end forecasts, outlined here, remain viable, but foreign exchange markets are unlikely to fully reset to pre-war levels in the near term, meaning that the dollar should remain bid against energy-importer currencies.

*Incredibly, Trump yesterday told an ABC News reporter he is open to the US joining Iran in charging tolls, and is “thinking of doing it as a joint venture. It’s a way of securing it—also securing it from lots of other people … It’s a beautiful thing.”

**”Incredibly” has, admittedly, lost its meaning in this environment.

***Note that four dry bulk carriers have crossed.

****It was not, to our knowledge, written on paper,