• AUD strength. Positive sentiment & firmer inflation have supported the AUD. This & JPY weakness have propelled AUD/JPY to a multi-decade high.

• Data flow. US producer price inflation due later this week. Looking ahead, AU GDP, as well as the US ISMs, retail sales, & jobs report are out next week.

Global Trends

There was an upbeat tone overnight with limited fresh economic newsflow coming out over the past 24hrs. US and European equities rose. The US S&P500 (+0.8%) is within striking distance of record highs. A solid earnings update from tech heavyweight Nvidia after the US market close may further support risk sentiment in the short-term. Elsewhere, US bond yields ticked up, however the benchmark 10yr rate (now ~4.05%) is still below its 6-month average. In FX, month end portfolio rebalancing looks to be kicking into gear. The USD index was a bit weaker with EUR (the major USD alternative) edging back over ~$1.18. GBP also increased (now ~$1.3553) while the firmer CNH post the Lunar New Year period has seen USD/CNH touch its lowest level since April 2023. The positive risk backdrop underpinned the NZD (now ~$0.60), with the market dynamics and firmer Australian inflation pressures (see below) helping the AUD outperform (now ~$0.7120).

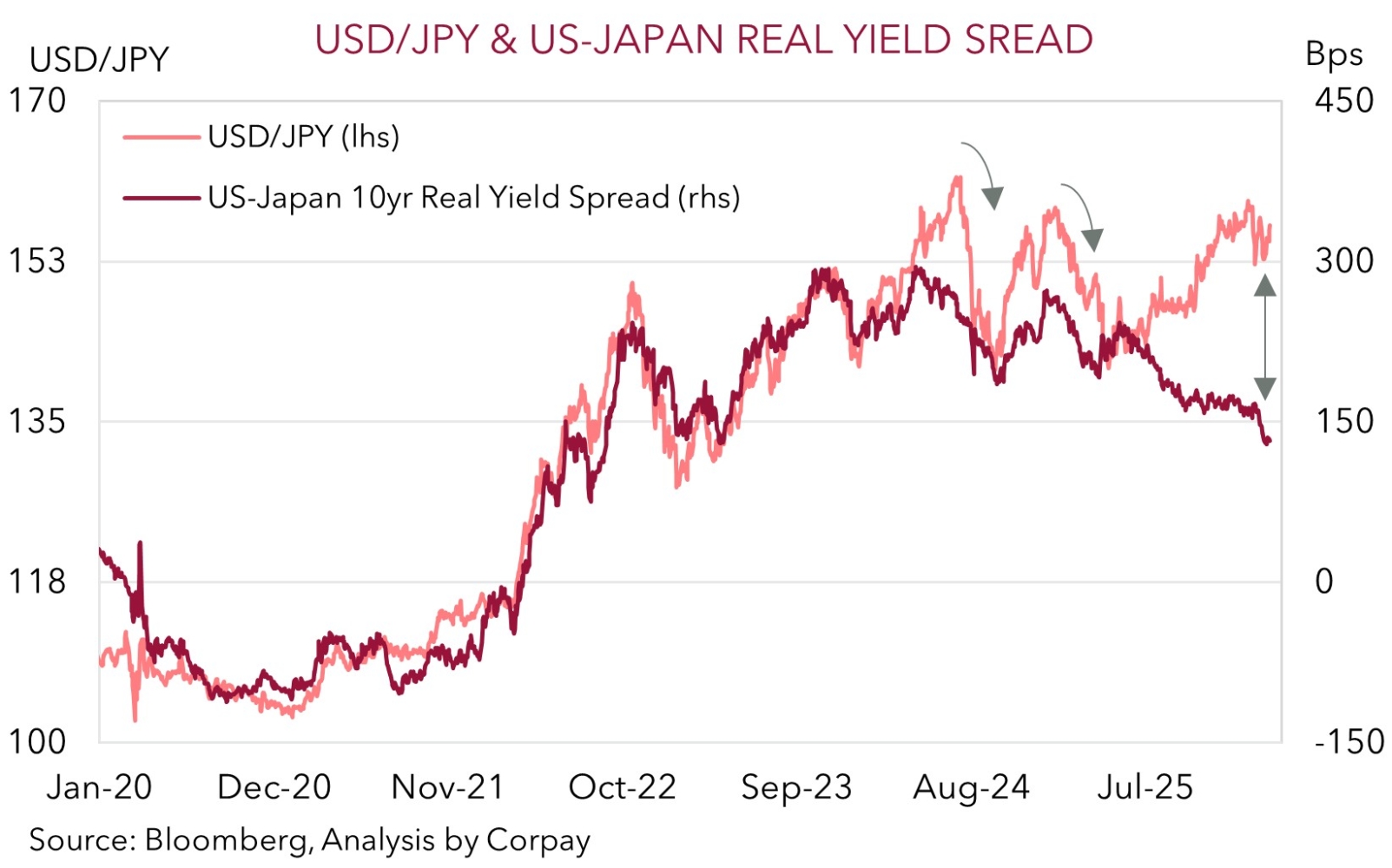

Sticking with FX, the Japanese yen weakened again yesterday with the JPY’s underperformance more than offsetting the softer USD (USD/JPY lifted to ~156.47, ~2% from its mid-January peak). Other JPY crosses are at very elevated levels with AUD/JPY (now ~111.40) around its highest since 1990. The new Japanese government nominated a couple of Bank of Japan board picks to replace outgoing members. The nominees are perceived to have ‘dovish’ leanings. In our view, when it comes to the JPY short-sighted markets are getting caught up chasing momentum and are at risk of a ‘reality check’ reversal, as has been the case a few times over recent years (see chart below). It will be difficult for new members to exert strong influence on the BoJ Board, particularly as the underlying inflation pulse in Japan is stronger than it was in the past and with JPY weakness set to add to price pressures. The odds of a sharp rebound in the undervalued JPY, more towards where fundamentals suggest it should be, over the months ahead are growing, in our opinion.

In the US, weekly initial jobless claims are out tonight (12:30am AEDT), and Producer Price inflation is due tomorrow (Sat 12:30am AEDT). Next week the US data calendar heats up with the ISM business surveys, retail sales, and monthly jobs report scheduled. On balance, we believe signs of improvement in US activity and/or labour market conditions could see the USD claw back lost ground, particularly as it is tracking below our ‘fair value’ estimate.

Trans-Tasman Zone

The positive risk sentiment, as illustrated by the rise in US/European equities and firmer base metal prices like copper/iron ore, has supported the NZD (now ~$0.60). These impulses, combined with firmer Australian inflation and adjustment in RBA interest rate hike expectations, have helped the AUD outperform. At ~$0.7120 the AUD is back near the upper end of its multi-year range. The AUD has also risen by ~0.3-0.6% against the EUR (now ~0.6032), GBP (now ~0.5253), NZD (now ~1.1870), and CNH (now ~4.88) over the past 24hrs. AUD/JPY has powered ahead with the ~1.2% gain propelling it to levels last traded in 1990 (now ~111.40). Indeed, since 1988 AUD/JPY has only been above where it now is in ~3% of trading days. As discussed above, we don’t think the JPY weakness will be sustained, and AUD/JPY risks reversing course quite quickly down the track.

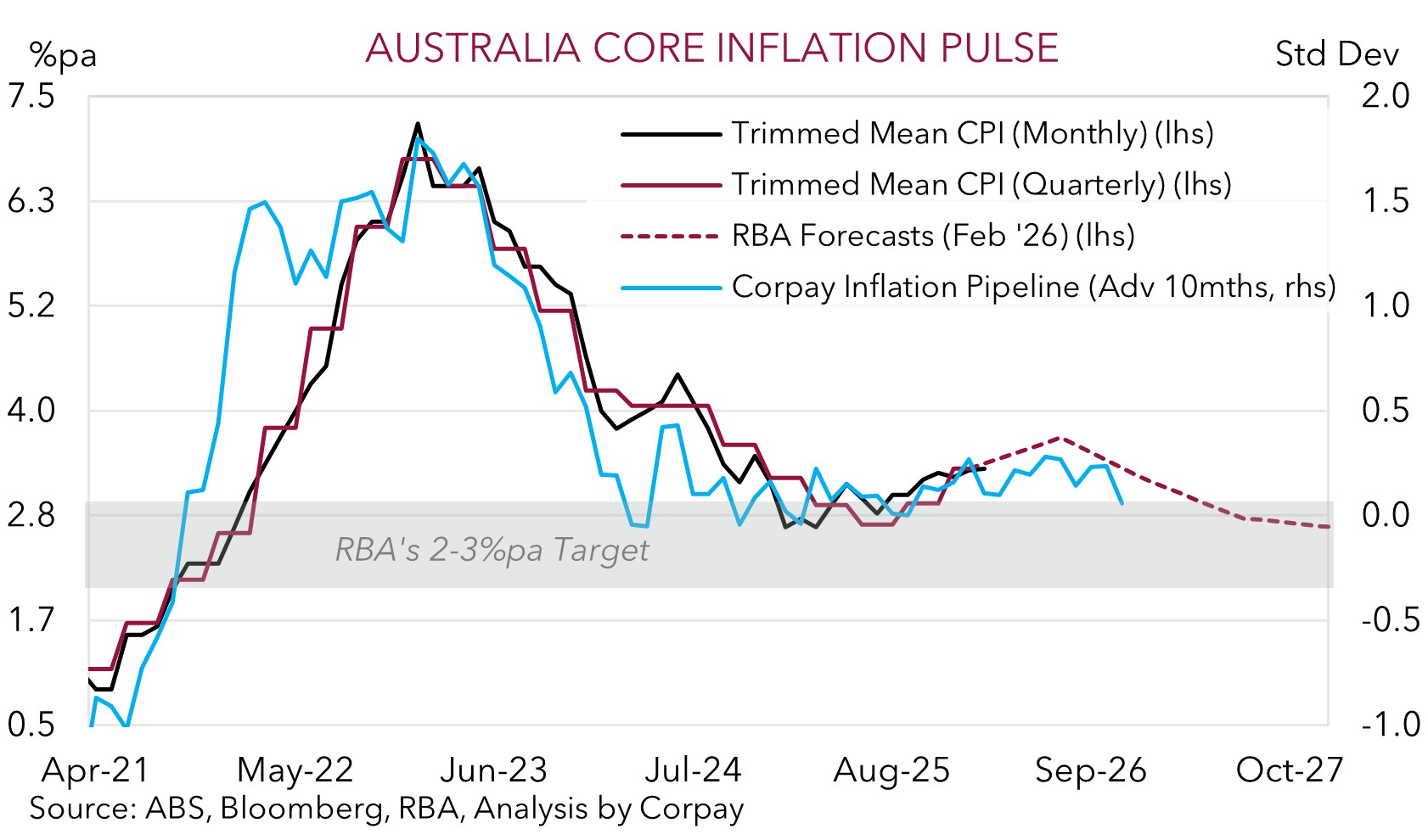

In terms of the Australian data the monthly CPI figures for January showed that price pressures remain firm. Core inflation (i.e. the trimmed mean) nudged up from 3.34% to 3.36%pa (this was rounded to 3.4%pa). Our pipeline measure indicates this sticky inflation trend might remain for a while (see chart below). The question is whether inflation is better/worse than what the RBA is anticipating. We calculate that the 3-month trimmed mean (which matches up with the quarterly inflation pulse) has eased to ~0.80%. It is still early in the quarter, but this run-rate looks to be a bit under what the RBA has penciled in for Q1. However, inflation is still uncomfortably high as quarterly CPI needs to run at ~0.6% to be consistent with the RBA’s target, so another rate hike by May looks likely, in our view. This is now ~90% priced in with ~40bps worth of tightening discounted by November.

From our perspective, the direct AUD tailwind from an upward adjustment in RBA interest rate expectations may be close to running its course. Outcomes compared to expectations matter, and there is a decent amount of tightening baked in. Based on this framework, with the negative effects of higher interest rates set to materialise across the economy later this year, and potential for a USD rebound due to an upturn in the US economy we remain of the opinion that ~$0.72 might be a ceiling for the AUD. That said, the shift up in the level of interest rates and swing in interest rate differentials in Australia’s favour should also limit how deep and long-lasting AUD pull-backs are without an acute bout of risk aversion. On net, we see the AUD tracking in a higher average range than what it has over the past few years (over 2024/25 the AUD averaged ~$0.6520).