Good morning, and happy Groundhog Day*. The dollar is strengthening and Treasury yields are rising as diplomatic efforts to reopen the Strait of Hormuz falter once again. Iran and the United States said last week they had reached a tentative deal to halt the war, but nothing has been signed and events on the ground moved in the opposite direction overnight: Iranian missiles damaged Kuwait’s airport and targeted Bahrain, attacks on commercial shipping resumed, US forces carried out strikes in response, and Israel continued its assault on Lebanese towns despite an American-brokered ceasefire. Both global crude benchmarks are up more than 2% on the session, and equity markets, having hit record highs, look set to consolidate at the open.

Most major currencies are stuck in defensive holding patterns after the United States unveiled yet another round of trade duties. The Office of the US Trade Representative last night said products from Canada, Mexico, Taiwan, the European Union and Britain, among others, would face a 10% tariff, while a higher 12.5% rate would be imposed on China, Japan, India, South Korea and Switzerland. Trade Representative Jamieson Greer framed the measures as a matter of fairness for American workers, claiming the group—which encompasses most major US trading partners—has failed to enforce prohibitions on goods made with forced labour, but the move appears designed to replace two earlier rounds of tariffs issued under the International Emergency Economic Powers Act and Section 122 of the Trade Act, both of which were struck down by the courts. Although this latest effort, rooted in a Section 301 unfair trade practices investigation, may prove no more durable**, the uncertainty alone is enough to keep businesses cautious and currencies range-bound.

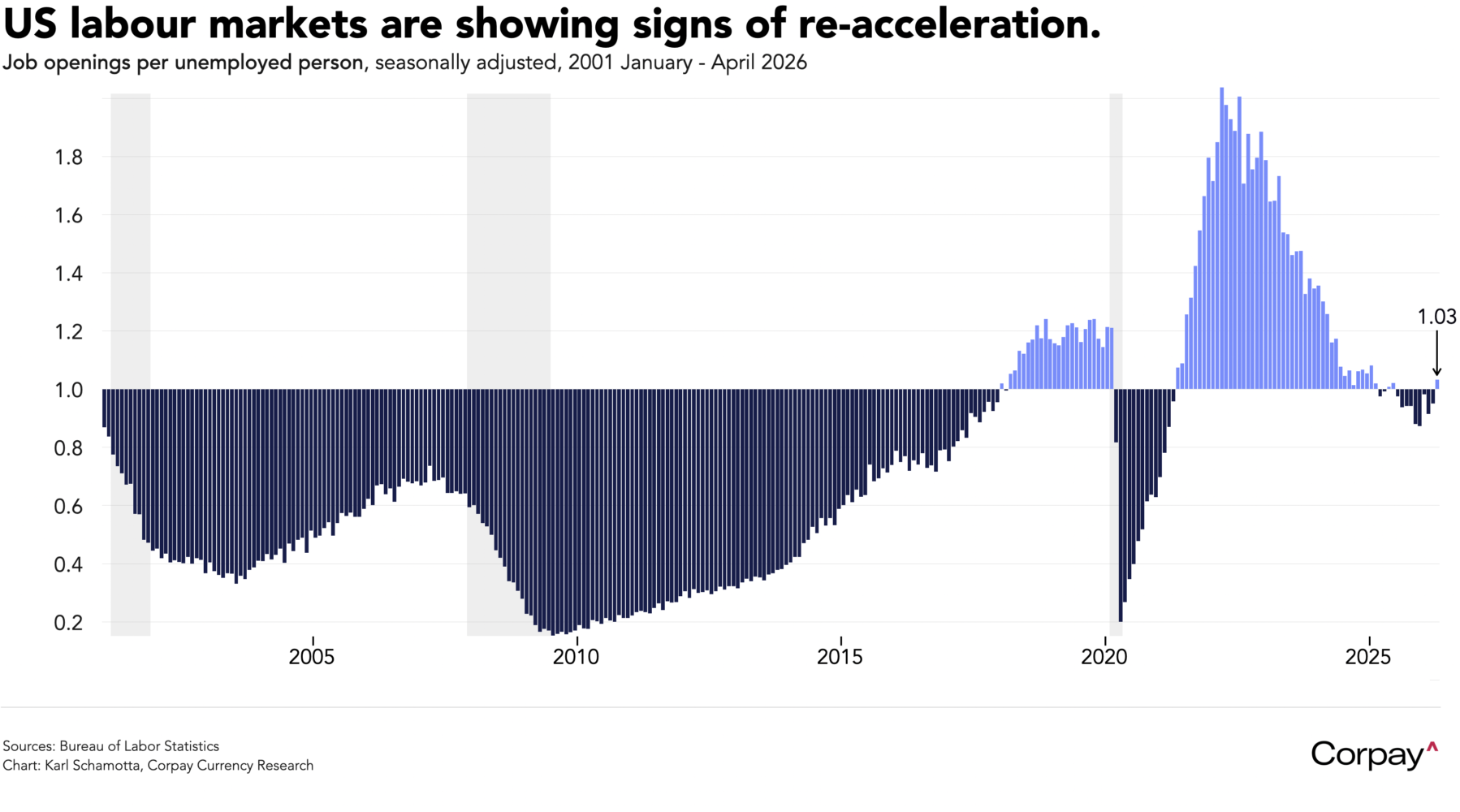

The dollar is trading with a bid after data published yesterday showed US job openings climbing more than forecast in April, raising expectations ahead of Friday’s non-farm payrolls report. The Bureau of Labor Statistics reported 731,000 new postings in the month, mostly concentrated in professional and business services***, while the ratio of vacancies to unemployed workers jumped to 1.03 from an upwardly revised 0.95 in March—back above the one-to-one threshold that typically signals a tight labour market. Today could bring more of the same: the ADP employment report, the May ISM services index and the Fed’s Beige Book survey are all due, and if they remain consistent with solid hiring and margin expansion among corporates, the dollar could climb further.

In stark contrast, private-sector activity in the euro area shrank at its fastest pace in 18 months in May, with demand for goods and services weakening enough to drag output lower for a second consecutive month. The S&P Global composite purchasing managers’ index fell to 48.5 from April’s 48.8, marking its lowest reading since November 2024, as Germany and France both recorded contractions while Italy and Spain managed to eke out modest expansions. The European Central Bank is expected to hike next week and again in September, raising the possibility that Frankfurt is once again tightening into a downturn. The euro is underperforming the British pound and most of its major counterparts as traders further downgrade growth expectations.

The Japanese yen is still flirting with the 160 mark against the dollar, prompting Prime Minister Sanae Takaichi to warn that authorities stand ready to act on exchange-rate moves as needed. Data released on Friday showed Japan spent ¥11.7trn ($74bn) in a single month from late April—the largest intervention round on record—to little avail. A steep rate discount against the dollar continues to put the yen under sustained downward pressure, and no amount of reserve-selling is likely to close that gap permanently.

Currency markets are largely becalmed, with daily trading ranges remaining incredibly tight and most major pairs holding close to their 200-day moving averages. Uncertainty over the path of inflation, the direction of Fed policy and the outcome of the war in the Middle East is keeping speculators on the sidelines, reluctant to place directional bets or enter carry trades*** that could be upended by a sudden shift in any of the three. Many hedgers, lulled into a sense of complacency by low implied and realised volatility, are sitting on the sidelines.

But a tipping point may be approaching. After months of drawdowns, global energy inventories are nearing levels at which supply shortages could trigger non-linear moves in prices and turmoil across financial markets. Against this backdrop, the current “muddle-through” playbook looks unsustainable, with the outlook turning increasingly binary: In one scenario, the United States steps back from the conflict, Iran allows the Strait to reopen, and safe-haven trades unwind sharply—forcing a reappraisal of monetary-policy trajectories, a decline in the dollar, and a recovery in energy-sensitive currencies. In the other, the closure persists, major importers suffer another leg down, the dollar squeezes higher, and the world braces for a sustained wave of inflation. It makes sense to prepare for either outcome, even if the former is more likely.

*I know it’s not actually Groundhog Day, but the sense of deja vu is overwhelming. As a certain weatherman once put it, “What if there is no tomorrow? There wasn’t one today”.

**A narrower set of Section 301 levies would likely withstand challenges, but generally speaking, the Constitution assigns broad tariff powers to Congress, not the executive.

***This seems suspicious. As far as I can tell, labour markets now consist of artificial intelligence systems writing job postings and artificial intelligence systems applying for them. It may be many months before a concrete hiring signal emerges from the noise.

****Borrowing in low-yielding currencies to invest in higher-yielding ones, with the intention of profiting from rate differentials.*****

*****Also known as “picking up nickels in front of steamrollers,” after a long and distinguished history of delivering steady returns before suddenly flattening traders who had no business being surprised.